Does a Change in a Logo Affect the Value of the Brand? The Case

... that Starbucks was placing larger orders for a particular drip coffeemaker than retail giant Macy’s. When he first entered Starbucks the powerful and pleasant aromas of the coffee beans and the wall displaying the coffee took his breath away.10 And after his first cup of full-flavored, dark-roasted ...

... that Starbucks was placing larger orders for a particular drip coffeemaker than retail giant Macy’s. When he first entered Starbucks the powerful and pleasant aromas of the coffee beans and the wall displaying the coffee took his breath away.10 And after his first cup of full-flavored, dark-roasted ...

chapter 6

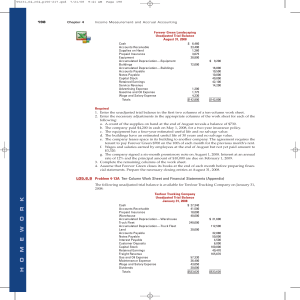

... 2. Explain the accounting for inventories, and apply the inventory cost flow methods. The primary basis of accounting for inventories is cost. Cost includes all expenditures necessary to acquire goods and place them in condition ready for sale. Cost of goods available for sale includes (a) cost of b ...

... 2. Explain the accounting for inventories, and apply the inventory cost flow methods. The primary basis of accounting for inventories is cost. Cost includes all expenditures necessary to acquire goods and place them in condition ready for sale. Cost of goods available for sale includes (a) cost of b ...

PTA Money Matters Quick-Reference Guide

... Your role as PTA treasurer carries a good deal of responsibility, but it is also a wonderful position to have. You are about to embark upon an enriching, challenging, and fulfilling opportunity to help carry out PTA’s Mission for your community’s school and children. National PTA has created this qu ...

... Your role as PTA treasurer carries a good deal of responsibility, but it is also a wonderful position to have. You are about to embark upon an enriching, challenging, and fulfilling opportunity to help carry out PTA’s Mission for your community’s school and children. National PTA has created this qu ...

Accounting for TourismThe Tourism Satellite Account (TSA)

... Nederlandstalige samenvatting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245 References. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253 ...

... Nederlandstalige samenvatting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245 References. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253 ...

Chapter Accounting for Leases - McGraw Hill Higher Education

... reality and not merely with legal form. Although the legal form of a lease agreement is that the lessee may acquire no legal title to the leased asset, in the case of finance leases the substance and financial reality are that the lessee acquires the economic benefits of the use of the leased asset ...

... reality and not merely with legal form. Although the legal form of a lease agreement is that the lessee may acquire no legal title to the leased asset, in the case of finance leases the substance and financial reality are that the lessee acquires the economic benefits of the use of the leased asset ...

Budgeting and Budgetary Institutions

... In Western democracies, systems of checks and balances built into government structures have formed the core of good governance and have helped empower citizens for more than two hundred years. The incentives that motivate public servants and policy makers— the rewards and sanctions linked to result ...

... In Western democracies, systems of checks and balances built into government structures have formed the core of good governance and have helped empower citizens for more than two hundred years. The incentives that motivate public servants and policy makers— the rewards and sanctions linked to result ...

Financial Accounting Chapter 2

... AICPA Functional Competencies: Measurement AICPA Business Perspective Competencies: Strategic/Critical Thinking 2.1-25 A company paid cash for an amount owed to a creditor. This transaction decreased cash and: A) decreased revenues. B) decreased liabilities. C) decreased expenses. D) increased expen ...

... AICPA Functional Competencies: Measurement AICPA Business Perspective Competencies: Strategic/Critical Thinking 2.1-25 A company paid cash for an amount owed to a creditor. This transaction decreased cash and: A) decreased revenues. B) decreased liabilities. C) decreased expenses. D) increased expen ...

66862 c07 296-365

... To this point, we have concentrated on the accounting for businesses that sell services. Banks, hotels, airlines, health clubs, real estate offices, law firms, and accounting firms are all examples of service companies. In this chapter we turn to accounting by companies that sell products, or what a ...

... To this point, we have concentrated on the accounting for businesses that sell services. Banks, hotels, airlines, health clubs, real estate offices, law firms, and accounting firms are all examples of service companies. In this chapter we turn to accounting by companies that sell products, or what a ...

PJM Manual 28:

... Section 8: Transmission Congestion Accounting Overview................57 8.1 Transmission Congestion Accounting Overview......................................................... 57 8.2 Transmission Congestion Charges............................................................................. 58 8.2 ...

