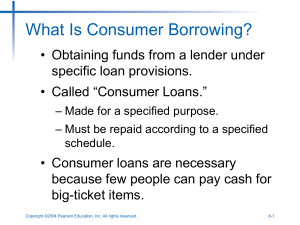

Loan Intrest

... • Focus on Ethics: Predatory Lending – Beware of illegal lending practices • Lender charging high loan fees • Lender provides home equity loan with the expectation of default so he can take ownership • Lender ties other products to loan approval ...

... • Focus on Ethics: Predatory Lending – Beware of illegal lending practices • Lender charging high loan fees • Lender provides home equity loan with the expectation of default so he can take ownership • Lender ties other products to loan approval ...

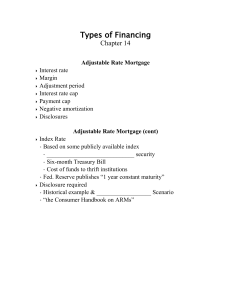

Adjustable Rate Mortgage

... Adjustment period Interest rate cap Payment cap Negative amortization Disclosures Adjustable Rate Mortgage (cont) ...

... Adjustment period Interest rate cap Payment cap Negative amortization Disclosures Adjustable Rate Mortgage (cont) ...

Digital Loan Marketplace

... Over the past ten years, spurred by the financial crisis and technological innovation, the process by which most mortgage loans are priced has changed dramatically. This new reality has demanded that lenders examine legacy processes to remain compliant and competitive. Today, lenders increasingly re ...

... Over the past ten years, spurred by the financial crisis and technological innovation, the process by which most mortgage loans are priced has changed dramatically. This new reality has demanded that lenders examine legacy processes to remain compliant and competitive. Today, lenders increasingly re ...

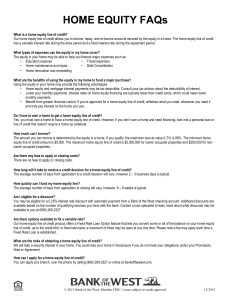

HOME EQUITY FAQs - Bank of the West

... • Benefit from greater financial control. If you’re approved for a home equity line of credit, withdraw what you need, whenever you need it and only pay interest on the funds you use. Do I have to own a home to get a home equity line of credit? Yes, you must own a home to have a home equity line of ...

... • Benefit from greater financial control. If you’re approved for a home equity line of credit, withdraw what you need, whenever you need it and only pay interest on the funds you use. Do I have to own a home to get a home equity line of credit? Yes, you must own a home to have a home equity line of ...

Adequate explanations

... • Existing Offer document will be used as the Binding Offer with a 10-day Reflection Period • Receipt of COT from solicitor waives reflection period ...

... • Existing Offer document will be used as the Binding Offer with a 10-day Reflection Period • Receipt of COT from solicitor waives reflection period ...

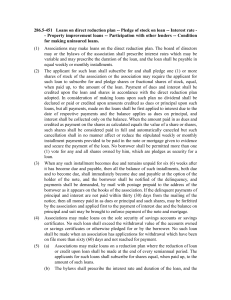

286.5-451 Loans on direct reduction plan -

... declared or paid or credited upon amounts credited as dues or principal upon such loans, but all payments, made on the loans shall be first applied to interest due to the date of respective payments and the balance applies as dues on principal, and interest shall be collected only on the balance. Wh ...

... declared or paid or credited upon amounts credited as dues or principal upon such loans, but all payments, made on the loans shall be first applied to interest due to the date of respective payments and the balance applies as dues on principal, and interest shall be collected only on the balance. Wh ...

how to avoid the pitfalls of the commercial mortgage application

... commercial mortgages since there is a maximum loan amount of $2-3 million for most Stated Income Commercial Mortgage Programs. 3. The third reason a commercial loan may be declined is due to property type or special requirements imposed that make the loan impractical for the commercial borrower. Not ...

... commercial mortgages since there is a maximum loan amount of $2-3 million for most Stated Income Commercial Mortgage Programs. 3. The third reason a commercial loan may be declined is due to property type or special requirements imposed that make the loan impractical for the commercial borrower. Not ...

Amendment

... • Willingness and ability to align loan-making with OEDIT strategies and programs such as CDBG revolving loan funds, outdoor recreation and tourism offices, SBDC, Minority Business Office (MBO), Advanced Industries, Creative Districts and Creative Industries Programs, Historic Preservation Tax Credi ...

