Chapter 8

... The return on a portfolio is the average return of the stocks in it, weighted by the dollars invested in each stock. The portfolio's return has a probability distribution with a mean and variance. These are the portfolio's expected return and risk. The expected return is the weighted average of the ...

... The return on a portfolio is the average return of the stocks in it, weighted by the dollars invested in each stock. The portfolio's return has a probability distribution with a mean and variance. These are the portfolio's expected return and risk. The expected return is the weighted average of the ...

Incorporating Strategy Risk of Active Managers into Portfolio Risk and Optimization

... to active managers who make formal alpha forecasts for each investment period. It cannot be used by more fundamental managers, nor by “outsiders” such as pension funds who employ the managers. The second is that the property of breadth is notoriously difficult to actually measure, as it represents a ...

... to active managers who make formal alpha forecasts for each investment period. It cannot be used by more fundamental managers, nor by “outsiders” such as pension funds who employ the managers. The second is that the property of breadth is notoriously difficult to actually measure, as it represents a ...

C01_Reilly1ce

... Risk and Expected Return • Risk refers to the uncertainty of the future outcomes of an investment – There are many possible returns/outcomes from an investment due to the uncertainty – Probability is the likelihood of an outcome – The sum of the probabilities of all the possible outcomes is equal t ...

... Risk and Expected Return • Risk refers to the uncertainty of the future outcomes of an investment – There are many possible returns/outcomes from an investment due to the uncertainty – Probability is the likelihood of an outcome – The sum of the probabilities of all the possible outcomes is equal t ...

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

... steeper as you move to the right along the horizontal axis show good timing ability. The steeper slope shows that the manager maintained higher portfolio sensitivity to market swings (i.e., a higher beta) in periods when the market performed well. This ability to choose more market-sensitive securit ...

... steeper as you move to the right along the horizontal axis show good timing ability. The steeper slope shows that the manager maintained higher portfolio sensitivity to market swings (i.e., a higher beta) in periods when the market performed well. This ability to choose more market-sensitive securit ...

Solutions to Chapter 11

... expect to see more 40-point days in 2010 even if market risk as measured by percentage returns is no higher than it was in 1990. Est time: 01–05 ...

... expect to see more 40-point days in 2010 even if market risk as measured by percentage returns is no higher than it was in 1990. Est time: 01–05 ...

A Portfolio Approach to the Optimal Funding of Pensions

... in less risky, lower return assets. While there may be other factors such as political independence of the investment board that are important, the level of risk in alternative available assets is also a crucial consideration. In the absence of another low risk alternative, individuals and pension f ...

... in less risky, lower return assets. While there may be other factors such as political independence of the investment board that are important, the level of risk in alternative available assets is also a crucial consideration. In the absence of another low risk alternative, individuals and pension f ...

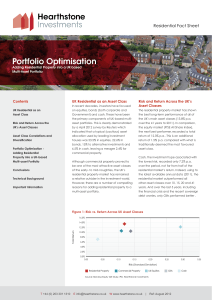

Investment risks - Lecture 10: Asset allocation methods

... 1. The optimal allocation is determined in two steps. First, we decide the allocation between the risky portfolio, and the riskless asset. Second, we determine the allocation between the assets that comprise the risky portfolio. 2. As every portfolio of the risky assets and the riskless asset has th ...

... 1. The optimal allocation is determined in two steps. First, we decide the allocation between the risky portfolio, and the riskless asset. Second, we determine the allocation between the assets that comprise the risky portfolio. 2. As every portfolio of the risky assets and the riskless asset has th ...

Alpha Dynamics_Evaluating the Activeness of Equity Portfolios.indd

... At Principal Global Investors, we have long recognized that tracking error and stock counts are not adequate to fully assess the activeness of a portfolio. Notably, we are often asked how we have been able to generate high levels of excess returns with a high degree of consistency, while maintaining ...

... At Principal Global Investors, we have long recognized that tracking error and stock counts are not adequate to fully assess the activeness of a portfolio. Notably, we are often asked how we have been able to generate high levels of excess returns with a high degree of consistency, while maintaining ...

Returns, Absolute Returns and Risk

... steadier for the hedge funds than for the market and higher overall. But does the fact that losses were minimized or avoided in the down years mean that hedge funds provide absolute returns? That depends on your criteria for “absolute.” If “insensitive to market movements” or “free of external refer ...

... steadier for the hedge funds than for the market and higher overall. But does the fact that losses were minimized or avoided in the down years mean that hedge funds provide absolute returns? That depends on your criteria for “absolute.” If “insensitive to market movements” or “free of external refer ...

PSF Conservative Balanced Portfolio

... stocks owned and the horizontal axis shows investment style (value, blend, or growth). A darkened square in the style box indicates the weighted average style of the portfolio. For fixed-income funds, the vertical axis shows the credit quality of the long bonds owned and the horizontal axis shows in ...

... stocks owned and the horizontal axis shows investment style (value, blend, or growth). A darkened square in the style box indicates the weighted average style of the portfolio. For fixed-income funds, the vertical axis shows the credit quality of the long bonds owned and the horizontal axis shows in ...