FREE Sample Here - We can offer most test bank and

... a) Direct materials must become a physical part of the finished product and their costs must be separately and conveniently traceable through the manufacturing process to finished goods inventory. Examples include wood, leather, steel, etc. Indirect materials become part of the finished product but ...

... a) Direct materials must become a physical part of the finished product and their costs must be separately and conveniently traceable through the manufacturing process to finished goods inventory. Examples include wood, leather, steel, etc. Indirect materials become part of the finished product but ...

Chapter 5 Merchandising Operations

... What Are the Merchandising Operations? Merchandising consists of buying and selling products rather than the services. Merchandisers have some new balance sheet and income statement items. ...

... What Are the Merchandising Operations? Merchandising consists of buying and selling products rather than the services. Merchandisers have some new balance sheet and income statement items. ...

Intermediate Accounting - McGraw Hill Higher Education

... which may then be allocated to inventory General and administrative (G&A) expenses are normally treated as period expenses because they relate more directly to accounting periods than to inventory Distribution and selling costs are also considered to be period operating expenses and are not allocate ...

... which may then be allocated to inventory General and administrative (G&A) expenses are normally treated as period expenses because they relate more directly to accounting periods than to inventory Distribution and selling costs are also considered to be period operating expenses and are not allocate ...

chap.3 - HCC Learning Web

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

DMO Cost Principles - Department of Defence

... The Capability Acquisition & Sustainment Group Cost Principles 2015, supports the Commonwealth’s objective to standardise the applicability and transparency of the cost basis used in Defence contracts. The document details the Cost Principles that Defence and Industry will utilise towards contract c ...

... The Capability Acquisition & Sustainment Group Cost Principles 2015, supports the Commonwealth’s objective to standardise the applicability and transparency of the cost basis used in Defence contracts. The document details the Cost Principles that Defence and Industry will utilise towards contract c ...

Accounting for Rental Costs Incurred During the Constr

... the capitalization of certain costs incurred during construction of real estate projects to be sold or rented. Such costs include real estate property taxes and insurance and other project costs that are clearly associated with the acquisition, construction, and development of real estate projects. ...

... the capitalization of certain costs incurred during construction of real estate projects to be sold or rented. Such costs include real estate property taxes and insurance and other project costs that are clearly associated with the acquisition, construction, and development of real estate projects. ...

RAILROAD ACCOUNTING: ITS PROBLEMS AND THEIR EFFECT

... taxes to other accounts and/or other years when there are divergencies between the handling of major items of income or expense for tax purposes and for financial accounting purposes. 4. The acquisition adjustment account of the railroads comprises a variety of diverse elements* Under generally acce ...

... taxes to other accounts and/or other years when there are divergencies between the handling of major items of income or expense for tax purposes and for financial accounting purposes. 4. The acquisition adjustment account of the railroads comprises a variety of diverse elements* Under generally acce ...

section 300 financial management policies

... Bank Accounts ................................................................................................................. Accounts Receivable ........................................................................................................ Excess Costs .................................. ...

... Bank Accounts ................................................................................................................. Accounts Receivable ........................................................................................................ Excess Costs .................................. ...

Principles of Accounting I

... such as cash, land, accounts receivable, etc. Also there are various kinds of liability accounts such as accounts payable, taxes payable, etc. For our purposes now there are just two categories of owner’s equity accounts: (Capital) Paid In Capital and Retained Earnings. Note that revenue increases r ...

... such as cash, land, accounts receivable, etc. Also there are various kinds of liability accounts such as accounts payable, taxes payable, etc. For our purposes now there are just two categories of owner’s equity accounts: (Capital) Paid In Capital and Retained Earnings. Note that revenue increases r ...

Computerised Accounting System

... of information to various users at the same time on a real time basis (that is spontaneously). Automated Document Production : Most of the computerised accounting systems have standardised, user defined format of accounting reports that are generated automatically. The accounting reports such as Cas ...

... of information to various users at the same time on a real time basis (that is spontaneously). Automated Document Production : Most of the computerised accounting systems have standardised, user defined format of accounting reports that are generated automatically. The accounting reports such as Cas ...

GAAP

... concept is based on the accounting period concept. It is widely accepted that desire of making profit is the most important motivation to keep the proprietors engaged in business activities. By `matching’ we mean appropriate association of related revenues and expenses pertaining to a particular a ...

... concept is based on the accounting period concept. It is widely accepted that desire of making profit is the most important motivation to keep the proprietors engaged in business activities. By `matching’ we mean appropriate association of related revenues and expenses pertaining to a particular a ...

chapter 5 part 1

... accurate cost information on materials, labor, and overhead when making decisions. For example, when a construction company bills a client at set points throughout the construction, it is important that unit cost be generated in a timely manner. ...

... accurate cost information on materials, labor, and overhead when making decisions. For example, when a construction company bills a client at set points throughout the construction, it is important that unit cost be generated in a timely manner. ...

5 ACCOUNTING FOR

... We give a brief demonstration of the proper use of columnar paper and explain that all homework problems should be prepared in pencil. If the partially filled-in working papers are used (which we recommend), we show the students the worksheet for an extensive problem so that they will appreciate the ...

... We give a brief demonstration of the proper use of columnar paper and explain that all homework problems should be prepared in pencil. If the partially filled-in working papers are used (which we recommend), we show the students the worksheet for an extensive problem so that they will appreciate the ...

