chapter 6

... 5. Indicate the effects of inventory errors on the financial statements. In the income statement of the current year: (a) An error in beginning inventory will have a reverse effect on net income. (b) An error in ending inventory will have a similar effect on net income. In the following period, its ...

... 5. Indicate the effects of inventory errors on the financial statements. In the income statement of the current year: (a) An error in beginning inventory will have a reverse effect on net income. (b) An error in ending inventory will have a similar effect on net income. In the following period, its ...

Table of Contents - Ontario Energy Board

... shall be supported by such detailed information as will permit ready identification, examination, analysis, and verification of all relevant facts. The records shall be filed in such a manner as to be readily accessible for examination by authorized representatives of the Board; ...

... shall be supported by such detailed information as will permit ready identification, examination, analysis, and verification of all relevant facts. The records shall be filed in such a manner as to be readily accessible for examination by authorized representatives of the Board; ...

- TestbankU

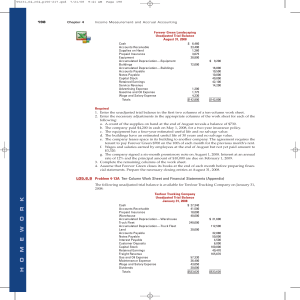

... involves the procedures for measuring, recording, and reporting product costs. From the data accumulated, companies determine the total cost and the unit cost of each product. The two basic types of cost accounting systems are job order cost and process cost. In job order costing, companies first ac ...

... involves the procedures for measuring, recording, and reporting product costs. From the data accumulated, companies determine the total cost and the unit cost of each product. The two basic types of cost accounting systems are job order cost and process cost. In job order costing, companies first ac ...

66862 c07 296-365

... Banks, hotels, airlines, health clubs, real estate offices, law firms, and accounting firms are all examples of service companies. In this chapter we turn to accounting by companies that sell products, or what accountants call inventory. Companies that sell inventory can be broadly categorized into ...

... Banks, hotels, airlines, health clubs, real estate offices, law firms, and accounting firms are all examples of service companies. In this chapter we turn to accounting by companies that sell products, or what accountants call inventory. Companies that sell inventory can be broadly categorized into ...

Chapter 02 Job Order Costing and Analysis

... 15. When a job is finished, its job cost sheet is completed and moved from the file of jobs in process to the file of finished jobs that are yet to be delivered to customers. ...

... 15. When a job is finished, its job cost sheet is completed and moved from the file of jobs in process to the file of finished jobs that are yet to be delivered to customers. ...

HOMEWORK

... merchandise in finished form and offer it for resale without transforming the product in any way. Merchandise companies typically have a relatively large dollar amount in inventory. For example, on its February 3, 2007, balance sheet, Gap Inc. reported merchandise inventory of $1,796 million and tot ...

... merchandise in finished form and offer it for resale without transforming the product in any way. Merchandise companies typically have a relatively large dollar amount in inventory. For example, on its February 3, 2007, balance sheet, Gap Inc. reported merchandise inventory of $1,796 million and tot ...

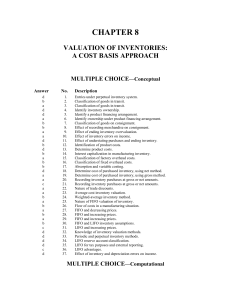

chapter 8 - Csulb.edu

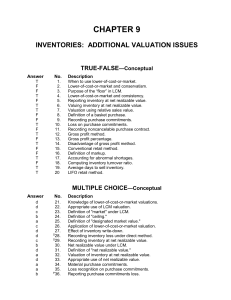

... Which of the following statements is not valid as it applies to inventory costing methods? a. If inventory quantities are to be maintained, part of the earnings must be invested (plowed back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net incom ...

... Which of the following statements is not valid as it applies to inventory costing methods? a. If inventory quantities are to be maintained, part of the earnings must be invested (plowed back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net incom ...

Answer No. Description - accountingreviewmaterials

... company may value inventory at cost in one year and at market in the next year. ...

... company may value inventory at cost in one year and at market in the next year. ...

extract

... bookkeeping emerged spontaneously in 13th century Italian businesses and was summarized in Pacioli’s (1494) classic printed text. After the corporate form was introduced in 16th century Britain (Micklethwait and Wooldridge, 2003), bookkeeping increased in complexity. Accounting, which classifies, ag ...

