Charities Accounting Standard (CAS)

... governing board members‟ duty of public accountability and stewardship. The CAS sets out the accounting standards for this purpose but governing board members shall consider providing any additional information that is needed to give donors, beneficiaries and the general public a greater insight int ...

... governing board members‟ duty of public accountability and stewardship. The CAS sets out the accounting standards for this purpose but governing board members shall consider providing any additional information that is needed to give donors, beneficiaries and the general public a greater insight int ...

Wahlen 1e_PPT_Ch 21_IE

... Were the company’s operations a source or a use of cash? What investments and growth activities took place? How were they financed? What were the proceeds received from issuing capital stock or debt and how were the funds used? ...

... Were the company’s operations a source or a use of cash? What investments and growth activities took place? How were they financed? What were the proceeds received from issuing capital stock or debt and how were the funds used? ...

FREE Sample Here - We can offer most test bank and

... 29. Companies prepare classified and comparative financial statements because a. They are required by international accounting principles b. They provide financial statement readers with useful information about trends in financial position and operating performance c. They are required by the IRS d ...

... 29. Companies prepare classified and comparative financial statements because a. They are required by international accounting principles b. They provide financial statement readers with useful information about trends in financial position and operating performance c. They are required by the IRS d ...

Does the Big-4 Effect Exist when Reputation and

... concerns over omitted correlated variables. Third, this study provides new evidence on audit quality in the private-client segment of the economy. The private segment is pertinent because of its economic significance for the overall economy and in particular for the audit industry (i.e., many privat ...

... concerns over omitted correlated variables. Third, this study provides new evidence on audit quality in the private-client segment of the economy. The private segment is pertinent because of its economic significance for the overall economy and in particular for the audit industry (i.e., many privat ...

File

... Determine cash received from customers (direct method). Determine taxes paid (direct method). Determine net cash flow from financing activities. Compute net cash used in financing activities. Sale of fixed assets at a gain/cash flow effects. Analysis of plant asset account/cash flow presentation. Sa ...

... Determine cash received from customers (direct method). Determine taxes paid (direct method). Determine net cash flow from financing activities. Compute net cash used in financing activities. Sale of fixed assets at a gain/cash flow effects. Analysis of plant asset account/cash flow presentation. Sa ...

Full file at http://TestbankCollege.eu/Test-Bank-Financial

... 33) How does an account receivable differ from a note receivable? A) A note receivable is an asset while an account receivable is not. B) An account receivable is a written pledge while a note receivable is not. C) An account receivable is always an amount due from the company's customers while a no ...

... 33) How does an account receivable differ from a note receivable? A) A note receivable is an asset while an account receivable is not. B) An account receivable is a written pledge while a note receivable is not. C) An account receivable is always an amount due from the company's customers while a no ...

chapter 8 - Csulb.edu

... back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net income pattern by matching current cost of goods sold with current revenue, when inventories remain at constant quantities. c. When a firm using the LIFO method fails to maintain its usual in ...

... back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net income pattern by matching current cost of goods sold with current revenue, when inventories remain at constant quantities. c. When a firm using the LIFO method fails to maintain its usual in ...

CP8–3.

... depreciation on the asset. 14. An intangible asset is acquired and held by the business for use in operations and not for sale. Intangible assets are acquired because of the special rights they confer on ownership. They have no physical substance but represent valuable rights that will be used up in ...

... depreciation on the asset. 14. An intangible asset is acquired and held by the business for use in operations and not for sale. Intangible assets are acquired because of the special rights they confer on ownership. They have no physical substance but represent valuable rights that will be used up in ...

Revenue Recognition - Financial Reporting Council

... accounting standard governing the recognition and measurement of revenue. Different entities and industries follow practices that are in some respects inconsistent with one another; more generally, there are different views of what revenue is or represents, and of how financial statements should por ...

... accounting standard governing the recognition and measurement of revenue. Different entities and industries follow practices that are in some respects inconsistent with one another; more generally, there are different views of what revenue is or represents, and of how financial statements should por ...

Staff Guidance for Auditors of SEC-Registered Brokers and

... amendments, which are applicable when the auditor reports on the supporting schedules of a broker or dealer. 5 These standards and related amendments were approved by the SEC on February 12, 2014, and are effective for fiscal years ending on or after June 1, 2014, which coincides with the effective ...

... amendments, which are applicable when the auditor reports on the supporting schedules of a broker or dealer. 5 These standards and related amendments were approved by the SEC on February 12, 2014, and are effective for fiscal years ending on or after June 1, 2014, which coincides with the effective ...

