Inflation and the Price of Real Assets ∗ Monika Piazzesi Martin Schneider

... that reduced the propensity to save in the household sector. First, entry of the young baby boomers into asset markets directly lowered the average savings rate. Second, the erosion of bond portfolios by surprise inflation reduced the ratio of financial wealth to human wealth, which also gives rise ...

... that reduced the propensity to save in the household sector. First, entry of the young baby boomers into asset markets directly lowered the average savings rate. Second, the erosion of bond portfolios by surprise inflation reduced the ratio of financial wealth to human wealth, which also gives rise ...

Measuring and Modeling Execution Cost and Risk

... costs that can accommodate such parent orders. Implementation shortfall compares the value of a paper portfolio with no transaction costs to the real portfolio obtained by actual trading. This measure of execution cost has been used in empirical work by Keim and Madhavan (1997), Bertsimas and Lo (19 ...

... costs that can accommodate such parent orders. Implementation shortfall compares the value of a paper portfolio with no transaction costs to the real portfolio obtained by actual trading. This measure of execution cost has been used in empirical work by Keim and Madhavan (1997), Bertsimas and Lo (19 ...

lecture_20_hedging_and_black-scholes

... • In finance, delta neutral describes a portfolio of related financial securities, in which the portfolio value remains unchanged when small changes occur in the value of the underlying security. • Such a portfolio typically contains options and their corresponding underlying securities such that po ...

... • In finance, delta neutral describes a portfolio of related financial securities, in which the portfolio value remains unchanged when small changes occur in the value of the underlying security. • Such a portfolio typically contains options and their corresponding underlying securities such that po ...

Learning to Identify Winning Stocks

... firms by F-score and take the firms in the highest decile to form our portfolio. Based on the prices of these firms in Using the data set described in Section 2, we can recre- the current year and the subsequent year, we calculate the ate the F-score strategy as follows. Using only the last return o ...

... firms by F-score and take the firms in the highest decile to form our portfolio. Based on the prices of these firms in Using the data set described in Section 2, we can recre- the current year and the subsequent year, we calculate the ate the F-score strategy as follows. Using only the last return o ...

Working Paper No. 510 Institutional investor

... The aim of this paper is to address this gap in the literature. We examine the behaviour of institutional investors, ie insurance companies (life companies in particular) and pension funds, both before and during the global financial crisis using both aggregate and micro-level data, in order to inve ...

... The aim of this paper is to address this gap in the literature. We examine the behaviour of institutional investors, ie insurance companies (life companies in particular) and pension funds, both before and during the global financial crisis using both aggregate and micro-level data, in order to inve ...

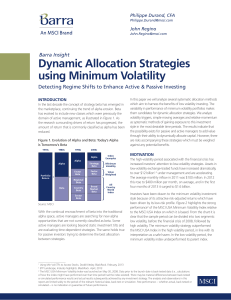

Dynamic Allocation Strategies using Minimum Volatility

... • Without limi ng any of the foregoing and to the maximum extent permi ed by applicable law, in no event shall any Informa on Provider have any liability regarding any of the Informa on for any direct, indirect, special, puni ve, consequen al (including lost profits) or any other damages even if no ...

... • Without limi ng any of the foregoing and to the maximum extent permi ed by applicable law, in no event shall any Informa on Provider have any liability regarding any of the Informa on for any direct, indirect, special, puni ve, consequen al (including lost profits) or any other damages even if no ...

the evaluation of active manager returns in a non

... positive active returns, on average, satisfy the first prerequisite for satisfactory performance. However the way that this satisfactory performance has been provides is also important to investors and this is captured by the next three moments of the active return distribution. Standard Deviation ...

... positive active returns, on average, satisfy the first prerequisite for satisfactory performance. However the way that this satisfactory performance has been provides is also important to investors and this is captured by the next three moments of the active return distribution. Standard Deviation ...

View Full Article - State Street Global Advisors

... the portfolio while delivering positive momentum and a small cap bias (which highly rated ESG companies do not naturally have exposure to). Using an optimizer can efficiently balance the desired ESG and factor exposures. To show how this can be done, we can create a model portfolio for illustrative ...

