Chapter 6 Efficiency and Fairness of Markets

... not change, then the marginal benefit of that good does not change. Hence an increase in the price decreases the consumer surplus from that good because 1) it decreases the quantity purchased, and 2) it decreases the consumer surplus on each particular unit that is purchased. Topic: Consumer surplus ...

... not change, then the marginal benefit of that good does not change. Hence an increase in the price decreases the consumer surplus from that good because 1) it decreases the quantity purchased, and 2) it decreases the consumer surplus on each particular unit that is purchased. Topic: Consumer surplus ...

Market Power: Monopoly and Monopsony

... Therefore, as demand becomes more elastic (Ed becomes more negative), the markup percentage becomes smaller. For example, if Ed changes from 2 to 5, the markup decreases from 0.5 to 0.2. This tells us that the firm has less power to mark up its price above marginal cost when it faces a more elasti ...

... Therefore, as demand becomes more elastic (Ed becomes more negative), the markup percentage becomes smaller. For example, if Ed changes from 2 to 5, the markup decreases from 0.5 to 0.2. This tells us that the firm has less power to mark up its price above marginal cost when it faces a more elasti ...

ECON 3070 Intermediate Microeconomic Theory Practice Multiple

... 17. If a market basket is changed by adding more to at least one of the goods, then every consumer will a. rank the market basket more highly after the change. b. rank the market basket more highly before the change. c. rank the market basket just as desirable after the change. d. be unable to deci ...

... 17. If a market basket is changed by adding more to at least one of the goods, then every consumer will a. rank the market basket more highly after the change. b. rank the market basket more highly before the change. c. rank the market basket just as desirable after the change. d. be unable to deci ...

wk1_ch02-sp12

... The effect of one good’s prices on the demand for another good is the cross-price elasticity, and with the particular utility function we are using here, that cross-price elasticity is zero. Typically, however, a change in the price of one good will affect demand for other goods as well. Public Fi ...

... The effect of one good’s prices on the demand for another good is the cross-price elasticity, and with the particular utility function we are using here, that cross-price elasticity is zero. Typically, however, a change in the price of one good will affect demand for other goods as well. Public Fi ...

Producer Choice - The Costs of Production

... total cost would rise if output were increased by one unit. The marginal cost always rises with the quantity of output. Average cost first falls as output increases and then rises. ...

... total cost would rise if output were increased by one unit. The marginal cost always rises with the quantity of output. Average cost first falls as output increases and then rises. ...

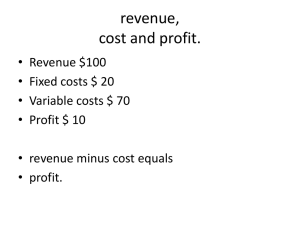

Profit and the Firm

... • When economic profit is equal to zero, business profit is equal to “normal” profit. • When a firm is making less than a normal profit it may consider leaving the industry in long run while it may continue operation in the short run ...

... • When economic profit is equal to zero, business profit is equal to “normal” profit. • When a firm is making less than a normal profit it may consider leaving the industry in long run while it may continue operation in the short run ...

production theory - Clemson University

... across its scale of output. It is useful to draw the long and short run curves paying careful attention to the association of long-run and short-run marginal costs. Notice the particularly striking case where long-run average cost is falling. Short-run average cost is tangent to the longrun function ...

... across its scale of output. It is useful to draw the long and short run curves paying careful attention to the association of long-run and short-run marginal costs. Notice the particularly striking case where long-run average cost is falling. Short-run average cost is tangent to the longrun function ...

Bertrand Equilibrium with Increasing Marginal Costs

... In the equilibrium both firms name P= PE and obtain the demand D(PE)/2. Suppose that firm 1 raises its price.→The profit is zero, so it has no incentive for raising its price. Suppose that firm 1 reduces its price. →It obtains the demand D(P1). Since PE =C1'(D(PE)/2), the profit is maximized given t ...

... In the equilibrium both firms name P= PE and obtain the demand D(PE)/2. Suppose that firm 1 raises its price.→The profit is zero, so it has no incentive for raising its price. Suppose that firm 1 reduces its price. →It obtains the demand D(P1). Since PE =C1'(D(PE)/2), the profit is maximized given t ...

PROFIT MAXIMIZATION BY A MONOPOLIST A - Course ON-LINE

... Barriers to entry can be structural, legal, or strategic. Structural barriers to entry exist when incumbent firms have cost or marketing advantages that would make it unattractive for a new firm to enter the industry and compete against them. The interaction of economies of scale and market demand t ...

... Barriers to entry can be structural, legal, or strategic. Structural barriers to entry exist when incumbent firms have cost or marketing advantages that would make it unattractive for a new firm to enter the industry and compete against them. The interaction of economies of scale and market demand t ...