rlp/blackrock aquila over 5 years index linked gilt

... The Fund Volatility figure shown is the annualised standard deviation of he monthly returns on the fund over a 3 year time period to 31.12.2014. Standard deviation is a measure of the spread of monthly returns around the average (mean) return. A higher volatility figure indicates that the fund has p ...

... The Fund Volatility figure shown is the annualised standard deviation of he monthly returns on the fund over a 3 year time period to 31.12.2014. Standard deviation is a measure of the spread of monthly returns around the average (mean) return. A higher volatility figure indicates that the fund has p ...

Chapter 5 Understanding Risk - McGraw Hill Higher Education

... • Sometimes we are less concerned with spread than with the worst possible outcome • Example: We don’t want a bank to fail ...

... • Sometimes we are less concerned with spread than with the worst possible outcome • Example: We don’t want a bank to fail ...

Emerging Market Equity Fund Investor: SEMNX SEMNX | Advisor: SEMVX SEMVX

... year period (out of 591 funds), 3 stars for the 5 year period (out of 410 funds), 4 stars for the 10 year period (out of 179 funds) within the Diversified Emerging Mkts category. For each fund with at least a 3-year history, Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-A ...

... year period (out of 591 funds), 3 stars for the 5 year period (out of 410 funds), 4 stars for the 10 year period (out of 179 funds) within the Diversified Emerging Mkts category. For each fund with at least a 3-year history, Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-A ...

1 - JustAnswer

... levered firm (III) an all-equity firm (Points: 5) I only II only III only I and III only 38. When comparing levered vs. unlevered capital structures, leverage works to increase EPS for high levels of operating income because ______. (Points: 5) interest payments on the debt vary with EBIT levels int ...

... levered firm (III) an all-equity firm (Points: 5) I only II only III only I and III only 38. When comparing levered vs. unlevered capital structures, leverage works to increase EPS for high levels of operating income because ______. (Points: 5) interest payments on the debt vary with EBIT levels int ...

UNIVERSITY OF NORTH FLORIDA

... OFG faced two major issues in Q4 as it entered the fixed income markets: the likelihood of a recession and the rare occurrence of an inverted yield curve, which was increasing in its depth of inversion. The recession issue has yet to be resolved, but it has triggered a belief that based on a weakeni ...

... OFG faced two major issues in Q4 as it entered the fixed income markets: the likelihood of a recession and the rare occurrence of an inverted yield curve, which was increasing in its depth of inversion. The recession issue has yet to be resolved, but it has triggered a belief that based on a weakeni ...

Document

... The Appeal of Common Stocks Residual Owners: stockholders of a firm are the owners, who are entitled to dividend income and a prorated share of the firm’s earnings only after all the firm’s other obligations have been met Stocks allow investors to tailor investments to meet individual needs and ...

... The Appeal of Common Stocks Residual Owners: stockholders of a firm are the owners, who are entitled to dividend income and a prorated share of the firm’s earnings only after all the firm’s other obligations have been met Stocks allow investors to tailor investments to meet individual needs and ...

search for yield

... models. However, one possible and more short-term alternative is to invest in higherrisk assets (Antolin et al, 2011). Another reason for the search for yield is the fund manager’s compensation system which may mean that the potential financial advantages of increased risk taking are greater than th ...

... models. However, one possible and more short-term alternative is to invest in higherrisk assets (Antolin et al, 2011). Another reason for the search for yield is the fund manager’s compensation system which may mean that the potential financial advantages of increased risk taking are greater than th ...

Impact Of Short Selling Activity On Market Dynamics

... sales ratio to examine the short selling activity at Borsa Istanbul.1 Construction of such measure allows us to focus on variation over time in short sales to which previous work has not paid much attention. Using also BIST100 market return and measures of liquidity and volatility, we investigate ho ...

... sales ratio to examine the short selling activity at Borsa Istanbul.1 Construction of such measure allows us to focus on variation over time in short sales to which previous work has not paid much attention. Using also BIST100 market return and measures of liquidity and volatility, we investigate ho ...

The Leverage Rotation Strategy

... and return. Low volatility stocks have exhibited above market performance with lower than market Beta, challenging the risk/return laws of the CAPM.2 Similarly perplexing is the tendency for high beta stocks to exhibit lower performance than predicted by their level of risk.3 In this paper, we propo ...