... bookkeeping emerged spontaneously in 13th century Italian businesses and was summarized in Pacioli’s (1494) classic printed text. After the corporate form was introduced in 16th century Britain (Micklethwait and Wooldridge, 2003), bookkeeping increased in complexity. Accounting, which classifies, ag ...

Assignment 1 is compulsory and due

... product cost info. Also essential to have accurate costing info when making pricing decision. Users of financials made up of : management of entity shareholders of entity & other interested parties (creditors, staff and government) So need to have info for all these people either : financial a ...

... product cost info. Also essential to have accurate costing info when making pricing decision. Users of financials made up of : management of entity shareholders of entity & other interested parties (creditors, staff and government) So need to have info for all these people either : financial a ...

PUBLIC SECTOR ACCOUNTING REFORM Tatjana Jovanović

... of core government and may overlap with the not-for-profit or private sectors. For the purposes of this guidance, the public sector consists of an expanding ring of organizations, with core government at the centre, followed by agencies and public enterprises. Around this centre, there is a zone con ...

... of core government and may overlap with the not-for-profit or private sectors. For the purposes of this guidance, the public sector consists of an expanding ring of organizations, with core government at the centre, followed by agencies and public enterprises. Around this centre, there is a zone con ...

Moderate

... 9. By their nature, product costs “attach” to the inventory and are recorded in the inventory account. These costs are directly connected with the bringing of goods to the place of business of the buyer and converting such goods to a salable condition. Such charges would include freight charges on g ...

... 9. By their nature, product costs “attach” to the inventory and are recorded in the inventory account. These costs are directly connected with the bringing of goods to the place of business of the buyer and converting such goods to a salable condition. Such charges would include freight charges on g ...

Accounting for Government and Society

... modern economies. The task of such research, however, has been facilitated by the development of well defined models of investor behavior and the widespread availability of large data bases. But capital markets are not ‘society’, and many other needs and concerns may be overlooked with a pursuit of ...

... modern economies. The task of such research, however, has been facilitated by the development of well defined models of investor behavior and the widespread availability of large data bases. But capital markets are not ‘society’, and many other needs and concerns may be overlooked with a pursuit of ...

The Role of Accounting in a Society

... of core methodological solutions, theory, and policy of accounting. In relation to this, Funell (2007, p. 23) asserted that accounting actually “has no virtue outside that which the social, legal and economic frameworks in which it operates allows it... [and that the] relevance of accounting to a so ...

... of core methodological solutions, theory, and policy of accounting. In relation to this, Funell (2007, p. 23) asserted that accounting actually “has no virtue outside that which the social, legal and economic frameworks in which it operates allows it... [and that the] relevance of accounting to a so ...

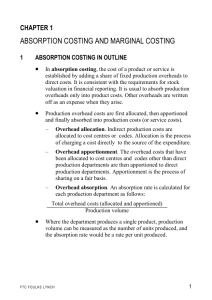

absorption costing and marginal costing chapter 1

... Transfers of inventory are recorded as a credit entry in the inventory account from which the transfer is made and the debit entry is to the account representing the cost or value of where the inventory was transferred to. (i) Transfers of raw materials from stores are recorded as a credit entry i ...

... Transfers of inventory are recorded as a credit entry in the inventory account from which the transfer is made and the debit entry is to the account representing the cost or value of where the inventory was transferred to. (i) Transfers of raw materials from stores are recorded as a credit entry i ...

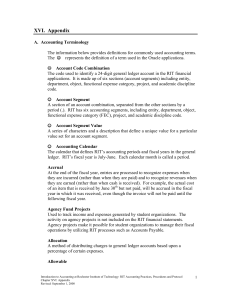

Appendix

... they are earned (rather than when cash is received). For example, the actual cost of an item that is received by June 30th but not paid, will be accrued in the fiscal year in which it was received, even though the invoice will not be paid until the following fiscal year. Agency Fund Projects Used to ...

... they are earned (rather than when cash is received). For example, the actual cost of an item that is received by June 30th but not paid, will be accrued in the fiscal year in which it was received, even though the invoice will not be paid until the following fiscal year. Agency Fund Projects Used to ...

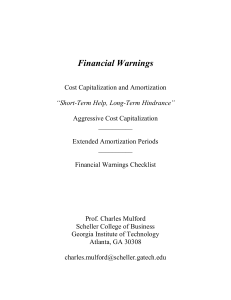

Capitalized Costs - National Association of Credit Management

... devoted to discussion of HealthSouth Corp. "What I know about the accounting at HRC will be the blow that will bring HRC to its knees," wrote the individual, alluding to the company's stock symbol and using the alias Junior followed by eight numbers. A few minutes later, he added, "what is going on ...

