fixed cost

... Manager’s choice of product mix, design, quality, features, distribution, and so on, influence product and service costs. These decisions should be made in a cost/benefit framework. ...

... Manager’s choice of product mix, design, quality, features, distribution, and so on, influence product and service costs. These decisions should be made in a cost/benefit framework. ...

PROBLEMS ON ACCEPT OR REJECT SPECIAL ORDER DECISION

... c) Assume that 75 percent of the variable marketing costs can be eliminated. What would be the effect on the net income from accepting this order?(TU 2046) P – 12. The Kathmandu Product Ltd.; a company engaged in production of specialized goods called ‘Kath Craft’ has been utilizing its capacity onl ...

... c) Assume that 75 percent of the variable marketing costs can be eliminated. What would be the effect on the net income from accepting this order?(TU 2046) P – 12. The Kathmandu Product Ltd.; a company engaged in production of specialized goods called ‘Kath Craft’ has been utilizing its capacity onl ...

Manufacturing Accounting

... 1. Prepare a statement of cost of good manufactured. The statement of cost of goods manufactured includes the beginning work-in-process inventory, plus the cost of raw materials used, plus direct labor, plus factory overhead, less the ending work-in-process inventory. 2. Complete a work sheet for a ...

... 1. Prepare a statement of cost of good manufactured. The statement of cost of goods manufactured includes the beginning work-in-process inventory, plus the cost of raw materials used, plus direct labor, plus factory overhead, less the ending work-in-process inventory. 2. Complete a work sheet for a ...

Unit 10 Management Accounting

... name manufacturing businesses that they know of. Ask them what makes these businesses different from a retail business. Introduce the concepts of the three inventories: raw materials, work-in-process, and finished goods. Have students recall the calculation of ending inventory in the multi-step inco ...

... name manufacturing businesses that they know of. Ask them what makes these businesses different from a retail business. Introduce the concepts of the three inventories: raw materials, work-in-process, and finished goods. Have students recall the calculation of ending inventory in the multi-step inco ...

Inventory Management: Economic Order Quantity

... Theory of Constraints Five-Step Method for Improving Performance • Identify an organization’s constraints. • Exploit the binding constraints. • Subordinate everything else to the decisions made in Step 2. • Elevate the organization’s binding constraints. • Repeat the process as a new constraint eme ...

... Theory of Constraints Five-Step Method for Improving Performance • Identify an organization’s constraints. • Exploit the binding constraints. • Subordinate everything else to the decisions made in Step 2. • Elevate the organization’s binding constraints. • Repeat the process as a new constraint eme ...

1 of 2 generic companies vertically integrated from API to finished

... This presentation contains references to non-GAAP financial measures, including Adjusted operating income, which are financial measures that are not prepared in conformity with accounting principles generally accepted in the United States (GAAP). Adjusted operating income is adjusted to exclude, amo ...

... This presentation contains references to non-GAAP financial measures, including Adjusted operating income, which are financial measures that are not prepared in conformity with accounting principles generally accepted in the United States (GAAP). Adjusted operating income is adjusted to exclude, amo ...

ACCT - Accounting Department

... 3. Explain the opportunity-cost concept and wh it is used in decision making. 4. Know how to choose which products to produce when there are capacity constraints. 5. Discuss factors managers must consider when adding or dropping customers or segments. 6. Explain why book value of equipment is irrele ...

... 3. Explain the opportunity-cost concept and wh it is used in decision making. 4. Know how to choose which products to produce when there are capacity constraints. 5. Discuss factors managers must consider when adding or dropping customers or segments. 6. Explain why book value of equipment is irrele ...

Stamford University Bangladesh MBA Program Cost and

... Finished goods inventory, beginning............... $ 50,000 Add: Cost of goods manufactured .................. 690,000 * Goods available for sale (given) ..................... 740,000 Deduct: Finished goods inventory, ending....... 80,000 * Cost of goods sold (given) ............................. $6 ...

... Finished goods inventory, beginning............... $ 50,000 Add: Cost of goods manufactured .................. 690,000 * Goods available for sale (given) ..................... 740,000 Deduct: Finished goods inventory, ending....... 80,000 * Cost of goods sold (given) ............................. $6 ...

Applications of functions to economics

... Problem 1. Suppose that the radio manufacture has a machine that costs $15,000 and is sold ten years later for $5,000. We say the value of the machine depreciates from $15,000 today to resale value of $5,000 in ten years. The depreciation formula gives the value, V (t), in dollars, of the machine as ...

... Problem 1. Suppose that the radio manufacture has a machine that costs $15,000 and is sold ten years later for $5,000. We say the value of the machine depreciates from $15,000 today to resale value of $5,000 in ten years. The depreciation formula gives the value, V (t), in dollars, of the machine as ...

Class Lecture 3: Continuation of Cost Terms - Md.ahsan

... The work of management focuses on (1) planning, which includes setting objectives and outlining how to attain these objectives (2) control, which includes the steps to take to ensure that objectives are realized. To carry out these planning and control responsibilities, managers need information abo ...

... The work of management focuses on (1) planning, which includes setting objectives and outlining how to attain these objectives (2) control, which includes the steps to take to ensure that objectives are realized. To carry out these planning and control responsibilities, managers need information abo ...

environmental accounting: emerging issues of theory

... systematic analysis of business operations and processes is undertaken, it generally becomes clear that environmental costs are a far greater percentage of total costs than had been realised. Typically, this underestimation is a consequence of lazy accounting practice. Overhead accounts become gener ...

... systematic analysis of business operations and processes is undertaken, it generally becomes clear that environmental costs are a far greater percentage of total costs than had been realised. Typically, this underestimation is a consequence of lazy accounting practice. Overhead accounts become gener ...

