The Impact of Collateral

... says Jennis. “Systems need to look at the type of collateral and what is accessible. They need reports in terms of concentration such as are available on GlobalCollateral’s Collateral Management Utility. They need to do it more frequently: daily and intraday.” The paper reported that half of the fir ...

... says Jennis. “Systems need to look at the type of collateral and what is accessible. They need reports in terms of concentration such as are available on GlobalCollateral’s Collateral Management Utility. They need to do it more frequently: daily and intraday.” The paper reported that half of the fir ...

CBOE Holdings, Inc. Annual Report 2012 40 Years of Innovation

... April commemorates the 40th anniversary of the Chicago Board Options Exchange (CBOE) and the U.S. options industry. For four decades, CBOE has been the undisputed options innovator, with nearly every major industry “first” conceived by CBOE. The creation of listed options in 1973; index options in 1 ...

... April commemorates the 40th anniversary of the Chicago Board Options Exchange (CBOE) and the U.S. options industry. For four decades, CBOE has been the undisputed options innovator, with nearly every major industry “first” conceived by CBOE. The creation of listed options in 1973; index options in 1 ...

Endogenous Tick Sizes, Bid-Ask Spreads, Depth, and Trading Volumes

... The Stock Exchange of Thailand (SET) is operated as a pure order-driven market, similar to the SSE. However, the trading on the SET is displayed anonymously, unlike the transparency of order origination displayed in the SSE. Concluding that the various mandatory tick size rule used by SET could aff ...

... The Stock Exchange of Thailand (SET) is operated as a pure order-driven market, similar to the SSE. However, the trading on the SET is displayed anonymously, unlike the transparency of order origination displayed in the SSE. Concluding that the various mandatory tick size rule used by SET could aff ...

The impact of stock recommendations given on Dutch television

... Through various media, investors have access to an enormous amount of information. Why do investors take some stocks into consideration and not others? Barber and Odean (2008) state: “When there are many alternatives, options that attract attention are more likely to be considered, hence more likely ...

... Through various media, investors have access to an enormous amount of information. Why do investors take some stocks into consideration and not others? Barber and Odean (2008) state: “When there are many alternatives, options that attract attention are more likely to be considered, hence more likely ...

Philippine Bond Market Guide

... (ADB consultant), and Matthias Schmidt (ADB consultant), The ADB Team would also like to express our sincere gratitude to the Philippine Working Group (PWG). The PWG was composed of public and private sector representatives. The public sector was represented by the Department of Finance, Bangko Sent ...

... (ADB consultant), and Matthias Schmidt (ADB consultant), The ADB Team would also like to express our sincere gratitude to the Philippine Working Group (PWG). The PWG was composed of public and private sector representatives. The public sector was represented by the Department of Finance, Bangko Sent ...

Active CDS Trading and Managers` Voluntary Disclosure

... also find that the effect of liquid CDSs on forecasting strengthens with negative credit news, as measured by an increase in abnormal CDS spreads, further suggesting that unobservable firm characteristics correlated with CDS liquidity are unlikely to drive forecasting behavior. Next, we validate th ...

... also find that the effect of liquid CDSs on forecasting strengthens with negative credit news, as measured by an increase in abnormal CDS spreads, further suggesting that unobservable firm characteristics correlated with CDS liquidity are unlikely to drive forecasting behavior. Next, we validate th ...

2 Economic analysis of the pricing of market data services

... The first part focuses on the costs of market data services to brokers. It shows that the order of magnitude of these costs, compared with trade execution costs, can vary significantly by broker. This is not surprising and is driven by the pricing schedules as well as the fact that different broker ...

... The first part focuses on the costs of market data services to brokers. It shows that the order of magnitude of these costs, compared with trade execution costs, can vary significantly by broker. This is not surprising and is driven by the pricing schedules as well as the fact that different broker ...

UBS ATS Monthly Volume Summary – November 2016 (restated 1

... Average firm up quantity Average firm up minimum quantity Average executed quantity ...

... Average firm up quantity Average firm up minimum quantity Average executed quantity ...

TRANSMISSION OF INFORMATION ACROSS INTERNATIONAL

... liquidity-based price movements, which are normally related to high trading volume, can also be transmitted across borders and have a global impact on market performance in other countries. Last but not least, this study explores the economic significance of international information spillovers and ...

... liquidity-based price movements, which are normally related to high trading volume, can also be transmitted across borders and have a global impact on market performance in other countries. Last but not least, this study explores the economic significance of international information spillovers and ...