... Section 8: Transmission Congestion Accounting Overview................57 8.1 Transmission Congestion Accounting Overview......................................................... 57 8.2 Transmission Congestion Charges............................................................................. 58 8.2 ...

Earnings Quality and Stock Returns

... aggressive in applying accounting rules so as not to disappoint investors and analysts. The Securities and Exchange Commission (SEC) (2003) cites hundreds of cases in which managers have used accounting maneuvers to puff up their firms’ profits. Examples of high-profile firms that have inflated earn ...

... aggressive in applying accounting rules so as not to disappoint investors and analysts. The Securities and Exchange Commission (SEC) (2003) cites hundreds of cases in which managers have used accounting maneuvers to puff up their firms’ profits. Examples of high-profile firms that have inflated earn ...

HOMEWORK

... statements, the cost that a retailer pays for the merchandise that it sells is the most important factor in determining whether the company is profitable. For Gap Inc., “Cost of goods sold and occupancy expenses” amounted to approximately $10 billion in each year. One of the biggest challenges a ret ...

... statements, the cost that a retailer pays for the merchandise that it sells is the most important factor in determining whether the company is profitable. For Gap Inc., “Cost of goods sold and occupancy expenses” amounted to approximately $10 billion in each year. One of the biggest challenges a ret ...

FREE Sample Here

... c. the assets purchased with cash contributed by the owner and the cash spent to operate the business d. the amounts received from customers for goods or services and the amounts paid forthe inputs used to provide the goods or services ANSWER: DIFFICULTY: ...

... c. the assets purchased with cash contributed by the owner and the cash spent to operate the business d. the amounts received from customers for goods or services and the amounts paid forthe inputs used to provide the goods or services ANSWER: DIFFICULTY: ...

Chapter 1 - Test Bank

... The AICPA's Code of Professional Conduct for Accountants provides guidance to CPAs in the performance of their work. Answer: True LO: 1-3 Diff: 1 EOC Ref: E1-15 AACSB: Reflective Thinking AICPA Business Perspective Competencies: Legal, Regulatory AICPA Functional Competencies: Reporting, Decision Mo ...

... The AICPA's Code of Professional Conduct for Accountants provides guidance to CPAs in the performance of their work. Answer: True LO: 1-3 Diff: 1 EOC Ref: E1-15 AACSB: Reflective Thinking AICPA Business Perspective Competencies: Legal, Regulatory AICPA Functional Competencies: Reporting, Decision Mo ...

Chapter 2—Financial Statements and the Annual Report

... a. To reflect prospective cash receipts to investors and creditors. b. To reflect prospective cash flows to an enterprise. c. To reflect resources and claims to resources. d. To reflect current stock prices and information concerning stock markets. ANS: D OBJ: 1 ...

... a. To reflect prospective cash receipts to investors and creditors. b. To reflect prospective cash flows to an enterprise. c. To reflect resources and claims to resources. d. To reflect current stock prices and information concerning stock markets. ANS: D OBJ: 1 ...

ASRE 2410 Review of a Financial Report Performed by the Independent Auditor of the Entity. The choice of ASRE 2400

... statement by those responsible for the financial report. The related notes ordinarily comprise a summary of significant accounting policies and other explanatory information. The requirements of the applicable financial reporting framework determine the form and content of the financial report. For ...

... statement by those responsible for the financial report. The related notes ordinarily comprise a summary of significant accounting policies and other explanatory information. The requirements of the applicable financial reporting framework determine the form and content of the financial report. For ...

FREE Sample Here

... 32. Costs incurred in operating a business are also known as a. revenues. b. expenses. c. liabilities. d. dividends. ANS: B PTS: 0 DIF: Easy NAT: AACSB Reflective Thinking | AICPA FN-Measurement ...

... 32. Costs incurred in operating a business are also known as a. revenues. b. expenses. c. liabilities. d. dividends. ANS: B PTS: 0 DIF: Easy NAT: AACSB Reflective Thinking | AICPA FN-Measurement ...

AH Belo Corporation - corporate

... in Net Income, (i) any cash payments made during such period in respect of non-cash charges described in clause (a)(v) taken in a prior period and (ii) any extraordinary gains and any non-cash items of income for such period, all calculated for the Company and its Subsidiaries on a consolidated basi ...

... in Net Income, (i) any cash payments made during such period in respect of non-cash charges described in clause (a)(v) taken in a prior period and (ii) any extraordinary gains and any non-cash items of income for such period, all calculated for the Company and its Subsidiaries on a consolidated basi ...