... and return. Low volatility stocks have exhibited above market performance with lower than market Beta, challenging the risk/return laws of the CAPM.2 Similarly perplexing is the tendency for high beta stocks to exhibit lower performance than predicted by their level of risk.3 In this paper, we propo ...

Constant Proportion Portfolio Insurance in presence

... between the value of the multiplier m and the risk of the insured portfolio, which allows to choose the multiplier based on the risk tolerance of the investor, and provide a Fourier transform method for computing the distribution of losses and various risk measures (VaR, expected loss, probability ...

... between the value of the multiplier m and the risk of the insured portfolio, which allows to choose the multiplier based on the risk tolerance of the investor, and provide a Fourier transform method for computing the distribution of losses and various risk measures (VaR, expected loss, probability ...

CEO ownership, stock market performance, and managerial discretion

... The second explanation is based on the interplay of value increasing effort of the CEO and irrational markets. The main idea is that high managerial ownership induces the CEO to work harder; incentives between the CEO and outside investors are better aligned. In other words, owner-CEOs are value inc ...

... The second explanation is based on the interplay of value increasing effort of the CEO and irrational markets. The main idea is that high managerial ownership induces the CEO to work harder; incentives between the CEO and outside investors are better aligned. In other words, owner-CEOs are value inc ...

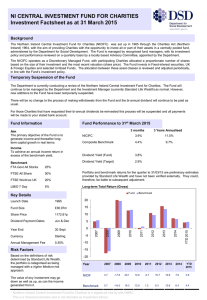

NORTHERN IRELAND CENTRAL INVESTMENT FUND FOR CHARITIES

... has been here before when a negative economic backdrop can result in a positive outcome for financial assets. The US economy ticks along nicely although growth forecasts have been trimmed. Unemployment continues to fall as does inflation (largely helped by the oil price decline) and speculation grow ...

... has been here before when a negative economic backdrop can result in a positive outcome for financial assets. The US economy ticks along nicely although growth forecasts have been trimmed. Unemployment continues to fall as does inflation (largely helped by the oil price decline) and speculation grow ...

after-tax returns: methodology for computing

... APPENDIX: SHADOW BENCHMARK The shadow benchmark can be thought of as a simulated account which shadows the actual account’s investment flows, returns, and market value over time. As with all simulations, it makes some simplifying assumptions. It models the evolution of a single-security investment, ...

... APPENDIX: SHADOW BENCHMARK The shadow benchmark can be thought of as a simulated account which shadows the actual account’s investment flows, returns, and market value over time. As with all simulations, it makes some simplifying assumptions. It models the evolution of a single-security investment, ...

Vanguard`s framework for constructing globally diversified portfolios

... Although no one can predict which individual investments will do best in the future, we believe that the best strategy for long-term success is to have a well-thoughtout plan with an emphasis on balance and diversification and a focus on keeping costs low and maintaining discipline (Vanguard, 2013). ...

... Although no one can predict which individual investments will do best in the future, we believe that the best strategy for long-term success is to have a well-thoughtout plan with an emphasis on balance and diversification and a focus on keeping costs low and maintaining discipline (Vanguard, 2013). ...

columbia us treasury index fund

... Investment risks — Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. The U.S. Government may be unable or unwilling to honor its financial obligations. Securities issued or guaranteed by federal agencies and U.S. government-sponsored instrumentalities ...

... Investment risks — Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. The U.S. Government may be unable or unwilling to honor its financial obligations. Securities issued or guaranteed by federal agencies and U.S. government-sponsored instrumentalities ...

FRBSF L CONOMIC

... the opposite sign of that predicted by the theory (Engsted and Pedersen 2012). Indeed, in the most recent U.S. housing boom, the high house price-to-rent ratio observed during the boom did not foreshadow subsequent high real rent growth. In fact, the growth rate of real rents actually declined in th ...

... the opposite sign of that predicted by the theory (Engsted and Pedersen 2012). Indeed, in the most recent U.S. housing boom, the high house price-to-rent ratio observed during the boom did not foreshadow subsequent high real rent growth. In fact, the growth rate of real rents actually declined in th ...