ANNEX Section 1. Cost accounting and accounting

... gather accounting separation information in respect of non-SMP markets only insofar as an NRA can justify that the provision of such information is necessary for the NRA to carry out its responsibilities under other provisions of the framework. Accounting separation requirements could be developed s ...

... gather accounting separation information in respect of non-SMP markets only insofar as an NRA can justify that the provision of such information is necessary for the NRA to carry out its responsibilities under other provisions of the framework. Accounting separation requirements could be developed s ...

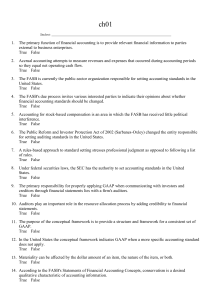

1. The primary function of financial accounting is

... . purchase method of accounting for the combination. B The negative effects on subsequent earnings of amortizing goodwill if firms were required to use the . pooling method of accounting for the combination. C The unrealistic balance sheet assets that would be created if firms were required to use t ...

... . purchase method of accounting for the combination. B The negative effects on subsequent earnings of amortizing goodwill if firms were required to use the . pooling method of accounting for the combination. C The unrealistic balance sheet assets that would be created if firms were required to use t ...

Class Coursepack - NC State University

... Selecting a Form of Business Ownership --------------------------------The Role of Accounting in Business --------------------------------------The Cash Basis of Accounting ---------------------------------------------The Accrual Basis of Accounting -----------------------------------------Introduct ...

... Selecting a Form of Business Ownership --------------------------------The Role of Accounting in Business --------------------------------------The Cash Basis of Accounting ---------------------------------------------The Accrual Basis of Accounting -----------------------------------------Introduct ...

Fixed Asset Policy

... Fixed Assets: Tangible assets acquired, purchased, constructed, or donated for use in operations and not for investment or sale. Their useful life is larger than two years, they retain their individual identity (including all component parts) throughout their useful life and meet the thresholds list ...

... Fixed Assets: Tangible assets acquired, purchased, constructed, or donated for use in operations and not for investment or sale. Their useful life is larger than two years, they retain their individual identity (including all component parts) throughout their useful life and meet the thresholds list ...

Unit F011 - Accounting principles - Scheme of work and

... Explain the terms cost, useful life and residual value ...

... Explain the terms cost, useful life and residual value ...

FREE Sample Here

... that it addressed only accounting’s transaction function. Rather, he saw accounting as encompassing other important functions, such as managerial control and the protection of the interests of equity holders. He also viewed accounting as having both an internal control function and an external funct ...

... that it addressed only accounting’s transaction function. Rather, he saw accounting as encompassing other important functions, such as managerial control and the protection of the interests of equity holders. He also viewed accounting as having both an internal control function and an external funct ...

What is Accounting? - masif-emba-fais-s12

... Careers with the IRS, the FBI, the SEC, and in public colleges and universities. ...

... Careers with the IRS, the FBI, the SEC, and in public colleges and universities. ...

Chapter 1 - Pearson Schools and FE Colleges

... In response, in 1971, the UK accounting bodies formed the Accounting Standards Committee (ASC) who issued many accounting standards known as Statements of Standard Accounting Practice (SSAPs). In 1990 the accountancy bodies replaced the ASC with the Accounting Standards Board (ASB) who issued furth ...

... In response, in 1971, the UK accounting bodies formed the Accounting Standards Committee (ASC) who issued many accounting standards known as Statements of Standard Accounting Practice (SSAPs). In 1990 the accountancy bodies replaced the ASC with the Accounting Standards Board (ASB) who issued furth ...

Glossary - Cengage

... Debt ratio The ratio that measures the percentage of a company's risk as the percentage of its assets financed by creditors increases. It is computed by dividing a company's total liabilities by its total assets. Decentralization The granting of decision-making freedom to lower operating levels. Dec ...

... Debt ratio The ratio that measures the percentage of a company's risk as the percentage of its assets financed by creditors increases. It is computed by dividing a company's total liabilities by its total assets. Decentralization The granting of decision-making freedom to lower operating levels. Dec ...

the relevance of auditing in a computerized accounting system

... accounting system is tedious and time consuming, it offers some benefits. The ledgers are easy to review, and Accountants can make simple changes if necessary; individual accounts are easily reconciled because information is in a systematic order through each ledger. Accountants also have the benefi ...

... accounting system is tedious and time consuming, it offers some benefits. The ledgers are easy to review, and Accountants can make simple changes if necessary; individual accounts are easily reconciled because information is in a systematic order through each ledger. Accountants also have the benefi ...

4.2.2 Standard Costing - College of Education and External Studies

... Some have even gone to the extent of making losses while others are continuously making losses. In the coca cola company, despite using the same cost controlling techniques, the value of profits keep changing that is, either higher or lower. I would like to find out if there is any relationship betw ...

... Some have even gone to the extent of making losses while others are continuously making losses. In the coca cola company, despite using the same cost controlling techniques, the value of profits keep changing that is, either higher or lower. I would like to find out if there is any relationship betw ...

J. Lee Nicholson

Jerome Lee (J. Lee) Nicholson (1863 - November 2, 1924) was an American accountant, industrial consultant, author and educator at the New York University and Columbia University, known as pioneer in cost accounting. He is considered in the United States to be the ""father of cost accounting.""Nicholson most important contributions to cost accounting consisted of ""emphasizing cost centres and the measuring of profits for individual departments based on machine hour rates. Furthermore, he was instrumental in organizing the National Organization of Cost Accountants (later, the Institute of Management Accountants).""