Notes - cloudfront.net

... eliminations of duplicate staff and expenses, rationalization of exploration spending and capital expenditures, operating savings, interest and taxes, all of which are estimated to be approximately $70 million after tax during the first full year of combined operations. ...

... eliminations of duplicate staff and expenses, rationalization of exploration spending and capital expenditures, operating savings, interest and taxes, all of which are estimated to be approximately $70 million after tax during the first full year of combined operations. ...

CPA PassMaster Questions–Auditing 4 Export Date: 10/30/08

... from the custodial function allows an individual to misappropriate cash and then cover up the theft by posting credits against the related A/R balance. Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same ...

... from the custodial function allows an individual to misappropriate cash and then cover up the theft by posting credits against the related A/R balance. Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same ...

Form DEF 14A Cryoport, Inc. - CYRX Filed: September 02, 2016

... Notwithstanding the foregoing, if any proposal is contested, the rules of the New York Stock Exchange governing brokers’ discretionary authority (which apply to brokers’ authority with respect to companies listed on NASDAQ) do not permit brokers to exercise discretionary authority regarding any of t ...

... Notwithstanding the foregoing, if any proposal is contested, the rules of the New York Stock Exchange governing brokers’ discretionary authority (which apply to brokers’ authority with respect to companies listed on NASDAQ) do not permit brokers to exercise discretionary authority regarding any of t ...

Cost Accounting

... ix. To help in the preparation of budgets and implementation of budgetary control. x. To guide management in the formulation and implementation of incentive bonus plans based on productivity and cost savings. xi. To supply useful data to the management to take various financial decisions such as int ...

... ix. To help in the preparation of budgets and implementation of budgetary control. x. To guide management in the formulation and implementation of incentive bonus plans based on productivity and cost savings. xi. To supply useful data to the management to take various financial decisions such as int ...

IBAC Annual Report 2014/15 - Independent broad

... with procurement practices in state government, alleged serious corruption and theft by a local council worker with criminal connections, and alleged assault by police on a vulnerable person in custody. One of our major investigations, Operation Fitzroy, focused on serious systemic corruption within ...

... with procurement practices in state government, alleged serious corruption and theft by a local council worker with criminal connections, and alleged assault by police on a vulnerable person in custody. One of our major investigations, Operation Fitzroy, focused on serious systemic corruption within ...

Cash Operations Manual *UPDATED*

... University, hereafter referred to as the University, into one centralized, easy to use reference manual. The collection and control of cash (see definition in Section IV) at Savannah State University are very important functions. Ideally, from an internal control perspective, the collection and cont ...

... University, hereafter referred to as the University, into one centralized, easy to use reference manual. The collection and control of cash (see definition in Section IV) at Savannah State University are very important functions. Ideally, from an internal control perspective, the collection and cont ...

Experimental Biodiversity Accounting as a component of the

... characteristics (e.g. soil type, altitude) with the economy and other human activities. It also allows comparison and integration of data on ecosystem services with other economic and social data. Biodiversity Accounts, one of a number of accounts in the SEEA-EEA framework, can help understand the r ...

... characteristics (e.g. soil type, altitude) with the economy and other human activities. It also allows comparison and integration of data on ecosystem services with other economic and social data. Biodiversity Accounts, one of a number of accounts in the SEEA-EEA framework, can help understand the r ...

Lesson : 1

... completed this project, the profits arising thereof will be shared by them in proportion to their contribution. Whey they are undertaking this project, they are free to carry on their own business as usual unless otherwise agreed. As the project ends, the relationship between the parties i.e. co-ven ...

... completed this project, the profits arising thereof will be shared by them in proportion to their contribution. Whey they are undertaking this project, they are free to carry on their own business as usual unless otherwise agreed. As the project ends, the relationship between the parties i.e. co-ven ...

History of accounting

The history of accounting or accountancy is thousands of years old and can be traced to ancient civilisations.The early development of accounting dates back to ancient Mesopotamia, and is closely related to developments in writing, counting and money and early auditing systems by the ancient Egyptians and Babylonians. By the time of the Emperor Augustus, the Roman government had access to detailed financial information.Some Hindus believe that the Indian Chanakya created a work similar to a financial management book, during the period of the Maurya Empire. His book ""Arthashasthra"" contains few detailed aspects of maintaining books of accounts for a Sovereign State. The Italian Luca Pacioli, recognized as The Father of accounting and bookeeping was the first person to publish a work on double-entry bookkeeping, which then developed in medieval Europe. Accounting began to transition into an organized profession in the nineteenth century, with local professional bodies in England merging to form the Institute of Chartered Accountants in England and Wales in 1880.