AT1- 1 Achievement Test 1 Achievement Test 1: Chapters 1 and 2

... Instructions: Designate the best answer for each of the following questions. ____ 1. "GAAP" refers to a. General Accounting and Auditing Principles. b. Guidelines for American Accounting Procedures. c. General Association of Accounting Practitioners. d. None of the above. ____ 2. The requirement tha ...

... Instructions: Designate the best answer for each of the following questions. ____ 1. "GAAP" refers to a. General Accounting and Auditing Principles. b. Guidelines for American Accounting Procedures. c. General Association of Accounting Practitioners. d. None of the above. ____ 2. The requirement tha ...

Diapositiva 1 - impact iTech

... •Integrated with External Rate Systems •The same document structure as Money Markets •Integrated to E-Banking ...

... •Integrated with External Rate Systems •The same document structure as Money Markets •Integrated to E-Banking ...

ACCOUNTING is primarily a system of

... accounts of the accounting journal as either debits or credits. Journal entries are usually backed up with a piece of paper; a receipt, a bill, an invoice, or some other direct record of the transaction; making them easy to record and to maintain traceability for each transaction. 56. LIABILITY, is ...

... accounts of the accounting journal as either debits or credits. Journal entries are usually backed up with a piece of paper; a receipt, a bill, an invoice, or some other direct record of the transaction; making them easy to record and to maintain traceability for each transaction. 56. LIABILITY, is ...

ADVANCED ACCOUNTING (02)

... 8. The objective of a petty cash systems is to _______. A. facilitate office payment of small, miscellaneous items B. cash checks for employees C. account for cash sales D. account for all cash receipts and disbursement 9. Barry Brothers’ Sales were $375,850, Sales Discounts were $12,000 and Sales R ...

... 8. The objective of a petty cash systems is to _______. A. facilitate office payment of small, miscellaneous items B. cash checks for employees C. account for cash sales D. account for all cash receipts and disbursement 9. Barry Brothers’ Sales were $375,850, Sales Discounts were $12,000 and Sales R ...

Accounting 1 Syllabus

... Students will not enter chat rooms. Some sites are very large and may not need to be printed. Students will not print except by teacher permission only. Students must also return the district agreement for network usage signed by themselves and their parents. It is imperative that students maintain ...

... Students will not enter chat rooms. Some sites are very large and may not need to be printed. Students will not print except by teacher permission only. Students must also return the district agreement for network usage signed by themselves and their parents. It is imperative that students maintain ...

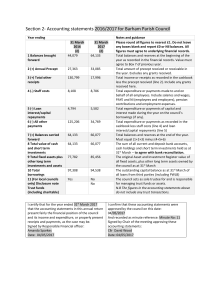

section 2 Accounts - Barham Parish Council

... cash holdings and short term investments held as at 31st March – to agree with bank reconciliation. The original Asset and Investment Register value of all fixed assets, plus other long term assets owned by the council as at 31st March The outstanding capital balance as at 31st March of all loans fr ...

... cash holdings and short term investments held as at 31st March – to agree with bank reconciliation. The original Asset and Investment Register value of all fixed assets, plus other long term assets owned by the council as at 31st March The outstanding capital balance as at 31st March of all loans fr ...

Course Outline - Jackson College

... To analyze and interpret cost accounting reports, i.e. cost of production and variance analysis reports. To prepare cost accounting reports, i.e. cost of production and variance analysis reports in both job order and process systems. 5. To apply the principles of cost accounting and cost behavior to ...

... To analyze and interpret cost accounting reports, i.e. cost of production and variance analysis reports. To prepare cost accounting reports, i.e. cost of production and variance analysis reports in both job order and process systems. 5. To apply the principles of cost accounting and cost behavior to ...

ACCT 108 Title: College Accounting Division

... and should not be penalized for the absence. Proper procedure should be followed in notifying faculty in advance of the student’s planned participation in the event. Ultimately it is the student’s responsibility to notify the instructor in advance of the planned absence. Unless students are particip ...

... and should not be penalized for the absence. Proper procedure should be followed in notifying faculty in advance of the student’s planned participation in the event. Ultimately it is the student’s responsibility to notify the instructor in advance of the planned absence. Unless students are particip ...

Document

... practices that companies use for financial accounting and reporting in the United States. These principles, or “rules” must be followed in the external reports of companies that sell stock to the public in the United States and by many other companies as well. ...

... practices that companies use for financial accounting and reporting in the United States. These principles, or “rules” must be followed in the external reports of companies that sell stock to the public in the United States and by many other companies as well. ...

Statement of Owners` Equity

... accounting standards and interpretations and, in 2001, became the International Accounting Standards Board (IASB). International Financial Reporting Standards (IFRS) are the standards and interpretations adopted by the IASB. Exchange rates- ratio at which a country’s currency can be ...

... accounting standards and interpretations and, in 2001, became the International Accounting Standards Board (IASB). International Financial Reporting Standards (IFRS) are the standards and interpretations adopted by the IASB. Exchange rates- ratio at which a country’s currency can be ...

Ch3

... On the expense side of the accounting equation there are two components. First are the traditional cost reduction methods of corporate downsizing, restructuring, re-engineering, and other cost containment strategies designed to reduce both fixed and variable operational overhead. Fixed costs are cos ...

... On the expense side of the accounting equation there are two components. First are the traditional cost reduction methods of corporate downsizing, restructuring, re-engineering, and other cost containment strategies designed to reduce both fixed and variable operational overhead. Fixed costs are cos ...

