Statement of Additional Information

... Rights of Each Share Class Each share of common stock of a Fund is entitled to one vote in electing Directors and other matters that may be submitted to shareholders for a vote. All shares of all Classes of each Fund generally have equal voting rights. However, matters affecting only one particular ...

... Rights of Each Share Class Each share of common stock of a Fund is entitled to one vote in electing Directors and other matters that may be submitted to shareholders for a vote. All shares of all Classes of each Fund generally have equal voting rights. However, matters affecting only one particular ...

Time-varying expected momentum profits

... of the value premium. Our paper is not the first to examine the procyclicality of momentum profits. Chordia and Shivakumar (2002), Cooper et al. (2004) and Stivers and Sun (2010) already documented procyclical variations in momentum profits. Unlike the previous literature, however, this paper shows tha ...

... of the value premium. Our paper is not the first to examine the procyclicality of momentum profits. Chordia and Shivakumar (2002), Cooper et al. (2004) and Stivers and Sun (2010) already documented procyclical variations in momentum profits. Unlike the previous literature, however, this paper shows tha ...

Cash-flow Risk, Discount Risk, and the Value Premium

... generate the value premium? Yes. Assets with high cash-flow risk and low duration have low price-dividend ratios. This is due to both the fact that they are risky, and thus prices have to be low to compensate agents for the risk they take, and because they have low expected dividend growth. Thus, po ...

... generate the value premium? Yes. Assets with high cash-flow risk and low duration have low price-dividend ratios. This is due to both the fact that they are risky, and thus prices have to be low to compensate agents for the risk they take, and because they have low expected dividend growth. Thus, po ...

An Empirical Assessment of Models of the Value Premium*

... Cooper (2006) makes the same link between profitability and B/M. If a firm has been hit by adverse profitability shocks, this firm’s B/M ratio is high because its market value falls while its book value remains fairly constant due to irreversibility. Such a firm is sensitive to aggregate shocks, an ...

... Cooper (2006) makes the same link between profitability and B/M. If a firm has been hit by adverse profitability shocks, this firm’s B/M ratio is high because its market value falls while its book value remains fairly constant due to irreversibility. Such a firm is sensitive to aggregate shocks, an ...

Investment Analysis and Portfolio Management

... expect r3 to be less than 4.5 percent, the expected interest rate on Investment 4 if it had low liquidity. Thus 2.5 percent < r3 < 4.5 percent. ...

... expect r3 to be less than 4.5 percent, the expected interest rate on Investment 4 if it had low liquidity. Thus 2.5 percent < r3 < 4.5 percent. ...

Client Investing Guide

... Our BPS may not be the most efficient service for such portfolios due to their reduced level of assets. However, Brooks Macdonald’s Multi Asset team manages four collective investment funds, which are sub funds of the IFSL Brooks Macdonald Fund provided by Investment Fund Services Limited, each matc ...

... Our BPS may not be the most efficient service for such portfolios due to their reduced level of assets. However, Brooks Macdonald’s Multi Asset team manages four collective investment funds, which are sub funds of the IFSL Brooks Macdonald Fund provided by Investment Fund Services Limited, each matc ...

Thesis - Kyiv School of Economics

... most of the cases. The capital flows were divided into three broad categories: government bonds, corporate bonds and corporate equities. For all of the capital categories market interest rate volatility as well as inflation volatility are significant and enter regressions with negative sign. This is ...

... most of the cases. The capital flows were divided into three broad categories: government bonds, corporate bonds and corporate equities. For all of the capital categories market interest rate volatility as well as inflation volatility are significant and enter regressions with negative sign. This is ...

Pairs Trading in the UK Equity Market Risk and Return

... are the returns from following such strategies in the UK? Is there a difference in performance and if so, can it be explained by the different characteristics of the two markets? In this paper we attempt to address these questions by examining the returns and risk of one type of hedge fund strategy ...

... are the returns from following such strategies in the UK? Is there a difference in performance and if so, can it be explained by the different characteristics of the two markets? In this paper we attempt to address these questions by examining the returns and risk of one type of hedge fund strategy ...

Does Financial Distress Risk Drive the Momentum Anomaly?

... years prior to bankruptcy, and particularly during the last year. This suggests that the market is anticipating, but not fully incorporating (i.e., under reacting to), the deteriorating financial health of a firm. Distressed firms, therefore, experience lower past realized returns. Hong et al. (2000 ...

... years prior to bankruptcy, and particularly during the last year. This suggests that the market is anticipating, but not fully incorporating (i.e., under reacting to), the deteriorating financial health of a firm. Distressed firms, therefore, experience lower past realized returns. Hong et al. (2000 ...

Webcast Presentation—Artisan Partners Global Equity Team

... Past performance does not guarantee and is not a reliable indicator of future results. Investment returns and principal values will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than that shown. V ...

... Past performance does not guarantee and is not a reliable indicator of future results. Investment returns and principal values will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than that shown. V ...

Value-at-Risk and Expected Stock Returns

... perspective of explaining asset returns. The concept of measuring downside risk dates back to Markowitz (1952) and Roy (1952). Markowitz (1952) provides a quantitative framework for measuring portfolio risk and return. The study utilizes mean returns, variances, and covariances to develop an efficie ...

... perspective of explaining asset returns. The concept of measuring downside risk dates back to Markowitz (1952) and Roy (1952). Markowitz (1952) provides a quantitative framework for measuring portfolio risk and return. The study utilizes mean returns, variances, and covariances to develop an efficie ...

lincreasedl Correlation in Bear Markets

... we propose an alternative approach to estimating the conditional correlation strxicture. We condition the correlation measure in a manner consistent with portfolio value at risk (VAR). irhe advantage is that our correlaiion estimates for portfolio retums are CDnditionedl on portfolio retums falling ...

... we propose an alternative approach to estimating the conditional correlation strxicture. We condition the correlation measure in a manner consistent with portfolio value at risk (VAR). irhe advantage is that our correlaiion estimates for portfolio retums are CDnditionedl on portfolio retums falling ...

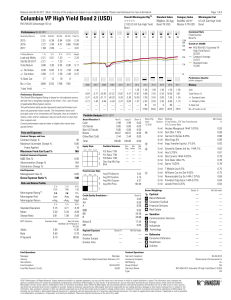

Columbia VP High Yield Bond 2 (USD)

... schedule of payments, a fixed investment account guaranteed by the insurance company or another form of guarantee depends on the claims paying ability of the issuing insurance company. Any such guarantee does not affect or apply to the investment return or principal value of the separate account and ...

... schedule of payments, a fixed investment account guaranteed by the insurance company or another form of guarantee depends on the claims paying ability of the issuing insurance company. Any such guarantee does not affect or apply to the investment return or principal value of the separate account and ...