2015-230 Presentation of Financial Statements of Not-for

... b. Composition of net assets with donor restrictions at the end of the period and how the restrictions affect the use of resources. Disagree in part – narrative about how the composition affects the use of resources is subjective, may be duplicative of information already in the financials and adds ...

... b. Composition of net assets with donor restrictions at the end of the period and how the restrictions affect the use of resources. Disagree in part – narrative about how the composition affects the use of resources is subjective, may be duplicative of information already in the financials and adds ...

JOB PROFILE Position #00035655 Date: August 8, 2014 Title

... This position serves the Ministries of Agriculture, Environment, Energy and Mines, Natural Gas Development and Forests, Lands and Natural Resource Operations and ensures that revenues meet the objectives of Generally Accepted Accounting Principles (GAAP), government policy and legislation. This incl ...

... This position serves the Ministries of Agriculture, Environment, Energy and Mines, Natural Gas Development and Forests, Lands and Natural Resource Operations and ensures that revenues meet the objectives of Generally Accepted Accounting Principles (GAAP), government policy and legislation. This incl ...

Financial Management Policy

... Independent audit firms, affiliated with internationally renowned Audit firms, for approval in Annual General Meeting to conduct statutory audit of the foundation. Audit committee shall review Audit process, financial reporting and performance of the auditor to recommend in this regard to general ...

... Independent audit firms, affiliated with internationally renowned Audit firms, for approval in Annual General Meeting to conduct statutory audit of the foundation. Audit committee shall review Audit process, financial reporting and performance of the auditor to recommend in this regard to general ...

Breaking the Cycle of Fraud - Financial Executives International

... To break the fraud cycle, it is necessary to address all three sides of the Fraud Triangle when assessing the risk of fraud, and mitigating those risks within an organization. ...

... To break the fraud cycle, it is necessary to address all three sides of the Fraud Triangle when assessing the risk of fraud, and mitigating those risks within an organization. ...

Year 12 accounting term 2 internal controls

... the transactions (goods sold on credit, cash received and so on) that have occurred and is in the same form as a three-column ledger. Statements of account also help to ensure that the business’s records are correct, as most people receiving an incorrect statement will contact the firm. This, in con ...

... the transactions (goods sold on credit, cash received and so on) that have occurred and is in the same form as a three-column ledger. Statements of account also help to ensure that the business’s records are correct, as most people receiving an incorrect statement will contact the firm. This, in con ...

Assignment 1 is compulsory and due

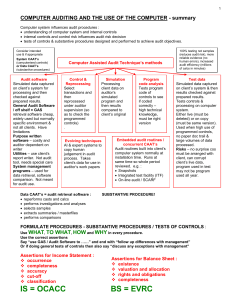

... and follow up differences with management GAS substantive procedures purchases (BS) – use audit software to : extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a ...

... and follow up differences with management GAS substantive procedures purchases (BS) – use audit software to : extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a ...

Audit Committee 18 September 2012

... Since the production of the draft accounts by 30 June 2012 they have been subject to external audit review for which the auditors report (ISA 260) is included as a separate item on this agenda. ...

... Since the production of the draft accounts by 30 June 2012 they have been subject to external audit review for which the auditors report (ISA 260) is included as a separate item on this agenda. ...

Managing Financial Aspects of a Business

... Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the phenomena that it purports to represent. To be a perfectly faithful representation, a depiction would have th ...

... Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the phenomena that it purports to represent. To be a perfectly faithful representation, a depiction would have th ...

documentation of the entity and its environment

... Have previous audits of this entity resulted in other than unqualified opinions? ___ Yes ___ No If yes, describe the reasons: ________________________________________________________________________ ________________________________________________________________________ ____________________________ ...

... Have previous audits of this entity resulted in other than unqualified opinions? ___ Yes ___ No If yes, describe the reasons: ________________________________________________________________________ ________________________________________________________________________ ____________________________ ...

III Local audit of project accounts

... state his position on them in his audit report: Principles of orderliness (financial regularity) Existence and adequacy and effectiveness of the Internal Control System (ICS) Conformity with the project objectives and adherence to the contract condition Economical conduct of business and eff ...

... state his position on them in his audit report: Principles of orderliness (financial regularity) Existence and adequacy and effectiveness of the Internal Control System (ICS) Conformity with the project objectives and adherence to the contract condition Economical conduct of business and eff ...

Leading Practice Examples of Audit Committee Reporting

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

Syllabus - Institute of Credit Management

... format. As computerised accounts are produced in this way CICM learners are already likely to have some experience of the continuous balance format before starting the course. Learners are required to prepare and recognise ledger accounts in this format in the examination and there will be no need f ...

