Portfolio Risk Calculation and Stochastic Portfolio Optimization by A

... Since the portfolio return is a multivariate distribution of individual asset returns, the portfolio return distribution can be modeled by copulas. With this aim, we selected 15 stocks from New York Stock Exchange and constructed different portfolios. Then we modeled the distributions of individual ...

... Since the portfolio return is a multivariate distribution of individual asset returns, the portfolio return distribution can be modeled by copulas. With this aim, we selected 15 stocks from New York Stock Exchange and constructed different portfolios. Then we modeled the distributions of individual ...

Cross-Sectional Dispersion and Expected Returns

... dispersion, since they would offer their highest returns during periods of higher idiosyncratic (and undiversified) risk at the aggregate level. Consequently, investors would bid up the prices of these assets that act as hedges, and we would expect them to offer lower returns. At the other end of th ...

... dispersion, since they would offer their highest returns during periods of higher idiosyncratic (and undiversified) risk at the aggregate level. Consequently, investors would bid up the prices of these assets that act as hedges, and we would expect them to offer lower returns. At the other end of th ...

Does Academic Research Destroy Stock Return Predictability?*

... for forecasting variables, we are sure to find instances of ‘reliable’ return predictability that are in fact spurious.” To the extent that the results of the studies in our sample are caused by such biases, we should observe a decline in return-predictability out-of-sample. Rational Expectations v ...

... for forecasting variables, we are sure to find instances of ‘reliable’ return predictability that are in fact spurious.” To the extent that the results of the studies in our sample are caused by such biases, we should observe a decline in return-predictability out-of-sample. Rational Expectations v ...

The Level, Slope and Curve Factor Model for Stocks

... and high minus low (value). When using principal components to extract common factors from individual stocks, he finds no evidence of common variation due to differences in size and book to market (Connor and Korajczyk, 1986, 1988), but when using principal components analysis on a 10 by 10 portfol ...

... and high minus low (value). When using principal components to extract common factors from individual stocks, he finds no evidence of common variation due to differences in size and book to market (Connor and Korajczyk, 1986, 1988), but when using principal components analysis on a 10 by 10 portfol ...

Risk Aversion, Entrepreneurial Risk, and Portfolio Selection

... when private business equity is excluded from their entire portfolio, entrepreneurs are either more risk averse or exhibit no significant difference in their risk preference relative to other similar wealthy households. Their investment in other risky assets is either lower or similar to that of gen ...

... when private business equity is excluded from their entire portfolio, entrepreneurs are either more risk averse or exhibit no significant difference in their risk preference relative to other similar wealthy households. Their investment in other risky assets is either lower or similar to that of gen ...

Testing CAPM

... – Stambaugh (1982): similar results if add to stock index bonds and real estate: unable to reject zero-beta CAPM – Shanken (1987): if correlation between stock index and true global index exceeds 0.7-0.8, CAPM is rejected ...

... – Stambaugh (1982): similar results if add to stock index bonds and real estate: unable to reject zero-beta CAPM – Shanken (1987): if correlation between stock index and true global index exceeds 0.7-0.8, CAPM is rejected ...

The Risky Capital of Emerging Markets – A Long-Run

... a breach of a no arbitrage condition in international capital markets? The answer to this question is affirmative only in the absence of investment risk. In the presence of uncertainty, international investors may face different levels of risk from investing in different locations. We put forward ne ...

... a breach of a no arbitrage condition in international capital markets? The answer to this question is affirmative only in the absence of investment risk. In the presence of uncertainty, international investors may face different levels of risk from investing in different locations. We put forward ne ...

Who are the Value and Growth Investors?

... of the value premium, however, has proven to be challenging on traditional data sets that do not provide individual trades and therefore do not permit to assess the determinants of investor decisions. In this paper, we propose to use the rich information in investor portfolios to shed light on theor ...

... of the value premium, however, has proven to be challenging on traditional data sets that do not provide individual trades and therefore do not permit to assess the determinants of investor decisions. In this paper, we propose to use the rich information in investor portfolios to shed light on theor ...

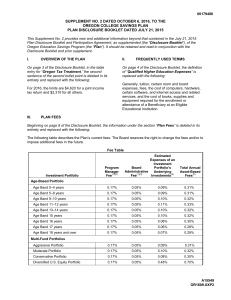

Vanguard Personal Advisor Services Brochure

... agreed-upon maximum limit (the “Upper Threshold”). When the Upper Threshold is exceeded, your Spending Fund balance will be reduced to the agreed-upon target amount (the “Target Balance”) and the additional assets will be invested according to the terms of your current Financial Plan, unless and unt ...

... agreed-upon maximum limit (the “Upper Threshold”). When the Upper Threshold is exceeded, your Spending Fund balance will be reduced to the agreed-upon target amount (the “Target Balance”) and the additional assets will be invested according to the terms of your current Financial Plan, unless and unt ...

Ashmore Emerging Markets Liquid Investment Portfolio Ashmore

... Coast and Poland were the top contributors to performance over the period. In China, the currency performed well, reverting to a trend of appreciation following intervention by the People's Bank of China (PBoC). The economy responded positively to targeted monetary easing as the Q2 2014 GDP accelera ...

... Coast and Poland were the top contributors to performance over the period. In China, the currency performed well, reverting to a trend of appreciation following intervention by the People's Bank of China (PBoC). The economy responded positively to targeted monetary easing as the Q2 2014 GDP accelera ...

Forward Looking Statements Non-GAAP

... income presents a useful view of the performance of our insurance operations, but should be considered in conjunction with net income computed in accordance with GAAP. A reconciliation of these measures to GAAP measures is available in our regular reports on Forms 10-Q and 10-K and in our latest qua ...

... income presents a useful view of the performance of our insurance operations, but should be considered in conjunction with net income computed in accordance with GAAP. A reconciliation of these measures to GAAP measures is available in our regular reports on Forms 10-Q and 10-K and in our latest qua ...

The Impact of Risk Controls and Strategy-Specific Risk Diversification on Extreme Risk

... The Impact of Risk Controls and Strategy-Specific Risk Diversification on Extreme Risk — August 2014 ...

... The Impact of Risk Controls and Strategy-Specific Risk Diversification on Extreme Risk — August 2014 ...