User guide to Standing Direction 1

... The FMCF was launched by the Department of Treasury and Finance (DTF) in July 2003 and was subsequently updated in July 2005 and August 2007. The Directions are designed to supplement the Financial Management Act 1994 (FMA). ...

... The FMCF was launched by the Department of Treasury and Finance (DTF) in July 2003 and was subsequently updated in July 2005 and August 2007. The Directions are designed to supplement the Financial Management Act 1994 (FMA). ...

FAP Chapter 19 SM - Test Bank wizard

... 10. This production run should be accounted for as a job lot (batch). Although individual iPhones could be viewed as individual jobs, the costs of tracking this detailed information would outweigh the benefits. Determining the cost of the batch should provide management and employees with sufficient ...

... 10. This production run should be accounted for as a job lot (batch). Although individual iPhones could be viewed as individual jobs, the costs of tracking this detailed information would outweigh the benefits. Determining the cost of the batch should provide management and employees with sufficient ...

Annual Report 2011-2012 - Financial Intelligence Centre

... money laundering and the financing of terrorism and the proliferation of weapons of mass destruction. It has 36 members – including South Africa, which is the only African representative – and its Recommendations have been adopted by more than 180 countries. In February 2012, the FATF adopted a revi ...

... money laundering and the financing of terrorism and the proliferation of weapons of mass destruction. It has 36 members – including South Africa, which is the only African representative – and its Recommendations have been adopted by more than 180 countries. In February 2012, the FATF adopted a revi ...

Revised Guidance Statement GS 009: Auditing SMSFs

... approved SMSF auditor (the auditor),4 who is required to complete both the financial audit and the compliance engagement and sign the auditor’s report before a SMSF may submit its Annual Return.5 The auditor reports to the trustees6 in the “approved form”, as issued and updated from time to time, by ...

... approved SMSF auditor (the auditor),4 who is required to complete both the financial audit and the compliance engagement and sign the auditor’s report before a SMSF may submit its Annual Return.5 The auditor reports to the trustees6 in the “approved form”, as issued and updated from time to time, by ...

RICC 1256 Rev 6

... development by the European Agricultural Fund for Rural Development (EAFRD). Council Regulation (EC) No 1083/2006 of 11 July 2006 (OJ L 210, 31.7.2006, p. 25) laying down general provisions on the European Regional Development Fund, the European Social Fund and the Cohesion Fund and ...

... development by the European Agricultural Fund for Rural Development (EAFRD). Council Regulation (EC) No 1083/2006 of 11 July 2006 (OJ L 210, 31.7.2006, p. 25) laying down general provisions on the European Regional Development Fund, the European Social Fund and the Cohesion Fund and ...

Internal Control and Cash

... measure contributes to the safeguarding of cash in two ways: First, the insurance company carefully screens all individuals before adding them to the policy and may reject risky applicants. Second, bonded employees know that the insurance company will vigorously prosecute all offenders. 2. Rotating ...

... measure contributes to the safeguarding of cash in two ways: First, the insurance company carefully screens all individuals before adding them to the policy and may reject risky applicants. Second, bonded employees know that the insurance company will vigorously prosecute all offenders. 2. Rotating ...

Fraud, Internal Control, and Cash 7

... “We have an electronic cash register, but it’s not the fancy new kind where you just punch in the item,” explains Ms. Mintenko. “You have to punch in the prices.” The machine does keep track of sales in several categories, however. Cashiers punch a button to indicate whether each item is a beverage, ...

... “We have an electronic cash register, but it’s not the fancy new kind where you just punch in the item,” explains Ms. Mintenko. “You have to punch in the prices.” The machine does keep track of sales in several categories, however. Cashiers punch a button to indicate whether each item is a beverage, ...

Detecting asset misappropriation: a framework for

... payment by submitting invoices for fictitious goods or services or goods with inferior quality, inflated invoices, or invoices for personal purchases (Wells, 2005; Buckhoff, 2006; Silverstone and Sheetz, 2007; ACFE, 2010). Results from the 2010 ACFE’s Report to the Nation on Occupational Fraud and A ...

... payment by submitting invoices for fictitious goods or services or goods with inferior quality, inflated invoices, or invoices for personal purchases (Wells, 2005; Buckhoff, 2006; Silverstone and Sheetz, 2007; ACFE, 2010). Results from the 2010 ACFE’s Report to the Nation on Occupational Fraud and A ...

