Mortgage Loans

... money when you have the need. You may draw upon the account as long as you do not exceed the credit limit and are not in default. The amount of the monthly payment is based on the amount of credit you have used. Some lenders may charge a fee for the use of the line of credit. Home equity lines of cr ...

... money when you have the need. You may draw upon the account as long as you do not exceed the credit limit and are not in default. The amount of the monthly payment is based on the amount of credit you have used. Some lenders may charge a fee for the use of the line of credit. Home equity lines of cr ...

I. Debt around the world

... more developed debt and equity markets should provide better institutional conditions for structured products to grow. Credit side: From the credit side, there are three main groups of participants in this market: commercial banks, investment banks, and institutional investors. ...

... more developed debt and equity markets should provide better institutional conditions for structured products to grow. Credit side: From the credit side, there are three main groups of participants in this market: commercial banks, investment banks, and institutional investors. ...

justice foreclosed

... were people of color more likely to receive subprime loans, but the terms tended to be more predatory than those given to whites. Since the housing market collapsed, black homeowners are 76 percent more likely than white homeowners to have lost their home to foreclosure; the number for Latino homeow ...

... were people of color more likely to receive subprime loans, but the terms tended to be more predatory than those given to whites. Since the housing market collapsed, black homeowners are 76 percent more likely than white homeowners to have lost their home to foreclosure; the number for Latino homeow ...

CHAPTER 16, CREDIT IN AMERICA CREDIT

... currency exchange. Americans began to be dependent on one another. Sources of credit was needed to help families meet their financial needs. Consumer credit had begun. Earliest forms of credit was theaccount at the local general store. Banks lent farmers lump sums of money as large as $500 to put in ...

... currency exchange. Americans began to be dependent on one another. Sources of credit was needed to help families meet their financial needs. Consumer credit had begun. Earliest forms of credit was theaccount at the local general store. Banks lent farmers lump sums of money as large as $500 to put in ...

Project Finance Overview

... The solution to the potential inconsistency between the loan and ISDA agreements is relatively simple: (1) the events of default under the ISDA agreement should be disapplied as they relate to the borrower and (2) the events of default under the loan agreement should be incorporated by reference int ...

... The solution to the potential inconsistency between the loan and ISDA agreements is relatively simple: (1) the events of default under the ISDA agreement should be disapplied as they relate to the borrower and (2) the events of default under the loan agreement should be incorporated by reference int ...

View/Open

... Even though hire/purchase agreements are legally structured as rental agreements, they are equivalent to conventional installment loans. For example, a borrower may agree to make rental payments of 120 Rands per month for 12 months for a wardrobe with a cash price of 1,000 Rands. Although there is n ...

... Even though hire/purchase agreements are legally structured as rental agreements, they are equivalent to conventional installment loans. For example, a borrower may agree to make rental payments of 120 Rands per month for 12 months for a wardrobe with a cash price of 1,000 Rands. Although there is n ...

Current Challenges in Housing and Home Loans: Complicating Factors and

... unemployed homeowners with “negative equity,” foreclosure was often the only option. The more recent period also points to the importance of falling house prices and negative equity in foreclosures. In the more recent period (shown in Figures 6 and 7), the foreclosure rate – which was not particular ...

... unemployed homeowners with “negative equity,” foreclosure was often the only option. The more recent period also points to the importance of falling house prices and negative equity in foreclosures. In the more recent period (shown in Figures 6 and 7), the foreclosure rate – which was not particular ...

LCQ12: Measures to combat unscrupulous business practices of

... intermediaries which is a major issue of public concern, the Money Lenders Ordinance (Cap. 163) (MLO) expressly prohibits the charging of any fees on borrowers by money lenders, their connected parties (e.g. their employees, agents and persons acting for them) and persons acting in collusion with t ...

... intermediaries which is a major issue of public concern, the Money Lenders Ordinance (Cap. 163) (MLO) expressly prohibits the charging of any fees on borrowers by money lenders, their connected parties (e.g. their employees, agents and persons acting for them) and persons acting in collusion with t ...

English

... these cases the amount of interest you must pay can be very large. Simple Interest is calculated based on the loan amount. With simple interest problems we refer to the loan amount as the principal. The formula for calculating simple interest is given below. ...

... these cases the amount of interest you must pay can be very large. Simple Interest is calculated based on the loan amount. With simple interest problems we refer to the loan amount as the principal. The formula for calculating simple interest is given below. ...