... • Willingness and ability to align loan-making with OEDIT strategies and programs such as CDBG revolving loan funds, outdoor recreation and tourism offices, SBDC, Minority Business Office (MBO), Advanced Industries, Creative Districts and Creative Industries Programs, Historic Preservation Tax Credi ...

assisting the start-up and growing business

... neither afford to maintain high balances on deposit which are a source of profits for institutional lenders, nor can they purchase many ancillary products from the bank such as payroll or investment services. Thus, financing small businesses is perceived as high risk and low reward. In an effort to ...

... neither afford to maintain high balances on deposit which are a source of profits for institutional lenders, nor can they purchase many ancillary products from the bank such as payroll or investment services. Thus, financing small businesses is perceived as high risk and low reward. In an effort to ...

English

... that it is anticipated that they will collect deposits from a large number of unspecified people, making it necessary to protect these depositors, they act as local financial institutions in providing credit to local residents and businesses, and it is essential to maintain their sound management, b ...

... that it is anticipated that they will collect deposits from a large number of unspecified people, making it necessary to protect these depositors, they act as local financial institutions in providing credit to local residents and businesses, and it is essential to maintain their sound management, b ...

Tightest Credit Market in 16 Years Rejects Bernanke`s Bid

... James Bregenzer, a 31-year-old marketing strategist in Chicago, was rejected for a mortgage in May after successfully financing two previous home purchases. The hitch this time: his monthly payment would have been $100 more than the lender was willing to approve. Bregenzer is in good company. Standa ...

... James Bregenzer, a 31-year-old marketing strategist in Chicago, was rejected for a mortgage in May after successfully financing two previous home purchases. The hitch this time: his monthly payment would have been $100 more than the lender was willing to approve. Bregenzer is in good company. Standa ...

presentation

... We have information on whether the loan volume has decreased during negotiations (likely first step). During crisis, slight increase compared to normal times but still < 1% of loans ...

... We have information on whether the loan volume has decreased during negotiations (likely first step). During crisis, slight increase compared to normal times but still < 1% of loans ...

- Seckman High School

... purchase of a house. • Ten to thirty years of payments • Fixed or adjustable rate (ARM) • Balloon payments, large amount at the end, can reduce the monthly payments • Closing costs—expenses the buyer pays in order to get the loan. Personal Finance ...

... purchase of a house. • Ten to thirty years of payments • Fixed or adjustable rate (ARM) • Balloon payments, large amount at the end, can reduce the monthly payments • Closing costs—expenses the buyer pays in order to get the loan. Personal Finance ...

CUTTING THROUGH THE JARGON: A Basic Primer on

... accordance with a Waterfall (see below). Mezzanine Loans typically refers to secondary financing on a project, similar in purpose to a second mortgage, except that a mezzanine loan is secured by the equity interests of the company that owns the property, as opposed to the real estate. If the company ...

... accordance with a Waterfall (see below). Mezzanine Loans typically refers to secondary financing on a project, similar in purpose to a second mortgage, except that a mezzanine loan is secured by the equity interests of the company that owns the property, as opposed to the real estate. If the company ...

Word Wall Words

... finance charge- The total cost of using credit, including interest and any fees. credit score- A numerical rating, based on credit report information, that represents a person’s level of creditworthiness. cosigner- A person with a strong established credit history who signs the credit application an ...

... finance charge- The total cost of using credit, including interest and any fees. credit score- A numerical rating, based on credit report information, that represents a person’s level of creditworthiness. cosigner- A person with a strong established credit history who signs the credit application an ...

Debt Financing in a Challenging Regulatory and Market Environment

... Less competition from CMBS lenders and higher demand for bank and life company money. Life companies will likely get through most of their allocations by late summer ...

... Less competition from CMBS lenders and higher demand for bank and life company money. Life companies will likely get through most of their allocations by late summer ...

payment holiday - BondPlus Online

... consecutive repayments The additional funds will enable them to use the funds for an emergency, furnish their new home or use it for a holiday over the festive period. Example : Registration of a bond usually takes between 2 -3 months. If a client applies for a home loan and takes up the payment hol ...

... consecutive repayments The additional funds will enable them to use the funds for an emergency, furnish their new home or use it for a holiday over the festive period. Example : Registration of a bond usually takes between 2 -3 months. If a client applies for a home loan and takes up the payment hol ...

Applying for and Managing Loans

... loans to accept and how much to borrow. The subsidized loans with the lowest interest rates are the most desirable. Often students have no choice but to take all the loans they are offered in a given financial aid package, which is why careful comparison of financial aid offers is critical. The entr ...

