Comments Template QRT Assets final - eiopa

... EIOPA would like to thank Afa Sjukförsäkring, AFA Trygghetsförsäkring, AFA Livförsäkring, Audit&Consulting Services – Poland, AM Best, AMICE, ANIA Reinsurance Working Group, Association of British Insurers (ABI), Association of Financial Mutuals (AFM), AXERIA PREVOYANCE – AXERIA IARD – SOLUCIA, Barn ...

... EIOPA would like to thank Afa Sjukförsäkring, AFA Trygghetsförsäkring, AFA Livförsäkring, Audit&Consulting Services – Poland, AM Best, AMICE, ANIA Reinsurance Working Group, Association of British Insurers (ABI), Association of Financial Mutuals (AFM), AXERIA PREVOYANCE – AXERIA IARD – SOLUCIA, Barn ...

Statement of Financial Accounting Standards No. 140

... loan syndications and participations, risk participations in banker's acceptances, factoring arrangements, transfers of receivables with recourse, and extinguishments of liabilities. This Statement also provides guidance about whether a transferor has retained effective control over assets transferr ...

... loan syndications and participations, risk participations in banker's acceptances, factoring arrangements, transfers of receivables with recourse, and extinguishments of liabilities. This Statement also provides guidance about whether a transferor has retained effective control over assets transferr ...

Subprime Lending, Suboptimal Bankruptcy: A Proposal to Amend

... the enormous growth in the subprime mortgage lending market is a relatively recent phenomenon. When the Bankruptcy Code was adopted in 1978, policymakers were not concerned with the impact of mortgage lending on bankruptcy policy. Quite the opposite: in the environment of the late 1970s, in which ho ...

... the enormous growth in the subprime mortgage lending market is a relatively recent phenomenon. When the Bankruptcy Code was adopted in 1978, policymakers were not concerned with the impact of mortgage lending on bankruptcy policy. Quite the opposite: in the environment of the late 1970s, in which ho ...

SWD(2014) 61 final - European Commission

... At a time when the European Union (EU) is facing the biggest economic crisis in its history leading to record numbers of bankruptcies in most Member States, improving the efficiency of insolvency laws in the EU has become an important factor in supporting the economic recovery. In recent years, an a ...

... At a time when the European Union (EU) is facing the biggest economic crisis in its history leading to record numbers of bankruptcies in most Member States, improving the efficiency of insolvency laws in the EU has become an important factor in supporting the economic recovery. In recent years, an a ...

US CORNER - Paul, Weiss

... would be triggered prior to those of any other creditor. Unsecured creditors would usually have no financial covenants and much looser negative covenants. Problems that would trigger first lien lenders covenants might not even give rise to a default under the unsecured debt. If there were a problem ...

... would be triggered prior to those of any other creditor. Unsecured creditors would usually have no financial covenants and much looser negative covenants. Problems that would trigger first lien lenders covenants might not even give rise to a default under the unsecured debt. If there were a problem ...

Annual Report - John Hancock Investments

... uncertainty to the global economic outlook, and it remains to be seen whether other countries will follow suit. Many investment professionals believe that global central banks will likely expand their efforts to stimulate economic activity and that the fallout from Brexit, combined with the November ...

... uncertainty to the global economic outlook, and it remains to be seen whether other countries will follow suit. Many investment professionals believe that global central banks will likely expand their efforts to stimulate economic activity and that the fallout from Brexit, combined with the November ...

Document

... III. THIRD PARTY EFFECTIVENESS (PUBLICATION/PERFECTION) ........... 29 A. CREATION/ATTACHMENT, PERFECTION/PUBLICATION, AND PRIORITY .......................................................... 29 B. PURPOSES OF PERFECTION/PUBLICATION..................................................................... ...

... III. THIRD PARTY EFFECTIVENESS (PUBLICATION/PERFECTION) ........... 29 A. CREATION/ATTACHMENT, PERFECTION/PUBLICATION, AND PRIORITY .......................................................... 29 B. PURPOSES OF PERFECTION/PUBLICATION..................................................................... ...

Equity Auctions and the New Value Corollary to the

... exchange for old shares, the creditors were entitled to the benefit of that value, whether it was present or prospective, for dividends or only for purposes of control. In either event it was a right of property out of which the creditors were entitled to be paid before the stockholders could retain ...

... exchange for old shares, the creditors were entitled to the benefit of that value, whether it was present or prospective, for dividends or only for purposes of control. In either event it was a right of property out of which the creditors were entitled to be paid before the stockholders could retain ...