Will Big Four Audit Firms Survive in a World of Unlimited Liability

... vanished in a sea of liability that it was only a matter of time before another firm followed. And then, the thought goes, the others would find it impossible to persuade partners to stay, lest their net worth be decimated as happened at Andersen. Perhaps the situation is not unlike the one that con ...

... vanished in a sea of liability that it was only a matter of time before another firm followed. And then, the thought goes, the others would find it impossible to persuade partners to stay, lest their net worth be decimated as happened at Andersen. Perhaps the situation is not unlike the one that con ...

Developing a Cost Accounting System for First Government Contract

... A multi-billion dollar Middle-Eastern logistics support and chain supply company received their first U.S. government contract with the U.S. Army to provide field supplies to military forces in Kuwait and Afghanistan under a cost reimbursable contract. Reimbursable contracts require an acceptable co ...

... A multi-billion dollar Middle-Eastern logistics support and chain supply company received their first U.S. government contract with the U.S. Army to provide field supplies to military forces in Kuwait and Afghanistan under a cost reimbursable contract. Reimbursable contracts require an acceptable co ...

ch_1_intro_to_accoun..

... Each transaction must identify the specific items affected and the net change on each item Each transaction has a dual effect on the accounting equation The two sides of the accounting equation must ...

... Each transaction must identify the specific items affected and the net change on each item Each transaction has a dual effect on the accounting equation The two sides of the accounting equation must ...

Prior Year Adjustment (PYA)/Extraordinary Revenue

... (b) They must be specifically identifiable with and directly related to the business activities of prior years; (c) They are not attributable to economic events occurring subsequent to the date of the financial statements for such prior years; and (d) They could not be reasonably estimated prior to ...

... (b) They must be specifically identifiable with and directly related to the business activities of prior years; (c) They are not attributable to economic events occurring subsequent to the date of the financial statements for such prior years; and (d) They could not be reasonably estimated prior to ...

Financial Recordkeeping, pp 428-436

... Accounting Systems Businesses keep score GAAP: Generally Accepted Accounting Principles The Accounting Equation: Assets = Liabilities + Owner’s Equity Assets are anything of value (ie cash, equipment, accounts receivable) Liabilities are anything the business owes Owner’s Equity is the net worth of ...

... Accounting Systems Businesses keep score GAAP: Generally Accepted Accounting Principles The Accounting Equation: Assets = Liabilities + Owner’s Equity Assets are anything of value (ie cash, equipment, accounts receivable) Liabilities are anything the business owes Owner’s Equity is the net worth of ...

1. Accountants refer to an economic event as a a. purchase. b. sale

... The matching principle states that expenses should be matched with revenues. Another way of stating the principle is to say that a. assets should be matched with liabilities. b. efforts should be matched with accomplishments. c. dividends to stockholders should be matched with stockholders' investme ...

... The matching principle states that expenses should be matched with revenues. Another way of stating the principle is to say that a. assets should be matched with liabilities. b. efforts should be matched with accomplishments. c. dividends to stockholders should be matched with stockholders' investme ...

會計學原理Principles of Accounts

... • If you are the business owner • You should : – Know the company’s Profit or Loss; Assets (資產) and Liabilities (負債) – Make business decisions with the financial information of the company – Investigate business fraud if any ...

... • If you are the business owner • You should : – Know the company’s Profit or Loss; Assets (資產) and Liabilities (負債) – Make business decisions with the financial information of the company – Investigate business fraud if any ...

Ch. 15 – Vocabulary Review accounting generally accepted

... operating expenses, cash receipts, and outlays for a future time period. ...

... operating expenses, cash receipts, and outlays for a future time period. ...

Don Insley, CPA

... Don Insley, CPA Donald F. Insley, Jr., P.A. Certified Public Accountant After graduating from Salisbury University’s Perdue School of Business with a Bachelor’s Degree in Accounting in 1987, I began working for a regional CPA firm based in Baltimore. During this time period, I worked very hard to ob ...

... Don Insley, CPA Donald F. Insley, Jr., P.A. Certified Public Accountant After graduating from Salisbury University’s Perdue School of Business with a Bachelor’s Degree in Accounting in 1987, I began working for a regional CPA firm based in Baltimore. During this time period, I worked very hard to ob ...

Ethical and Educational Perspectives of Accounting Practices: Experience with Two Canadian Service Organizations:

... their moral beliefs. However, accountants with extensive practical experience feel that their moral beliefs should not rise above their professional duty (as accountant) because they have been experienced with confronting more dilemmas. This study also found that accountants with legal background ba ...

... their moral beliefs. However, accountants with extensive practical experience feel that their moral beliefs should not rise above their professional duty (as accountant) because they have been experienced with confronting more dilemmas. This study also found that accountants with legal background ba ...

History of accounting

The history of accounting or accountancy is thousands of years old and can be traced to ancient civilisations.The early development of accounting dates back to ancient Mesopotamia, and is closely related to developments in writing, counting and money and early auditing systems by the ancient Egyptians and Babylonians. By the time of the Emperor Augustus, the Roman government had access to detailed financial information.Some Hindus believe that the Indian Chanakya created a work similar to a financial management book, during the period of the Maurya Empire. His book ""Arthashasthra"" contains few detailed aspects of maintaining books of accounts for a Sovereign State. The Italian Luca Pacioli, recognized as The Father of accounting and bookeeping was the first person to publish a work on double-entry bookkeeping, which then developed in medieval Europe. Accounting began to transition into an organized profession in the nineteenth century, with local professional bodies in England merging to form the Institute of Chartered Accountants in England and Wales in 1880.