What is Credit- Teacher Guide

... purchase of such things such as automobiles or household appliances. Sometimes their customers do not qualify for bank credit and therefore pay a higher rate of interest. • Department stores and other financial service providers sometimes offer their own credit cards for their customers’ use. 5. Ask ...

... purchase of such things such as automobiles or household appliances. Sometimes their customers do not qualify for bank credit and therefore pay a higher rate of interest. • Department stores and other financial service providers sometimes offer their own credit cards for their customers’ use. 5. Ask ...

statement on subprime mortgage lending

... borrowers based on limited or no documentation of income or imposing substantial prepayment penalties or prepayment penalty periods extending past the initial fixed interest rate period. Also, borrowers may not be adequately informed of product features and risks, such as their responsibility to pay ...

... borrowers based on limited or no documentation of income or imposing substantial prepayment penalties or prepayment penalty periods extending past the initial fixed interest rate period. Also, borrowers may not be adequately informed of product features and risks, such as their responsibility to pay ...

Credit Unions and Caisses Populaires SECTOR OUTLOOK 4Q16

... The proposed concept of “Lender Risk Sharing”, where lenders take on additional risk for insured mortgages, could be detrimental to borrowers as lenders may increase interest rates to pass on this risk as an additional cost to the borrowers, which will reduce the amount the prospective home buyer ca ...

... The proposed concept of “Lender Risk Sharing”, where lenders take on additional risk for insured mortgages, could be detrimental to borrowers as lenders may increase interest rates to pass on this risk as an additional cost to the borrowers, which will reduce the amount the prospective home buyer ca ...

financial prudential norms

... b) reporting date – the last day of the reporting period for which the association is submitting a financial statement to the National Commission on Financial Market (hereinafter – National Commission); c) group of members acting together means two or more members who are exposed to the same risk du ...

... b) reporting date – the last day of the reporting period for which the association is submitting a financial statement to the National Commission on Financial Market (hereinafter – National Commission); c) group of members acting together means two or more members who are exposed to the same risk du ...

Information Asymmetry in Syndicated Loans

... 2. The Determinants of Syndicate Structure and Loan Terms The structure of a loan syndicate is related to the information asymmetries between the lead arranger and the participants in the syndicate or between the lenders and the borrowers. The characteristics of the lead arrangers have been shown to ...

... 2. The Determinants of Syndicate Structure and Loan Terms The structure of a loan syndicate is related to the information asymmetries between the lead arranger and the participants in the syndicate or between the lenders and the borrowers. The characteristics of the lead arrangers have been shown to ...

Residential mortgage lending for underserved communities: recent

... upfront interest rate buy-down reduces the interest rate substantially, especially for WBHL℠ products with a rate step-up, as the buy-down only applies to the initial rate for those versions of the loan.10 Altogether, these factors allow the WBHL℠ to achieve a lower interest rate and higher equity c ...

... upfront interest rate buy-down reduces the interest rate substantially, especially for WBHL℠ products with a rate step-up, as the buy-down only applies to the initial rate for those versions of the loan.10 Altogether, these factors allow the WBHL℠ to achieve a lower interest rate and higher equity c ...

here - Reverse Market Insight

... Very popular for secondary mortgage market investors – makes LIBORindexed mortgage backed securities more liquid (easier to sell) Greater liquidity means lenders can offer lower margins to borrowers ...

... Very popular for secondary mortgage market investors – makes LIBORindexed mortgage backed securities more liquid (easier to sell) Greater liquidity means lenders can offer lower margins to borrowers ...

Financing Options for Your Small Business Guide

... entirely qualify for loans or investments through traditional lending institutions. They will participate with other lenders in providing financing and may take a second lien position on collateral. Loans amounts up to $500,000. They also fund some stand-alone loans up to ...

... entirely qualify for loans or investments through traditional lending institutions. They will participate with other lenders in providing financing and may take a second lien position on collateral. Loans amounts up to $500,000. They also fund some stand-alone loans up to ...

What does it mean? Common terms for home ownership factsheet

... Mortgage offset account - A savings account run in conjunction with a home loan. The interest earned on the account reduces the interest paid on the loan. A 100% offset is where the interest rates earned and paid are the same. A partial offset account is where the interest rate earned on the offset ...

... Mortgage offset account - A savings account run in conjunction with a home loan. The interest earned on the account reduces the interest paid on the loan. A 100% offset is where the interest rates earned and paid are the same. A partial offset account is where the interest rate earned on the offset ...

Handout(1)

... added to the balance owed on the card, along with any applicable interest payments and other finance charges Interest is generally higher than retail purchase balances APR for cash advance: 20.39% to 37.14% Administration fee/ handling fee: 1% to 4% (Source: Consumer Council, May 2013) ...