... devoted to discussion of HealthSouth Corp. "What I know about the accounting at HRC will be the blow that will bring HRC to its knees," wrote the individual, alluding to the company's stock symbol and using the alias Junior followed by eight numbers. A few minutes later, he added, "what is going on ...

Cost Concepts and Behavior - McGraw Hill Higher Education

... In addition, managers need to understand how financial statements are commonly prepared because this will often be the primary form in which the information is available. The effects of the decisions made by managers are shown publicly in the firm’s published financial statements. Although these sta ...

... In addition, managers need to understand how financial statements are commonly prepared because this will often be the primary form in which the information is available. The effects of the decisions made by managers are shown publicly in the firm’s published financial statements. Although these sta ...

inventory cost flow for a - McGraw

... inventory, is designed to evaluate a company's effectiveness in managing its investment in inventory. ...

... inventory, is designed to evaluate a company's effectiveness in managing its investment in inventory. ...

CJAR Fundamentalist Perspective on Accounting Jiang

... lacking direction as to the specific accounting that satisfies the objective. One needs to cut to the quick: what is the accounting that the user requires to forecast cash flows? The answer to this question might be solicited by going to investors and analysts directly and posing the question. Inde ...

... lacking direction as to the specific accounting that satisfies the objective. One needs to cut to the quick: what is the accounting that the user requires to forecast cash flows? The answer to this question might be solicited by going to investors and analysts directly and posing the question. Inde ...

Management Accounting System for Hospitals (MASH) Manual

... MASH is an Excel workbook built around 12 interrelated spreadsheets. Four of these involve entering primary data and the other eight use that data to perform calculations and analysis. All the spreadsheets are structured by cost centers – organizational units with distinct function, output, technolo ...

... MASH is an Excel workbook built around 12 interrelated spreadsheets. Four of these involve entering primary data and the other eight use that data to perform calculations and analysis. All the spreadsheets are structured by cost centers – organizational units with distinct function, output, technolo ...

Intermediate Accounting, Eighth Canadian Edition

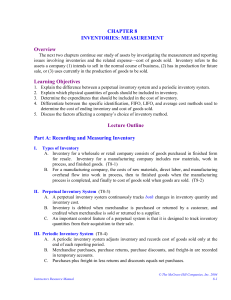

... After studying this chapter, you should be able to: • Understand inventory from a business perspective. • Define inventory from an accounting perspective. • Identify which inventory items should be included in ending inventory. • Identify the effects of inventory errors on the financial statements a ...

... After studying this chapter, you should be able to: • Understand inventory from a business perspective. • Define inventory from an accounting perspective. • Identify which inventory items should be included in ending inventory. • Identify the effects of inventory errors on the financial statements a ...

Accounting 20 Module 4 Lesson 17 Lesson 17

... The depreciation expense for that period is recorded and the book value of the asset is figured. Study the two examples on pages 650 to 652 in the textbook. Book value is the original asset cost less accumulated depreciation. In the example on page 652, the book value is calculated as $700 less $120 ...

... The depreciation expense for that period is recorded and the book value of the asset is figured. Study the two examples on pages 650 to 652 in the textbook. Book value is the original asset cost less accumulated depreciation. In the example on page 652, the book value is calculated as $700 less $120 ...

Management control systems. Literature

... sacrifice resulting from the use of assets. The evolution of MCS can be also assessed on historical grounds. Before the Second World War the primary focus of internal accounting was the determination of costs, with particular emphasis on product costing and the control of direct labor, direct materi ...

... sacrifice resulting from the use of assets. The evolution of MCS can be also assessed on historical grounds. Before the Second World War the primary focus of internal accounting was the determination of costs, with particular emphasis on product costing and the control of direct labor, direct materi ...

J. Lee Nicholson

Jerome Lee (J. Lee) Nicholson (1863 - November 2, 1924) was an American accountant, industrial consultant, author and educator at the New York University and Columbia University, known as pioneer in cost accounting. He is considered in the United States to be the ""father of cost accounting.""Nicholson most important contributions to cost accounting consisted of ""emphasizing cost centres and the measuring of profits for individual departments based on machine hour rates. Furthermore, he was instrumental in organizing the National Organization of Cost Accountants (later, the Institute of Management Accountants).""