Postage Stamp Rates - Province of British Columbia

... pooled across the province but actual customer rates vary by rate class based on how much it costs to serve each class, known as the Fully Allocated Cost of Service. There are price discrepancies between rate classes where some customers are subsidized by others. For example, residential customers c ...

... pooled across the province but actual customer rates vary by rate class based on how much it costs to serve each class, known as the Fully Allocated Cost of Service. There are price discrepancies between rate classes where some customers are subsidized by others. For example, residential customers c ...

Break-even point

... • Is there another customer who would pay more for spare capacity rather than ‘selling it off’ cheaply • Potential loss of customer goodwill as a result of selling the same product at different prices • It may be better to reduce total capacity and thereby reduce fixed costs, if inability to sell fu ...

... • Is there another customer who would pay more for spare capacity rather than ‘selling it off’ cheaply • Potential loss of customer goodwill as a result of selling the same product at different prices • It may be better to reduce total capacity and thereby reduce fixed costs, if inability to sell fu ...

The economic benefits of net metering vary significantly

... The economic benefits of net metering vary significantly based upon the test applied, the state / utility analyzed, and the assumptions regarding long run avoided costs. Significant drivers of the analysis include the electric rates avoided by the customer with net metering, assumptions regarding lo ...

... The economic benefits of net metering vary significantly based upon the test applied, the state / utility analyzed, and the assumptions regarding long run avoided costs. Significant drivers of the analysis include the electric rates avoided by the customer with net metering, assumptions regarding lo ...

ECON 201- - WordPress.com

... • Decision Option 1: The company should not sell the drug. You don’t sell something for $30,000 a year when it cost $10m to make it. • Option 2: The company should go ahead and sell the drug. If they don’t, they would be wasting that huge investment of $10m. • Economist’s Response: Neither approach ...

... • Decision Option 1: The company should not sell the drug. You don’t sell something for $30,000 a year when it cost $10m to make it. • Option 2: The company should go ahead and sell the drug. If they don’t, they would be wasting that huge investment of $10m. • Economist’s Response: Neither approach ...

Fixed Costs

... organization’s departments are performing. Managers can also use CVP analysis to measure the effects of alternative courses of action, such as changing variable or fixed costs, expanding or contracting sales volume, and increasing or decreasing selling prices. ...

... organization’s departments are performing. Managers can also use CVP analysis to measure the effects of alternative courses of action, such as changing variable or fixed costs, expanding or contracting sales volume, and increasing or decreasing selling prices. ...

learning objectives

... department & assigning costs to products. 3. Understand how Work-in-Process account both describes transformation of inputs into outputs & accounts for costs incurred. 4. Compare & contrast normal & actual costing. 5. Know various production methods & different accounting systems each requires. Cont ...

... department & assigning costs to products. 3. Understand how Work-in-Process account both describes transformation of inputs into outputs & accounts for costs incurred. 4. Compare & contrast normal & actual costing. 5. Know various production methods & different accounting systems each requires. Cont ...

Basic Fixed-Order Quantity Models Multi

... • Inventory is the stock of any item or resource used in an organization and can include: raw materials, finished products, component parts, supplies, and work-in-process • An inventory system is the set of policies and controls that monitor levels of inventory and determines what levels should be m ...

... • Inventory is the stock of any item or resource used in an organization and can include: raw materials, finished products, component parts, supplies, and work-in-process • An inventory system is the set of policies and controls that monitor levels of inventory and determines what levels should be m ...

Answer to Worksheet–Optimization Business Application

... Answer: The total profit function is given by P = xp − C = 5x − 0.001x2 − (35 + 1.5x) = 3.5x − 0.001x2 − 35 ⇒ P 0 = 3.5 − 0.002x ...

... Answer: The total profit function is given by P = xp − C = 5x − 0.001x2 − (35 + 1.5x) = 3.5x − 0.001x2 − 35 ⇒ P 0 = 3.5 − 0.002x ...

The timecard/labor ticket is keyed and verified into the production

... unique use a job-order costing system1. This is the case when a company manufactures goods to a customer’s unique specifications. Companies using job-order systems include construction companies, producers of equipment and tools, shipbuilding companies, and printing companies. In the context of job- ...

... unique use a job-order costing system1. This is the case when a company manufactures goods to a customer’s unique specifications. Companies using job-order systems include construction companies, producers of equipment and tools, shipbuilding companies, and printing companies. In the context of job- ...

introduction

... management decisions because the decisions are based on contribution margin rather than product costs. By subtracting the relevant fixed costs from the contribution margin, different contribution margins or different layers can be obtained. Example: If there are fixed Research and Development or Adv ...

... management decisions because the decisions are based on contribution margin rather than product costs. By subtracting the relevant fixed costs from the contribution margin, different contribution margins or different layers can be obtained. Example: If there are fixed Research and Development or Adv ...

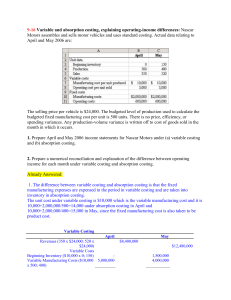

9-16 Variable and absorption costing, explaining

... 9-16 Variable and absorption costing, explaining operating-income differences: Nascar Motors assembles and sells motor vehicles and uses standard costing. Actual data relating to April and May 2006 are: ...