... format. As computerised accounts are produced in this way CICM learners are already likely to have some experience of the continuous balance format before starting the course. Learners are required to prepare and recognise ledger accounts in this format in the examination and there will be no need f ...

Prior Year Adjustment (PYA)/Extraordinary Revenue

... <>

To determine which entry is appropriate guidelines for each type of entry are included:

Prior Year Adjustments (PYAs) are rare and shall only include adjustments meeting all

of the following characteristics:

(a) The value per occurrence must be in ...

... <

Ch. 15 – Vocabulary Review accounting generally accepted

... operating expenses, cash receipts, and outlays for a future time period. ...

... operating expenses, cash receipts, and outlays for a future time period. ...

EFFECTS OF INTERNAL CONTROLS ON REVENUE COLLECTION

... 4.1 Gender characteristics of respondents.........................................................................22 4.2 Education level of respondents....................................................................................23 4.3 Position held in the organisation......................... ...

... 4.1 Gender characteristics of respondents.........................................................................22 4.2 Education level of respondents....................................................................................23 4.3 Position held in the organisation......................... ...

Audited Financial Statements

... judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the organization's preparation and fair presentation of the financial statements i ...

... judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the organization's preparation and fair presentation of the financial statements i ...

Module 5 – Understanding the Basic Elements of School Board

... Net cost of services should be reported. The net economic resources (accumulated surplus/deficit) available to use in providing future services should be reported ...

... Net cost of services should be reported. The net economic resources (accumulated surplus/deficit) available to use in providing future services should be reported ...

Document

... protection, employee safety, hiring practices, and taxes. Companies must comply with different sets of regulations depending on the nature of their business. ...

... protection, employee safety, hiring practices, and taxes. Companies must comply with different sets of regulations depending on the nature of their business. ...

Hang Chi Holdings Limited 恒智控股有限公司

... 5.2 to be primarily responsible for making recommendations to the Board on the appointment, reappointment and removal of the external auditor, and to approve the remuneration and terms of engagement of the external auditor, and any questions of its resignation or dismissal; 5.3 to review and monit ...

... 5.2 to be primarily responsible for making recommendations to the Board on the appointment, reappointment and removal of the external auditor, and to approve the remuneration and terms of engagement of the external auditor, and any questions of its resignation or dismissal; 5.3 to review and monit ...

BRITISH BUSINESS BANK PLC Role Profile JOB TITLE Manager

... Assist in the preparation and analysis of regular reporting on SUL and other programme performance, including liaison with the Bank’s Management Information team. Working with the wider Lending Solutions team, produce bespoke key lender briefing reports for use by Senior Management when meeting key ...

... Assist in the preparation and analysis of regular reporting on SUL and other programme performance, including liaison with the Bank’s Management Information team. Working with the wider Lending Solutions team, produce bespoke key lender briefing reports for use by Senior Management when meeting key ...

Essential Keys to Nonprofit Finance

... the Statement of Financial Position and the Statement of Activities. These are typically unaudited. They help create a complete picture of the organization’s financial condition and status of resources that are available for use. The board should plan meetings shortly after the receipt of financial ...

... the Statement of Financial Position and the Statement of Activities. These are typically unaudited. They help create a complete picture of the organization’s financial condition and status of resources that are available for use. The board should plan meetings shortly after the receipt of financial ...

table of contents - Caritas University

... units and service centre of power holding company of Nigerian plc in Enugu state are often plagued by accounting and administrative control problems as it affect revenue generation and other assets. As a result the establishment revenue base has assumed a downward trend. It has also been shown that ...

... units and service centre of power holding company of Nigerian plc in Enugu state are often plagued by accounting and administrative control problems as it affect revenue generation and other assets. As a result the establishment revenue base has assumed a downward trend. It has also been shown that ...

Post(s): S7 Grade Syllabus Total No. of Questions

... Business laws-contract act Business laws-sale of goods act Company law Cost Accounting-Concepts Cost Accounting-Marginal costing Cost Accounting- Budgetary control Financial management-basic concepts Financial management-Ratio analysis Financial management-Cash Flow Statement Budgeting & Financial C ...

... Business laws-contract act Business laws-sale of goods act Company law Cost Accounting-Concepts Cost Accounting-Marginal costing Cost Accounting- Budgetary control Financial management-basic concepts Financial management-Ratio analysis Financial management-Cash Flow Statement Budgeting & Financial C ...