Chapter 11. Rebuilding the American Economy

... emotionally, and psychologically as those who lived in Catal Hüyük in 6,000 BC, or those who first came to California 30,000 years ago. Yet now there are 6.7 billion people on Earth, and the environment is less rich and abundant than it was during either period. For as long as humankind has been on ...

... emotionally, and psychologically as those who lived in Catal Hüyük in 6,000 BC, or those who first came to California 30,000 years ago. Yet now there are 6.7 billion people on Earth, and the environment is less rich and abundant than it was during either period. For as long as humankind has been on ...

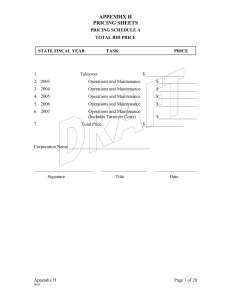

PRICING SCHEDULE A

... Other 1 ____________________________________ Other 2 ____________________________________ Other 3 ____________________________________ ...

... Other 1 ____________________________________ Other 2 ____________________________________ Other 3 ____________________________________ ...

Analysis and Interpretation of Financial Statements

... Break even point-the point at which a company makes neither a profit or a loss. Contribution per unit-the sales price minus the variable cost per unit. It measures the contribution made by each item of output to the fixed costs and profit of the organisation. Margin of safety-a measure in which the ...

... Break even point-the point at which a company makes neither a profit or a loss. Contribution per unit-the sales price minus the variable cost per unit. It measures the contribution made by each item of output to the fixed costs and profit of the organisation. Margin of safety-a measure in which the ...

Costs

... If general fixed costs are changed by making a choice over alternatives, these costs will be relevant for decision making. If general fixed costs increase as a result of a decision, this increase represents an incremental cost. Example: extra rent for a bigger factory to producing an additional prod ...

... If general fixed costs are changed by making a choice over alternatives, these costs will be relevant for decision making. If general fixed costs increase as a result of a decision, this increase represents an incremental cost. Example: extra rent for a bigger factory to producing an additional prod ...

Chapter 7 - Kennisbanksu

... s Manufacturing overhead includes the cost of manufacturing support departments s Includes the cost of indirect material and indirect labour s Non-manufacturing costs are all costs incurred outside of manufacturing Ù May be included in product costs for use in internal product-related decisions, but ...

... s Manufacturing overhead includes the cost of manufacturing support departments s Includes the cost of indirect material and indirect labour s Non-manufacturing costs are all costs incurred outside of manufacturing Ù May be included in product costs for use in internal product-related decisions, but ...

Marginal Costing vs. Absorption Costing Revision

... - fixed costs do not remain fixed at all levels of output (for example if extra premises are needed). • The assumption that all output is sold may not be true. • The presumption that there is only one product may not be correct. • External factors (such as rate of inflation) are not considered. Mr. ...

... - fixed costs do not remain fixed at all levels of output (for example if extra premises are needed). • The assumption that all output is sold may not be true. • The presumption that there is only one product may not be correct. • External factors (such as rate of inflation) are not considered. Mr. ...

Notes

... I. Price, the second "P"— it is the sum of all the values that consumers exchange for benefits of having the product/service. § It has been the major factor affecting buyer choice. § But nonprice ...

... I. Price, the second "P"— it is the sum of all the values that consumers exchange for benefits of having the product/service. § It has been the major factor affecting buyer choice. § But nonprice ...

null

... Weighted Average Revenue (.90 × $0.60 for prints) + (.10 × $1.00 for enlargements) = $ .64 ...

... Weighted Average Revenue (.90 × $0.60 for prints) + (.10 × $1.00 for enlargements) = $ .64 ...

Idle Capacity Costs: It Isn`t Just the Expense

... brand image—an intangible asset that the current accounting system ignores. Brand image is important to companies and investors to the extent that it translates into company value and share price. Even as current price discounting affects brand image negatively, it also affects a company’s current p ...

... brand image—an intangible asset that the current accounting system ignores. Brand image is important to companies and investors to the extent that it translates into company value and share price. Even as current price discounting affects brand image negatively, it also affects a company’s current p ...

Marginal costing

... Theory of constraints (TOC) and Throughput accounting (TA) Theory of constraint is an approach to production management, which aims to maximize sales revenue less material and minimize variable overhead cost. It focus on factors such as bottle necks which act as constraints to maximization. Bottlene ...

... Theory of constraints (TOC) and Throughput accounting (TA) Theory of constraint is an approach to production management, which aims to maximize sales revenue less material and minimize variable overhead cost. It focus on factors such as bottle necks which act as constraints to maximization. Bottlene ...

Capitalization and Depreciation of Property, Plant, and Equipment

... The capitalized costs of interest during construction for debt-financed projects are the costs of interest related to the acquisition or construction of an asset. The interest costs can be capitalized during the period of time that is required to complete and prepare the asset for its intended use. ...

... The capitalized costs of interest during construction for debt-financed projects are the costs of interest related to the acquisition or construction of an asset. The interest costs can be capitalized during the period of time that is required to complete and prepare the asset for its intended use. ...

Marketing Decision Making

... What about marketing territory info? Pricing? Credit Department: Look at keeping costs down. Bad debt. ...

... What about marketing territory info? Pricing? Credit Department: Look at keeping costs down. Bad debt. ...

a critical analysis of today`s accounting and cost calculation system

... the generated value on the market of the products and services and the capital market in the interest of all the interested factors (stockholder, employees, clients, community in general etc.) - the concept regarding the business process of the enterprise it is under the conditions in which the man ...

... the generated value on the market of the products and services and the capital market in the interest of all the interested factors (stockholder, employees, clients, community in general etc.) - the concept regarding the business process of the enterprise it is under the conditions in which the man ...