Proposed features of a sovereign debt restructur

... Finally, there is the question of the treatment of official bilateral claims under the amendment. At the conclusion of their discussion of the November paper, Directors expressed the views that the preferred course of action would be to proceed, at least initially, on the basis of excluding official ...

... Finally, there is the question of the treatment of official bilateral claims under the amendment. At the conclusion of their discussion of the November paper, Directors expressed the views that the preferred course of action would be to proceed, at least initially, on the basis of excluding official ...

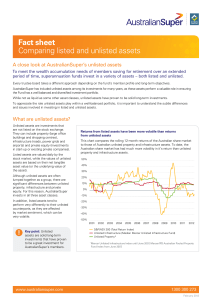

Fact sheet Comparing listed and unlisted assets

... In the case of infrastructure, high quality unlisted assets also have predictable revenue streams, particularly if they are based around a long-term contract (often with government) or regulated charges. Prior to the GFC many listed infrastructure funds adopted the practice of paying income to inves ...

... In the case of infrastructure, high quality unlisted assets also have predictable revenue streams, particularly if they are based around a long-term contract (often with government) or regulated charges. Prior to the GFC many listed infrastructure funds adopted the practice of paying income to inves ...

Intangible assets and SMEs

... ACCA (the Association of Chartered Certified Accountants) is the largest and fastest-growing global professional accountancy body with 296,000 students and 115,000 members in 170 countries. We aim to offer first-choice qualifications to people of application, ability and ambition around the world wh ...

... ACCA (the Association of Chartered Certified Accountants) is the largest and fastest-growing global professional accountancy body with 296,000 students and 115,000 members in 170 countries. We aim to offer first-choice qualifications to people of application, ability and ambition around the world wh ...

Preview

... The process described here, whereby intangible assets are used to generate pecuniary returns to satisfy financial motives is part of the process of financialization. In general, financialization refers to “a pattern of accumulation in which profits accrue primarily through financial channels rather ...

... The process described here, whereby intangible assets are used to generate pecuniary returns to satisfy financial motives is part of the process of financialization. In general, financialization refers to “a pattern of accumulation in which profits accrue primarily through financial channels rather ...

November 28, 2006

... • Modigliani and Miller (1958) argued that in the absence of bankruptcy costs and tax subsidies on the payment of interest, the value of the firm is independent of the financial structure. • Modigliani and Miller later (1963) argued that the existence of tax subsidies on interest payments would caus ...

... • Modigliani and Miller (1958) argued that in the absence of bankruptcy costs and tax subsidies on the payment of interest, the value of the firm is independent of the financial structure. • Modigliani and Miller later (1963) argued that the existence of tax subsidies on interest payments would caus ...

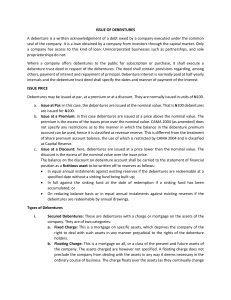

ISSUE OF DEBENTURES A debenture is a written

... Debentures may be issued at par, at a premium or at a discount. They are normally issued in units of N100. a. Issue at Par: in this case, the debentures are issued at the nominal value. That is N100 debentures are issued for N100. b. Issue at a Premium: in this case debentures are issued at a price ...

... Debentures may be issued at par, at a premium or at a discount. They are normally issued in units of N100. a. Issue at Par: in this case, the debentures are issued at the nominal value. That is N100 debentures are issued for N100. b. Issue at a Premium: in this case debentures are issued at a price ...

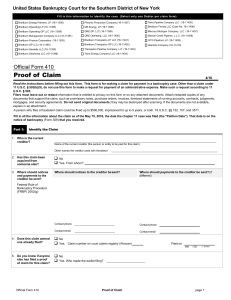

Proof of Claim - Cases

... I understand that an authorized signature on this Proof of Claim serves as an acknowledgment that when calculating the amount of the claim, the creditor gave the debtor credit for any payments received toward the debt. I have examined the information in this Proof of Claim and have a reasonable beli ...

... I understand that an authorized signature on this Proof of Claim serves as an acknowledgment that when calculating the amount of the claim, the creditor gave the debtor credit for any payments received toward the debt. I have examined the information in this Proof of Claim and have a reasonable beli ...

Development of Insolvency Law as Part of the Transition from a

... parties cannot agree. If the parties cannot agree on a reorganization, the law could provide for an ability to force a reorganization if certain criteria are met (minimum recoveries for creditors), or the law could provide that the enterprise's assets should be liquidated. ...

