Chap 2 Stock Market Indices Stock Market Indices

... Value-Weighted Stock Market Indices • The value-weighted indexes are (deservedly in biased toward the companies with the highest stock market value: a move in Intel will affect the S&P500 more than a move in MMM. • The index is the sum of today’s “total cap” of the 500 stocks divided by the total c ...

... Value-Weighted Stock Market Indices • The value-weighted indexes are (deservedly in biased toward the companies with the highest stock market value: a move in Intel will affect the S&P500 more than a move in MMM. • The index is the sum of today’s “total cap” of the 500 stocks divided by the total c ...

REITs` mean reversion presents trading opportunities

... REITs behave differently from other stocks by exhibiting a higher tendency to revert-to-the-mean. This means that REITs that have delivered outsized returns relative to peers during one month, tend to lag in the following month. The main reason for this behaviour is that REITs, for the most part, do ...

... REITs behave differently from other stocks by exhibiting a higher tendency to revert-to-the-mean. This means that REITs that have delivered outsized returns relative to peers during one month, tend to lag in the following month. The main reason for this behaviour is that REITs, for the most part, do ...

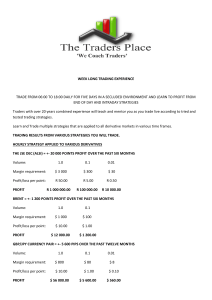

week long trading experience trade from 06:00 to 18:00 daily for five

... trading. He later joined Ideal CFD’s a CFD provider that was bought by IG Markets, he remained with IG as head Market Analyst and Client education for South Africa until December 2011. In January 2012 Warren started coaching other traders in Technical analysis, systems building and leveraged trading ...

... trading. He later joined Ideal CFD’s a CFD provider that was bought by IG Markets, he remained with IG as head Market Analyst and Client education for South Africa until December 2011. In January 2012 Warren started coaching other traders in Technical analysis, systems building and leveraged trading ...

short selling regulations

... Designated Securities provided he has first obtained the approval of the Chairman of the Board, which may be given either orally or in writing. Notice of such restriction or prohibition to the Exchange Participant, whether oral or written, shall take effect immediately upon communication to or servi ...

... Designated Securities provided he has first obtained the approval of the Chairman of the Board, which may be given either orally or in writing. Notice of such restriction or prohibition to the Exchange Participant, whether oral or written, shall take effect immediately upon communication to or servi ...

Amazing Market Why does the stock market exist? The answer

... (AMEX) and the New York Stock Exchange (NYSE) are the two biggest auction markets in the United States.2Owned by its members, AMEX lists many fewer stocks than the NYSE, but it has pioneered the development of exchange traded funds (ETFs) and specialized in trading options, which are special rights ...

... (AMEX) and the New York Stock Exchange (NYSE) are the two biggest auction markets in the United States.2Owned by its members, AMEX lists many fewer stocks than the NYSE, but it has pioneered the development of exchange traded funds (ETFs) and specialized in trading options, which are special rights ...

FREE Sample Here

... B. They let everyone know who is making the trade and at what price c. They provide the ability to trade after hours when the exchanges are closed ...

... B. They let everyone know who is making the trade and at what price c. They provide the ability to trade after hours when the exchanges are closed ...

FAQ Power Exchange - Tata Power Trading Company Ltd.

... All purchase bids and sale offers are aggregated in the unconstrained scenario. The aggregate supply and demand curves are drawn on Price-Quantity axes. The intersection point of the two curves gives Market Clearing Price (MCP) and Market Clearing Volume (MCV) corresponding to price and quantity of ...

... All purchase bids and sale offers are aggregated in the unconstrained scenario. The aggregate supply and demand curves are drawn on Price-Quantity axes. The intersection point of the two curves gives Market Clearing Price (MCP) and Market Clearing Volume (MCV) corresponding to price and quantity of ...