Option Trading, Reference Prices, and Volatility Kelley Bergsma

... sell extreme losing positions. Ben-David and Hirshleifer (2012) and An (2016) find a V-shaped disposition effect whereby investors sell stocks with large gains and large losses. Moreover, Chang, Solomon, and Westerfield (2016) document that investors at a large discount broker tend to exhibit a clas ...

... sell extreme losing positions. Ben-David and Hirshleifer (2012) and An (2016) find a V-shaped disposition effect whereby investors sell stocks with large gains and large losses. Moreover, Chang, Solomon, and Westerfield (2016) document that investors at a large discount broker tend to exhibit a clas ...

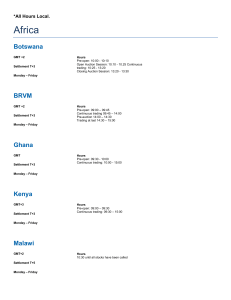

Global Trading Hours

... In Trading At Last, shares can be traded at their respective closing prices. This only applies for certain securities. Special Auction Double fixing stocks trade from 11:30 to 16:30. Single fixing stocks trade at designated auction periods depending on the trading group it belongs to. After each fix ...

... In Trading At Last, shares can be traded at their respective closing prices. This only applies for certain securities. Special Auction Double fixing stocks trade from 11:30 to 16:30. Single fixing stocks trade at designated auction periods depending on the trading group it belongs to. After each fix ...

Good news-Bad news: Information revelation

... I.1. Reaction to news in financial markets Recent research in behavioral finance has challenged the predictions of standard finance models putting forward the existence of financial anomalies such as the over- and under-reaction of asset prices to news. In their classic study, DeBondt and Thaler (19 ...

... I.1. Reaction to news in financial markets Recent research in behavioral finance has challenged the predictions of standard finance models putting forward the existence of financial anomalies such as the over- and under-reaction of asset prices to news. In their classic study, DeBondt and Thaler (19 ...

Regulation and Market Liquidity - University of British Columbia

... bonds. Our tests robustly capture breaks in latent liquidity dynamics at the start and at the end of the 2008-09 crisis (and indeed these tests can be employed to precisely time the beginning and end of the liquidity crisis). This reassures us on the tests having sufficient power within this specif ...

... bonds. Our tests robustly capture breaks in latent liquidity dynamics at the start and at the end of the 2008-09 crisis (and indeed these tests can be employed to precisely time the beginning and end of the liquidity crisis). This reassures us on the tests having sufficient power within this specif ...

Decimals and Liquidity: A study of the NYSE

... liquidity. Opponents claim that decimals will result in less liquid, high-volatility markets. Our results, however, provide a mixed verdict on the issue of liquidity and volatility. At the very least, information about the available supply and demand schedule outside the BBO must be made available t ...

... liquidity. Opponents claim that decimals will result in less liquid, high-volatility markets. Our results, however, provide a mixed verdict on the issue of liquidity and volatility. At the very least, information about the available supply and demand schedule outside the BBO must be made available t ...

Proceedings of 7th Annual American Business Research Conference

... In order to account for the cause of the fall in stock prices due to delisting, Sanger and Peterson (1990) and Macey, O'Hara, and Pompilo (2008) among others propose the liquidity hypothesis. Noting that the bid-ask spread triples and the volatility doubles in the OTC market after involuntary delist ...

... In order to account for the cause of the fall in stock prices due to delisting, Sanger and Peterson (1990) and Macey, O'Hara, and Pompilo (2008) among others propose the liquidity hypothesis. Noting that the bid-ask spread triples and the volatility doubles in the OTC market after involuntary delist ...

Informed Trading, Liquidity Provision, and Stock Selection by Mutual

... performance for a manager who attained such performance by trading stocks associated with more information events, i.e., we should expect stronger fund performance persistence among funds that traded in High-P IN stocks recently. Consistent with that conjecture, when we combine our trade_P IN variab ...

... performance for a manager who attained such performance by trading stocks associated with more information events, i.e., we should expect stronger fund performance persistence among funds that traded in High-P IN stocks recently. Consistent with that conjecture, when we combine our trade_P IN variab ...

How volatile are East Asian stocks during high volatility periods?*

... be higher when compared to estimates that assume a 2-state process. As can be gleaned from Table 3, Indonesia’s high volatility index now stands at 34 times its normal level. An interesting result that is obtained in the estimates is the indices derived for Malaysia and Singapore. The numbers indica ...