... loans to accept and how much to borrow. The subsidized loans with the lowest interest rates are the most desirable. Often students have no choice but to take all the loans they are offered in a given financial aid package, which is why careful comparison of financial aid offers is critical. The entr ...

Presentation Title

... Is there an average credit score? According to Experian, the current national average credit score is…. ...

... Is there an average credit score? According to Experian, the current national average credit score is…. ...

Answers to Chapter 24 Questions

... Banks may sell the loans of less creditworthy borrowers, thereby raising required yields. Indeed, since commercial paper issuers tend to be well-known companies, information, monitoring, and credit assessment costs are lower for commercial paper issues than for loan sales. Moreover, since there is a ...

... Banks may sell the loans of less creditworthy borrowers, thereby raising required yields. Indeed, since commercial paper issuers tend to be well-known companies, information, monitoring, and credit assessment costs are lower for commercial paper issues than for loan sales. Moreover, since there is a ...

LAWS OF LOANS

... necessary for the lender to affirm that he is wholeheartedly releasing the debt; only afterwards is it praiseworthy for the borrower to say that "even so," he wants to return the money (Mishna Shevi'it 10:8-9.) It seems even more surprising that the Sages themselves provided a way to evade the relea ...

... necessary for the lender to affirm that he is wholeheartedly releasing the debt; only afterwards is it praiseworthy for the borrower to say that "even so," he wants to return the money (Mishna Shevi'it 10:8-9.) It seems even more surprising that the Sages themselves provided a way to evade the relea ...

Credit Risk: Individual Loan Risk Chapter 11

... • Decline in C&I loans originated by commercial banks. • RE loans: primarily mortgages » mortgages can be subject to default risk when loanto-value declines. ...

... • Decline in C&I loans originated by commercial banks. • RE loans: primarily mortgages » mortgages can be subject to default risk when loanto-value declines. ...

Advance America Compared to All Other

... A final argument made by opponents of payday lending is that consumers who utilize payday loans are systematically acting irrationally (Francis, 2010). This argument is favored by proponents of behavioral economics who believe that individuals do not always act rationally, face asymmetric informatio ...

... A final argument made by opponents of payday lending is that consumers who utilize payday loans are systematically acting irrationally (Francis, 2010). This argument is favored by proponents of behavioral economics who believe that individuals do not always act rationally, face asymmetric informatio ...

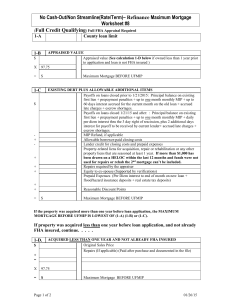

No Cash-Out/Non Streamline(Rate/Term)– Refinance Maximum

... VOM or other documentation is required which includes principal balance, date loan originated, names of original borrowers and type of loan. Other credit verifications are also required (VOE, VOD, etc.) There is no holding period. Acquisition could be a limiting factor. Max CLTV is 97.75. Borrower m ...

... VOM or other documentation is required which includes principal balance, date loan originated, names of original borrowers and type of loan. Other credit verifications are also required (VOE, VOD, etc.) There is no holding period. Acquisition could be a limiting factor. Max CLTV is 97.75. Borrower m ...

Payday loan

A payday loan (also called a payday advance, salary loan, payroll loan, small dollar loan, short term, or cash advance loan) is a small, short-term unsecured loan, ""regardless of whether repayment of loans is linked to a borrower's payday."" The loans are also sometimes referred to as ""cash advances,"" though that term can also refer to cash provided against a prearranged line of credit such as a credit card. Payday advance loans rely on the consumer having previous payroll and employment records. Legislation regarding payday loans varies widely between different countries and, within the USA, between different states.To prevent usury (unreasonable and excessive rates of interest), some jurisdictions limit the annual percentage rate (APR) that any lender, including payday lenders, can charge. Some jurisdictions outlaw payday lending entirely, and some have very few restrictions on payday lenders. In the United States, the rates of these loans were formerly restricted in most states by the Uniform Small Loan Laws (USLL), with 36%-40% APR generally the norm.There are many different ways to calculate annual percentage rate of a loan. Depending on which method is used, the rate calculated may differ dramatically. E.g., for a $15 charge on a $100 14-day payday loan, it could be (from the borrower's perspective) anywhere from 391% to 3733%.Although some have noted that these loans appear to carry substantial risk to the lender, it has recently been shown that these loans carry no more long term risk for the lender than other forms of credit. These studies seem to be confirmed by the SEC 10-K filings of at least one lender, who notes a charge-off rate of 3.2%.