RITCHIE BROS AUCTIONEERS INC (Form: 40-F

... Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this an ...

... Based on my knowledge, this annual report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this an ...

Business and Economics - Pearson Education Asia

... This new updated edition now incorporates the content offered in the supplementary 80 page booklet which was previously provided packaged with the text and will be available for courses commencing semester 2, 2011. This includes a fully revised Chapter 2, Audit Reports. Auditing, Assurance Services ...

... This new updated edition now incorporates the content offered in the supplementary 80 page booklet which was previously provided packaged with the text and will be available for courses commencing semester 2, 2011. This includes a fully revised Chapter 2, Audit Reports. Auditing, Assurance Services ...

download

... Example Exercise 6-1 On August 25, Gallatin Repair Service extended an offer of During year, soldatfor $125,000the forcurrent land that had merchandise been priced forissale $150,000. On Rp250,000,000 cash Repair and forService Rp975,000,000 onseller’s account. September 3, Gallatin accepted the The ...

... Example Exercise 6-1 On August 25, Gallatin Repair Service extended an offer of During year, soldatfor $125,000the forcurrent land that had merchandise been priced forissale $150,000. On Rp250,000,000 cash Repair and forService Rp975,000,000 onseller’s account. September 3, Gallatin accepted the The ...

Statement of Accounts 2014/2015

... liabilities recognised by the County Council. The net assets of the County Council (assets less liabilities) are matched by the reserves held. Reserves are reported in two categories. The first category of reserves are usable reserves, i.e. those reserves that the County Council may use to provide s ...

... liabilities recognised by the County Council. The net assets of the County Council (assets less liabilities) are matched by the reserves held. Reserves are reported in two categories. The first category of reserves are usable reserves, i.e. those reserves that the County Council may use to provide s ...

Defence Audit Guidelines_Final 25 March 2010

... practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approaches to audit that can be applied by auditors for conducting the audit of government entities in Pakistan. FAM has been implemented in the Department of the Auditor-General of Pakistan (DAG). Howev ...

... practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approaches to audit that can be applied by auditors for conducting the audit of government entities in Pakistan. FAM has been implemented in the Department of the Auditor-General of Pakistan (DAG). Howev ...

Accounts Receivable - University of New Orleans

... Delinquent accounts that are between 60 and 90 days past due are forwarded to the collections agency. Our current collections agency is National Recovery Agency. Once it is identified a student is defaulted and no longer a current student, a Pre-Collection (payment reminder) email is sent. Thi ...

... Delinquent accounts that are between 60 and 90 days past due are forwarded to the collections agency. Our current collections agency is National Recovery Agency. Once it is identified a student is defaulted and no longer a current student, a Pre-Collection (payment reminder) email is sent. Thi ...

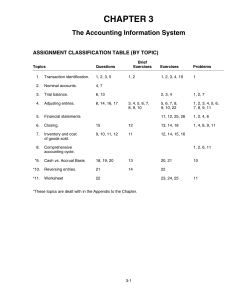

CHAPTER 3

... this account are: (1) Purchases, (2) Purchase Discounts, (3) Purchase Returns, (4) Purchase Allowances, (5) Transportation-in, (6) Inventory (beginning), and (7) Inventory (ending). The ending balance represents the cost of goods sold. 11. The purpose of the Cost of Goods Sold account is to accumula ...

... this account are: (1) Purchases, (2) Purchase Discounts, (3) Purchase Returns, (4) Purchase Allowances, (5) Transportation-in, (6) Inventory (beginning), and (7) Inventory (ending). The ending balance represents the cost of goods sold. 11. The purpose of the Cost of Goods Sold account is to accumula ...

History of accounting

The history of accounting or accountancy is thousands of years old and can be traced to ancient civilisations.The early development of accounting dates back to ancient Mesopotamia, and is closely related to developments in writing, counting and money and early auditing systems by the ancient Egyptians and Babylonians. By the time of the Emperor Augustus, the Roman government had access to detailed financial information.Some Hindus believe that the Indian Chanakya created a work similar to a financial management book, during the period of the Maurya Empire. His book ""Arthashasthra"" contains few detailed aspects of maintaining books of accounts for a Sovereign State. The Italian Luca Pacioli, recognized as The Father of accounting and bookeeping was the first person to publish a work on double-entry bookkeeping, which then developed in medieval Europe. Accounting began to transition into an organized profession in the nineteenth century, with local professional bodies in England merging to form the Institute of Chartered Accountants in England and Wales in 1880.