questions in real estate finance

... After several years the payments level off for the remainder of the term GPMs generally experience negative amortization in the early years Historically, FHA has had popular GPM programs Eliminating tilt effect allows borrowers to qualify for more funds Biggest problem is negative amortization and e ...

... After several years the payments level off for the remainder of the term GPMs generally experience negative amortization in the early years Historically, FHA has had popular GPM programs Eliminating tilt effect allows borrowers to qualify for more funds Biggest problem is negative amortization and e ...

What Caused This Mess? Bad Laws Built Up Over Time

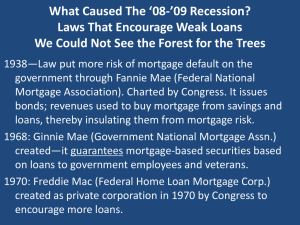

... What Caused The ‘08-’09 Recession? Laws That Encourage Weak Loans We Could Not See the Forest for the Trees 1938—Law put more risk of mortgage default on the government through Fannie Mae (Federal National Mortgage Association). Charted by Congress. It issues bonds; revenues used to buy mortgage fro ...

... What Caused The ‘08-’09 Recession? Laws That Encourage Weak Loans We Could Not See the Forest for the Trees 1938—Law put more risk of mortgage default on the government through Fannie Mae (Federal National Mortgage Association). Charted by Congress. It issues bonds; revenues used to buy mortgage fro ...

PowerPoint - Invest Ed

... • Spend no more than 2.5 times your annual salary on your mortgage. (total borrowing) • That means if I made $60K per year, I would aim for a mortgage less than $150,000 and a monthly payment of less than $1,050. (if I take home 70% of pay) ...

... • Spend no more than 2.5 times your annual salary on your mortgage. (total borrowing) • That means if I made $60K per year, I would aim for a mortgage less than $150,000 and a monthly payment of less than $1,050. (if I take home 70% of pay) ...

What does it mean? Common terms for home ownership factsheet

... either in the form of rent or capital gain. The owner does not live in the property. Joint tenants - Equal holding of a property between two or more persons. If one party dies, their share passes to the survivor/s. Lease - A document granting a period of tenancy of a property under specific terms a ...

... either in the form of rent or capital gain. The owner does not live in the property. Joint tenants - Equal holding of a property between two or more persons. If one party dies, their share passes to the survivor/s. Lease - A document granting a period of tenancy of a property under specific terms a ...

neophotonics corporation

... On February 25, 2015, NeoPhotonics Semiconductor GK (the “ Japanese Subsidiary ”), an indirect wholly-owned Japanese subsidiary of NeoPhotonics Corporation (the “ Company ”), entered into certain loan agreements and related special agreements (collectively, the “ Loan Documents ”) with The Bank of T ...

... On February 25, 2015, NeoPhotonics Semiconductor GK (the “ Japanese Subsidiary ”), an indirect wholly-owned Japanese subsidiary of NeoPhotonics Corporation (the “ Company ”), entered into certain loan agreements and related special agreements (collectively, the “ Loan Documents ”) with The Bank of T ...

REAL ESTATE SETTLEMENT PROCEDURES ACT (RESPA) T E

... The Real Estate Settlement Procedures Act of 1974 (12 USC § 2601) (“RESPA”), together with HUD’s Regulation X (24 CFR § 3500) promulgated by the Department of Housing & Urban Development (“HUD”), seeks to create a uniform disclosure and settlement procedure for residential mortgage transactions. RES ...

... The Real Estate Settlement Procedures Act of 1974 (12 USC § 2601) (“RESPA”), together with HUD’s Regulation X (24 CFR § 3500) promulgated by the Department of Housing & Urban Development (“HUD”), seeks to create a uniform disclosure and settlement procedure for residential mortgage transactions. RES ...

Why Can`t My Bank Help Me?

... rules and regulations are ever changing. Banks are required to reserve part of their profits to cover bad loans or bad debt. If collateral is attached to a loan – for example, a car is used to secure an auto loan – the car can always be sold off to pay off as much of the loan as possible. A plan is ...

... rules and regulations are ever changing. Banks are required to reserve part of their profits to cover bad loans or bad debt. If collateral is attached to a loan – for example, a car is used to secure an auto loan – the car can always be sold off to pay off as much of the loan as possible. A plan is ...