Monte Carlo Simulation

... to the inputs. This is an extremely important step that should not be overlooked. Comparing Data – MVO vs. Monte Carlo Simulation It is very important to analyze your data. Figures 2 and 3 show an example of possible differences that may occur when using a Monte Carlo simulation instead of MVO. Mont ...

... to the inputs. This is an extremely important step that should not be overlooked. Comparing Data – MVO vs. Monte Carlo Simulation It is very important to analyze your data. Figures 2 and 3 show an example of possible differences that may occur when using a Monte Carlo simulation instead of MVO. Mont ...

www.FirstRate.com | Evaluating Performance of Alternative

... own individual investment strategy that focuses on investments appropriate for that specific strategy. Hedge funds are generally available to a limited number of qualified investors who pay performance fees to the fund managers. The five most widely used strategies account for close to 90 percent of ...

... own individual investment strategy that focuses on investments appropriate for that specific strategy. Hedge funds are generally available to a limited number of qualified investors who pay performance fees to the fund managers. The five most widely used strategies account for close to 90 percent of ...

Stock Fundamentals 2010

... Operating Leverage is characterized by the slope of profit/sales graph of the project. Consider a small wine seller who is evaluating two alternative processes for producing wine: Process A which would cost $120,000 to buy and install and would have a variable cost of $0.57/bottle; Process B which w ...

... Operating Leverage is characterized by the slope of profit/sales graph of the project. Consider a small wine seller who is evaluating two alternative processes for producing wine: Process A which would cost $120,000 to buy and install and would have a variable cost of $0.57/bottle; Process B which w ...

Document

... price of options for the next 30 days. With a higher number, there is a less chance of the market going up. ...

... price of options for the next 30 days. With a higher number, there is a less chance of the market going up. ...

Key Information Document

... information such as the latest price for the shares are available at the registered office of ADCB SICAV, 1, rue du Potager, L-2347 Luxembourg and on the following website www.adcb.com. Prospective investors should inform themselves as to the tax consequences within the countries of their residence ...

... information such as the latest price for the shares are available at the registered office of ADCB SICAV, 1, rue du Potager, L-2347 Luxembourg and on the following website www.adcb.com. Prospective investors should inform themselves as to the tax consequences within the countries of their residence ...

3.4. Officer and Hathaway (1999) Regression Results

... Appendix 3. Estimation of the utilisation factor . This appendix explains how the various Australian studies cited in our report (Brown and Clarke (1993), Hathaway and Officer (1999) and McKinsey (1994)) are used to derive estimates of the franking credit “utilisation factor” . Section 3.1 prese ...

... Appendix 3. Estimation of the utilisation factor . This appendix explains how the various Australian studies cited in our report (Brown and Clarke (1993), Hathaway and Officer (1999) and McKinsey (1994)) are used to derive estimates of the franking credit “utilisation factor” . Section 3.1 prese ...

Institutional Factors and Real Estate Returns

... From Table 2, except for the first regression, the small values of variance inflation factors (VIF) of all the explaining variables indicate that there is little multicollinearity problem. We can see that controlling return volatility, both the economic freedom variable and the economic efficiency v ...

... From Table 2, except for the first regression, the small values of variance inflation factors (VIF) of all the explaining variables indicate that there is little multicollinearity problem. We can see that controlling return volatility, both the economic freedom variable and the economic efficiency v ...

Beta (finance)

In finance, the beta (β) of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not go up or down a lot, so it has a low beta. An example of the second is gold. The price of gold does go up and down a lot, but not in the same direction or at the same time as the market.A beta greater than one generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like equity put options can have large negative betas.Beta is important because it measures the risk of an investment that cannot be reduced by diversification. It does not measure the risk of an investment held on a stand-alone basis, but the amount of risk the investment adds to an already-diversified portfolio. In the capital asset pricing model, beta risk is the only kind of risk for which investors should receive an expected return higher than the risk-free rate of interest.The definition above covers only theoretical beta. The term is used in many related ways in finance. For example, the betas commonly quoted in mutual fund analyses generally measure the risk of the fund arising from exposure to a benchmark for the fund, rather than from exposure to the entire market portfolio. Thus they measure the amount of risk the fund adds to a diversified portfolio of funds of the same type, rather than to a portfolio diversified among all fund types.Beta decay refers to the tendency for a company with a high beta coefficient (β > 1) to have its beta coefficient decline to the market beta. It is an example of regression toward the mean.