... 9-16 Variable and absorption costing, explaining operating-income differences: Nascar Motors assembles and sells motor vehicles and uses standard costing. Actual data relating to April and May 2006 are: ...

Seri Pekatan Sdn Bhd

... When Seri Pekatan was opened back in 1998, there was only two workers that are employed. When Seri Pekatan opened its own factory in Lambak in 2001, there was a positive increase in the human resources. Now there are almost 50 employees under Seri Pekatan Sdn Bhd. Most workers that are employed ...

... When Seri Pekatan was opened back in 1998, there was only two workers that are employed. When Seri Pekatan opened its own factory in Lambak in 2001, there was a positive increase in the human resources. Now there are almost 50 employees under Seri Pekatan Sdn Bhd. Most workers that are employed ...

office of management and budget (omb)

... Allocable to Federal awards Not prohibited under State or local laws or regulations Be accorded consistent treatment. (i.e., direct versus indirect costs) ...

... Allocable to Federal awards Not prohibited under State or local laws or regulations Be accorded consistent treatment. (i.e., direct versus indirect costs) ...

INTERNATIONAL PRICING STRATEGY

... pricing would be dictated by such factors as: - competitive conditions - life style - position of the product - product diffusion process - regulatory considerations ...

... pricing would be dictated by such factors as: - competitive conditions - life style - position of the product - product diffusion process - regulatory considerations ...

Cost Effective Drainage Structures

... ALUMINUM- Aluminum pipe is usually affected more by soil-side corrosion than by corrosion of the invert. Long-term performance is difficult to predict because of a relatively short history of use, but the designer should not expect a product service life of greater than 50 years. ...

... ALUMINUM- Aluminum pipe is usually affected more by soil-side corrosion than by corrosion of the invert. Long-term performance is difficult to predict because of a relatively short history of use, but the designer should not expect a product service life of greater than 50 years. ...

chapter 4

... 3. Traditionally, a single driver (e.g., direct labor hours, or direct labor costs, or machine hours) was used to establish predetermined overhead rates. However, many alternative activity bases are available that can improve management information and enhance the competitive advantage of an organiz ...

... 3. Traditionally, a single driver (e.g., direct labor hours, or direct labor costs, or machine hours) was used to establish predetermined overhead rates. However, many alternative activity bases are available that can improve management information and enhance the competitive advantage of an organiz ...

Chapter 13

... – Would not accept Lottery if all-equity financed firm – Would not accept Lottery if company was a partnership; limited liability means B/Hs have no recourse to S/Hs ...

... – Would not accept Lottery if all-equity financed firm – Would not accept Lottery if company was a partnership; limited liability means B/Hs have no recourse to S/Hs ...

Basic Management Accounting Concepts Chapter 2

... statement for the month of July was completed and shown on Cornerstone 26. REQUIRED: Prepare an income statement for BlueDenim for the month of July. Calculation: Income statement appears on the next slide. Every item is divided by Sales , i.e., Sales; 792,000 / 792,000 = 100.0%, Cost of goods sold; ...

... statement for the month of July was completed and shown on Cornerstone 26. REQUIRED: Prepare an income statement for BlueDenim for the month of July. Calculation: Income statement appears on the next slide. Every item is divided by Sales , i.e., Sales; 792,000 / 792,000 = 100.0%, Cost of goods sold; ...

Chapter 3 – CVP

... 3) Target Pricing / Target Costing (Market-based strategy): Market sales price less desired profit = allowable cost. D) Margin of Safety (Pg 120/121 & H/W E3-11A): 1) How far can sales fall prior to Break-Even? 2) Two-step process: Calculate B/E first, then compare to expected sales volume to dete ...

... 3) Target Pricing / Target Costing (Market-based strategy): Market sales price less desired profit = allowable cost. D) Margin of Safety (Pg 120/121 & H/W E3-11A): 1) How far can sales fall prior to Break-Even? 2) Two-step process: Calculate B/E first, then compare to expected sales volume to dete ...

Chapter 20

... typically use job order costing. – A job order costing system traces the costs of direct materials, direct labor, and overhead to a specific batch of products or a specific job order. (cont.) • A job order cost card is the document on which all costs incurred in the production of a particular job or ...

... typically use job order costing. – A job order costing system traces the costs of direct materials, direct labor, and overhead to a specific batch of products or a specific job order. (cont.) • A job order cost card is the document on which all costs incurred in the production of a particular job or ...

Example - McGraw Hill Higher Education

... Least-squares regression also provides a statistic, called the R2, which is a measure of the goodness of fit of the regression line to the data points. ...

... Least-squares regression also provides a statistic, called the R2, which is a measure of the goodness of fit of the regression line to the data points. ...

Budget Justification Form

... disks, general-purpose software and site licenses (e.g., Word, Excel, GroupWise, etc.). Please see Costing Policies for more details. Local Telephone Costs Local telephone costs (defined as all expenses other than long distance calls) are not allowable as direct costs on federal/federal flow-through ...

... disks, general-purpose software and site licenses (e.g., Word, Excel, GroupWise, etc.). Please see Costing Policies for more details. Local Telephone Costs Local telephone costs (defined as all expenses other than long distance calls) are not allowable as direct costs on federal/federal flow-through ...