... parties cannot agree. If the parties cannot agree on a reorganization, the law could provide for an ability to force a reorganization if certain criteria are met (minimum recoveries for creditors), or the law could provide that the enterprise's assets should be liquidated. ...

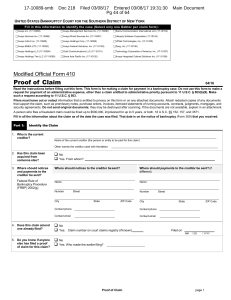

Bankruptcy Court Proof of Claim form

... Claim Pursuant to 11 U.S.C. § 503(b)(9): A claim arising from the value of any goods received by the Debtor within 20 days before the date of commencement of the above case, in which the goods have been sold to the Debtor in the ordinary course of the Debtor's business. Attach documentation supporti ...

... Claim Pursuant to 11 U.S.C. § 503(b)(9): A claim arising from the value of any goods received by the Debtor within 20 days before the date of commencement of the above case, in which the goods have been sold to the Debtor in the ordinary course of the Debtor's business. Attach documentation supporti ...

open-end credit under -truth-in- lending

... Even though other writers participating in the Symposium will undoubtedly cover this, it seems worth noting at this point, before going into the peculiar disclosure requirements applicable to Open-End Credit. As simply one example, the "general disclosure requirements" are applicable to all classes ...

... Even though other writers participating in the Symposium will undoubtedly cover this, it seems worth noting at this point, before going into the peculiar disclosure requirements applicable to Open-End Credit. As simply one example, the "general disclosure requirements" are applicable to all classes ...

Preference Actions?

... December 12th which remained unpaid to offset the two payments totaling $15,000 made on December 1st and December 5th, but would not be able to offset the final $7,000 payment received on December 18th because there were no subsequent advances after that payment. Accordingly, under this scenario the ...

... December 12th which remained unpaid to offset the two payments totaling $15,000 made on December 1st and December 5th, but would not be able to offset the final $7,000 payment received on December 18th because there were no subsequent advances after that payment. Accordingly, under this scenario the ...

Financial distress, reorganization and corporate performance

... sion (ASIC) 1998). Growth in use of VA presents significant opportunities and challenges for accounting professionals, and it is important that accountants understand the operation of the legislation and its suitability for particular clients. For example, timely recommendation to initiate VA by pro ...

... sion (ASIC) 1998). Growth in use of VA presents significant opportunities and challenges for accounting professionals, and it is important that accountants understand the operation of the legislation and its suitability for particular clients. For example, timely recommendation to initiate VA by pro ...

Bankruptcy Equilibrium: Secured and Unsecured assets

... her debt, in this situation we say that she goes bankruptcy. Allowing for bankruptcy brings some technical difficulties, agent’s feasible set (including consumption and portfolio) is no longer a convex set, so it is possible that the best response correspondence is not convex, this prevents us to us ...

... her debt, in this situation we say that she goes bankruptcy. Allowing for bankruptcy brings some technical difficulties, agent’s feasible set (including consumption and portfolio) is no longer a convex set, so it is possible that the best response correspondence is not convex, this prevents us to us ...

introduction to financial statements

... ASSETS – WHAT ARE THEY M. Nowicki defines assets “as economic resources that provide or are expected to provide benefit to the organization” Hmm… does that really help you? ...

... ASSETS – WHAT ARE THEY M. Nowicki defines assets “as economic resources that provide or are expected to provide benefit to the organization” Hmm… does that really help you? ...

AIFMD – Assets other than financial instruments held in custody

... an asset as well as cases where the AIF holds legal title to an asset. Since depositaries may not have possession of the AIF's "other assets", it will be necessary for depositaries to obtain the relevant information either directly from the AIF or its manager (AIFM) or from other sources. ...

... an asset as well as cases where the AIF holds legal title to an asset. Since depositaries may not have possession of the AIF's "other assets", it will be necessary for depositaries to obtain the relevant information either directly from the AIF or its manager (AIFM) or from other sources. ...

In any secured financing, a borrower`s undertakings relating to

... Collateral. In cross‐border financings, for non‐U.S. entities that are not subject to these tax considerations, costs of obtaining perfected security interests may still be very substantial, and can include such things as high stamp tax on the creation and/or registration of liens, costly no ...

... Collateral. In cross‐border financings, for non‐U.S. entities that are not subject to these tax considerations, costs of obtaining perfected security interests may still be very substantial, and can include such things as high stamp tax on the creation and/or registration of liens, costly no ...