... the portfolio while delivering positive momentum and a small cap bias (which highly rated ESG companies do not naturally have exposure to). Using an optimizer can efficiently balance the desired ESG and factor exposures. To show how this can be done, we can create a model portfolio for illustrative ...

Fear of the Unknown: Familiarity and Economic Decisions

... (sales) under a probability distribution that is adverse to buying (selling) (i.e., one in which the expected utility from the good or security is low (high)). This gives rise to the difference between the willingness to pay and the willingness to accept (e.g., Thaler, 1980). In a capital budgeting ...

... (sales) under a probability distribution that is adverse to buying (selling) (i.e., one in which the expected utility from the good or security is low (high)). This gives rise to the difference between the willingness to pay and the willingness to accept (e.g., Thaler, 1980). In a capital budgeting ...

Asset Pricing with Idiosyncratic Risk and Overlapping Generations

... Our model features non-degenerate trade in financial assets. Thus, we can say something about what kinds of portfolio rules support the imperfect aggregate risk sharing allocations described above. A useful benchmark is Bodie, Merton, and Samuelson (1992) (BMS). In their model wages are riskless an ...

... Our model features non-degenerate trade in financial assets. Thus, we can say something about what kinds of portfolio rules support the imperfect aggregate risk sharing allocations described above. A useful benchmark is Bodie, Merton, and Samuelson (1992) (BMS). In their model wages are riskless an ...

Financial Market Volatility Final Project

... were used since MLLIB did not have python bindings yet for cross-validated splitting of dataset. • Spark was ran on data held in HDFS. • Results obtained were tested on a hold out sample and R^2 calculated to show how much variance could be explained by the regressor. ...

... were used since MLLIB did not have python bindings yet for cross-validated splitting of dataset. • Spark was ran on data held in HDFS. • Results obtained were tested on a hold out sample and R^2 calculated to show how much variance could be explained by the regressor. ...

How different is the regulatory capital from the economic capital

... The aim of this study is to evaluate the ability of the regulatory capital requirements formula to hedge the portfolio credit risk. To this aim, we compare the level of capital requirements computed by using regulatory Basel 2 formula to the level of capital computed by using a model of portfolio c ...

... The aim of this study is to evaluate the ability of the regulatory capital requirements formula to hedge the portfolio credit risk. To this aim, we compare the level of capital requirements computed by using regulatory Basel 2 formula to the level of capital computed by using a model of portfolio c ...

The Risk-free Rate and the Market Risk Premium

... In the interests of transparency and to promote informed discussion, the Authority would prefer submissions to be made publicly available wherever this is reasonable. However, if a person making a submission does not want that submission to be public, that person should claim confidentiality in resp ...

... In the interests of transparency and to promote informed discussion, the Authority would prefer submissions to be made publicly available wherever this is reasonable. However, if a person making a submission does not want that submission to be public, that person should claim confidentiality in resp ...

Asset - Ludhiana

... The terms above comply with Para 19 of IAS 39- conditions for treating a transaction as “ transfer” . The conditions prima facie suggest that the risks and rewards are substantially transferred ...

... The terms above comply with Para 19 of IAS 39- conditions for treating a transaction as “ transfer” . The conditions prima facie suggest that the risks and rewards are substantially transferred ...

Markov process

... This expression reminds us of the Black Scholes formula! Indeed, GBM is central to Black Scholes pricing. GBM assumes stock returns are normally distributed. But empirical data reveals that large movements in stock price are more likely than a normally distributed stock price model suggests. ...

... This expression reminds us of the Black Scholes formula! Indeed, GBM is central to Black Scholes pricing. GBM assumes stock returns are normally distributed. But empirical data reveals that large movements in stock price are more likely than a normally distributed stock price model suggests. ...

Bond Landdering - Wealthcare Securities Pvt. Ltd.

... BOND LADDERING However… The face value of each bond might be same. For example, a bond portfolio of Rs10 lakh may have 10 different bonds of Rs1 lakh each maturing after one year, two years, three years and so on. In such a situation, your bond portfolio would actually look like a ladder in w ...

... BOND LADDERING However… The face value of each bond might be same. For example, a bond portfolio of Rs10 lakh may have 10 different bonds of Rs1 lakh each maturing after one year, two years, three years and so on. In such a situation, your bond portfolio would actually look like a ladder in w ...