... be higher when compared to estimates that assume a 2-state process. As can be gleaned from Table 3, Indonesia’s high volatility index now stands at 34 times its normal level. An interesting result that is obtained in the estimates is the indices derived for Malaysia and Singapore. The numbers indica ...

Merrill Edge® Self-Directed Investing Terms of Service

... self-directed basis through Merrill Lynch, Pierce, Fenner & Smith Incorporated (“Merrill Lynch”). For the purpose of the Merrill Edge Self-Directed Terms of Service, Merrill Edge and MESD, which are made available through Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), refer to certai ...

... self-directed basis through Merrill Lynch, Pierce, Fenner & Smith Incorporated (“Merrill Lynch”). For the purpose of the Merrill Edge Self-Directed Terms of Service, Merrill Edge and MESD, which are made available through Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), refer to certai ...

Day Trading the Currency Market

... “I thought this was one of the best books that I had read on FX. The book should be required reading not only for traders new to the foreign exchange markets, but also for seasoned professionals. I’ll definitely be keeping it on my desk for reference. The book is very readable and very educational. ...

... “I thought this was one of the best books that I had read on FX. The book should be required reading not only for traders new to the foreign exchange markets, but also for seasoned professionals. I’ll definitely be keeping it on my desk for reference. The book is very readable and very educational. ...

What types of investors drive commonality in

... and Viswanathan (2010), estimating the strength of commonality through sensitivity of changes in individual stock liquidity to changes in market liquidity. Second, following methodology by Chordia et al. (2000) we measure commonality in liquidity through the level of explanatory power when regressin ...

... and Viswanathan (2010), estimating the strength of commonality through sensitivity of changes in individual stock liquidity to changes in market liquidity. Second, following methodology by Chordia et al. (2000) we measure commonality in liquidity through the level of explanatory power when regressin ...

Issue 1. Volatility as an Asset Class and Dynamic Asset Allocation

... In practice the determination as to how much volatility to add is part of a larger strategic asset allocation and portfolio construction exercise, as other objectives, risk constraints and considerations need to be taken into account. It is also important to note that we would not hold a static perc ...

... In practice the determination as to how much volatility to add is part of a larger strategic asset allocation and portfolio construction exercise, as other objectives, risk constraints and considerations need to be taken into account. It is also important to note that we would not hold a static perc ...

Chicago Board of Trade (CBOT)

... To Hedge With Financial Futures: • Choose the contract that most closely describes the nature of the underlying risk • Choose the expiration month that most closely matches the time period to be addressed • Buy or sell the appropriate number of futures contracts to cover your exposure October 12, 20 ...

... To Hedge With Financial Futures: • Choose the contract that most closely describes the nature of the underlying risk • Choose the expiration month that most closely matches the time period to be addressed • Buy or sell the appropriate number of futures contracts to cover your exposure October 12, 20 ...

Interacting Limit Order Demand and Supply Curves

... product markets, demand elasticity depends on factors such as consumer preferences; while supply elasticity depends on factors such as production technologies and market power. In contrast, at least in the short-run, stock markets resemble a pure exchange economy: buyers become sellers and vice-vers ...

... product markets, demand elasticity depends on factors such as consumer preferences; while supply elasticity depends on factors such as production technologies and market power. In contrast, at least in the short-run, stock markets resemble a pure exchange economy: buyers become sellers and vice-vers ...

Dynamic Allocation Strategies using Minimum Volatility

... style in the most desirable time periods. The results indicate that the possibility exists for passive and active managers to add value through their ability to dynamically allocate capital. However, there are risks accompanying these strategies which must be weighed against any potential benefits. ...

... style in the most desirable time periods. The results indicate that the possibility exists for passive and active managers to add value through their ability to dynamically allocate capital. However, there are risks accompanying these strategies which must be weighed against any potential benefits. ...

Does Supply Curve Inelasticity Explain Abnormal Long

... allows them to identify periodic undervaluation, then they can buy strategically at those times and earn higher returns than outside investors. If this is the case, then other traders should not be able to replicate firms’ performance unless they can exactly copy the timing and magnitude of firms’ ...

... allows them to identify periodic undervaluation, then they can buy strategically at those times and earn higher returns than outside investors. If this is the case, then other traders should not be able to replicate firms’ performance unless they can exactly copy the timing and magnitude of firms’ ...