... added to the balance owed on the card, along with any applicable interest payments and other finance charges Interest is generally higher than retail purchase balances APR for cash advance: 20.39% to 37.14% Administration fee/ handling fee: 1% to 4% (Source: Consumer Council, May 2013) ...

Loans Classified by Special Provision

... The first such program, FHA-245, came into being in 1978. The FHA-245 program is especially attractive to those just starting their careers and anticipating increases in their incomes. They are able to obtain a home with an initial lower monthly installment obligation than would be available under a ...

... The first such program, FHA-245, came into being in 1978. The FHA-245 program is especially attractive to those just starting their careers and anticipating increases in their incomes. They are able to obtain a home with an initial lower monthly installment obligation than would be available under a ...

Credit Rationing by Loan Size in Commercial Loan Markets

... has the following properties. It indicates that the loan size, qi, offered to borrowers of type i = 1,...,n -,l is strictly less than the size available in a perfectly competitive market for all groups except the largest. To see why, observe that equation (4) indicates that the profit-maximizing loa ...

... has the following properties. It indicates that the loan size, qi, offered to borrowers of type i = 1,...,n -,l is strictly less than the size available in a perfectly competitive market for all groups except the largest. To see why, observe that equation (4) indicates that the profit-maximizing loa ...

Evaluating Consumer Loans

... Credit cards and overlines tied to checking accounts are the two most popular forms of revolving credit agreements ...

... Credit cards and overlines tied to checking accounts are the two most popular forms of revolving credit agreements ...

Evaluating Consumer Loans

... Credit cards and overlines tied to checking accounts are the two most popular forms of revolving credit agreements ...

... Credit cards and overlines tied to checking accounts are the two most popular forms of revolving credit agreements ...

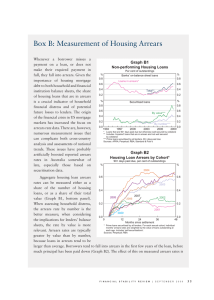

Box B: Measurement of Housing Arrears Graph B1

... from ADIs, and it is also used for securitised loans by some non-ADIs. In contrast, a ‘missed payments’ approach is used for other securitised loans, where a lender simply counts the number of missed payments, even if the borrower had previously made extra repayments. This is a stricter approach tha ...

... from ADIs, and it is also used for securitised loans by some non-ADIs. In contrast, a ‘missed payments’ approach is used for other securitised loans, where a lender simply counts the number of missed payments, even if the borrower had previously made extra repayments. This is a stricter approach tha ...

Five Ways to Ramp Up Fee Income

... Typically, wealth management is handled, if at all, by a subsidiary of the bank holding company. For example, CoBiz Financial, Inc., of Denver offers high end estate planning, wealth transfer and wealth management under its Financial Designs Ltd. subsidiary. Because of the complexity of high end cli ...

... Typically, wealth management is handled, if at all, by a subsidiary of the bank holding company. For example, CoBiz Financial, Inc., of Denver offers high end estate planning, wealth transfer and wealth management under its Financial Designs Ltd. subsidiary. Because of the complexity of high end cli ...

Payday loan

A payday loan (also called a payday advance, salary loan, payroll loan, small dollar loan, short term, or cash advance loan) is a small, short-term unsecured loan, ""regardless of whether repayment of loans is linked to a borrower's payday."" The loans are also sometimes referred to as ""cash advances,"" though that term can also refer to cash provided against a prearranged line of credit such as a credit card. Payday advance loans rely on the consumer having previous payroll and employment records. Legislation regarding payday loans varies widely between different countries and, within the USA, between different states.To prevent usury (unreasonable and excessive rates of interest), some jurisdictions limit the annual percentage rate (APR) that any lender, including payday lenders, can charge. Some jurisdictions outlaw payday lending entirely, and some have very few restrictions on payday lenders. In the United States, the rates of these loans were formerly restricted in most states by the Uniform Small Loan Laws (USLL), with 36%-40% APR generally the norm.There are many different ways to calculate annual percentage rate of a loan. Depending on which method is used, the rate calculated may differ dramatically. E.g., for a $15 charge on a $100 14-day payday loan, it could be (from the borrower's perspective) anywhere from 391% to 3733%.Although some have noted that these loans appear to carry substantial risk to the lender, it has recently been shown that these loans carry no more long term risk for the lender than other forms of credit. These studies seem to be confirmed by the SEC 10-K filings of at least one lender, who notes a charge-off rate of 3.2%.