Transaction Costs, Trade Throughs, and Riskless Principal Trading

... • Small traders and many institutional traders trade at a disadvantage because they do not know market prices as well as dealers do. • Transaction costs are high in bond markets in comparison to transaction costs in equities. – Risk considerations suggest the opposite. ...

... • Small traders and many institutional traders trade at a disadvantage because they do not know market prices as well as dealers do. • Transaction costs are high in bond markets in comparison to transaction costs in equities. – Risk considerations suggest the opposite. ...

Heterogeneous Beliefs under Different Market Architectures

... a finite number of predictors of future price according to the past performance of the predictors. It turns out that when the intensity of choice is high, the price time series may deviate from a fundamental benchmark in a systematic way, become chaotic and exhibit excess volatility and volatility c ...

... a finite number of predictors of future price according to the past performance of the predictors. It turns out that when the intensity of choice is high, the price time series may deviate from a fundamental benchmark in a systematic way, become chaotic and exhibit excess volatility and volatility c ...

DOC - Europa.eu

... markets." (see also the statement) Between 2008 and 2013, OPCOM required members of the spot electricity markets to have a Romanian VAT registration, refusing to accept traders that were already registered for VAT in other EU Member States. As a result, EU traders could only enter the Romanian whole ...

... markets." (see also the statement) Between 2008 and 2013, OPCOM required members of the spot electricity markets to have a Romanian VAT registration, refusing to accept traders that were already registered for VAT in other EU Member States. As a result, EU traders could only enter the Romanian whole ...

2010 Flash Crash

The May 6, 2010, Flash Crash also known as The Crash of 2:45, the 2010 Flash Crash or simply the Flash Crash, was a United States trillion-dollar stock market crash, which started at 2:32 and lasted for approximately 36 minutes. Stock indexes, such as the S&P 500, Dow Jones Industrial Average and Nasdaq 100, collapsed and rebounded very rapidly.The Dow Jones Industrial Average had its biggest intraday point drop (from the opening) up to that point, plunging 998.5 points (about 9%), most within minutes, only to recover a large part of the loss. It was also the second-largest intraday point swing (difference between intraday high and intraday low) up to that point, at 1,010.14 points. The prices of stocks, stock index futures, options and ETFs were volatile, thus trading volume spiked. A CFTC 2014 report described it as one of the most turbulent periods in the history of financial markets.On April 21, 2015, nearly five years after the incident, the U.S. Department of Justice laid ""22 criminal counts, including fraud and market manipulation"" against Navinder Singh Sarao, a trader. Among the charges included was the use of spoofing algorithms; just prior to the Flash Crash, he placed thousands of E-mini S&P 500 stock index futures contracts which he planned on canceling later. These orders amounting to about ""$200 million worth of bets that the market would fall"" were ""replaced or modified 19,000 times"" before they were canceled. Spoofing, layering and front-running are now banned.The Commodity Futures Trading Commission (CFTC) investigation concluded that Sarao ""was at least significantly responsible for the order imbalances"" in the derivatives market which affected stock markets and exacerbated the flash crash. Sarao began his alleged market manipulation in 2009 with commercially available trading software whose code he modified ""so he could rapidly place and cancel orders automatically."" Traders Magazine journalist, John Bates, argued that blaming a 36-year-old small-time trader who worked from his parents' modest stucco house in suburban west London for sparking a trillion-dollar stock market crash is a little bit like blaming lightning for starting a fire"" and that the investigation was lengthened because regulators used ""bicycles to try and catch Ferraris."" Furthermore, he concluded that by April 2015, traders can still manipulate and impact markets in spite of regulators and banks' new, improved monitoring of automated trade systems.As recently as May 2014, a CFTC report concluded that high-frequency traders ""did not cause the Flash Crash, but contributed to it by demanding immediacy ahead of other market participants.""Recent research shows that Flash Crashes are not isolated occurrences, but have occurred quite often over the past century. For instance, Irene Aldridge, the author of High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems, 2nd ed., Wiley & Sons, shows that Flash Crashes have been frequent and their causes predictable in market microstructure analysis.