Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

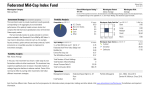

Morningstar U.S. Market Factor Tilt Index SM ® Learn More For more information about all of Morningstar’s indexes, visit http://indexes.morningstar.com or contact us: [email protected] 11 312 384-3735. Research shows that over long periods of time, portfolios of small-company stocks, as measured by market capitalization, tend to outperform portfolios of large-company stocks within the same equity markets, even after controlling for beta. corresponding market-capitalization-weighted index. Likewise, stocks designated as “large” or “growth” stocks have underweighting compared to a standard market-capitalization weighting. Similarly, research on the U.S. market reveals that in addition to a small-cap effect, there is also a value effect. In other words, over long periods of time, portfolios of stocks with relatively favorable valuation ratios (low price/book, low price/earnings, high dividend yields, etc.) tend to outperform portfolios of stocks with relatively unfavor-able valuation ratios, even after controlling for beta. Stocks with favorable ratios became known as “value” stocks and those with unfavorable ratios became known as “growth” stocks. Methodology The Index construction follows a four-step process: The Morningstar U.S. Market Factor Tilt Index is designed to take advantage of these market anomalies—the small-cap and value-oriented stocks tend to outperform over the long term. The U.S. Market Factor Tilt Index seeks to capture both value and size premium to achieve what the efficient-markets camp refers to as systematic exposure to undiversifiable risk. The Morningstar U.S. Market Factor Tilt Index The Morningstar U.S. Market Factor Tilt Index measures the performance of U.S. equity markets with increased exposure to small/micro-capitalization and value stocks. Stocks that are deemed to be small-capitalization or small-value have an overweighting in the index compared to their weight in a Step 1: Defining Investable Universe. To qualify for inclusion in the investable universe, a security must be U.S. domiciled, trade on one of the three major exchanges (the NYSE, NASDAQ, or NYSE AMEX) and must not have 10 nontrading days in the prior quarter. Step 2: Defining Total U.S. Market Portfolio. The largest 99.50% of the liquid securities by market capitalization qualify for inclusion in the Total U.S. Market Portfolio. The Total Market Portfolio is then broken down into four cap indexes using the following guidelines: 3 The Large-Cap Index is constructed by selecting the largest stocks that comprise 70% of the market capitalization in the investable universe. 3 The Mid-Cap Index represents the next-largest stocks that comprise 20% of the market capitalization in the investable universe. 3 The Small-Cap Index represents the next-largest stocks that comprise 7% of the market capitalization in the investable universe. Morningstar U.S. Market Factor Tilt Index Construction Process Lrg Morningstar Investable Universe Morningstar Total U.S. Market Portfolio Assign Value Scores/Stock Style Apply Factor Tilt Mid Sml Micro Val All U.S. domiciled companies listed on NYSE, NASDAQ & NYSE AMEX The largest 99.5% of liquid securities, by market cap Categorized by market cap: Micro, Small, Mid, Large and Style: Value, Core, Growth ©2011 Morningstar, Inc. All rights reserved. Morningstar and the Morningstar logo are either trademarks or service marks of Morningstar, Inc. 02-09-11 Tilt portfolios toward Small/ Micro-Cap, Value Cor Gro Morningstar ® U.S. Market Factor Tilt Index SM Growth of a $10,000 Investment (01 Jul 1997–31 Aug 2011) 28,000 24,000 Morningstar U.S. Factor Tilt Index 22,000 20,000 18,000 S&P 500 16,000 14,000 12,000 10,000 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Index Comparisons (01 Jul 1997–31 Aug 2011) Annualized Return % Standard Deviation % Sharpe Ratio % Max Draw Morningstar U.S. Market Factor Tilt 5.31 17.86 0.22 -52.46 S&P 500 3.55 16.52 0.12 -50.95 Index Data from July 01, 1997–September 30, 2011. 3 The Micro-Cap Index represents the next-largest stocks that comprise 2.50% of the market capitalization in the investable universe. Step 3: Assigning Value Scores and Stock Style. A stock’s value orientation reflects the price investors are willing to pay for a share of some combination of the stock’s prospective earnings, dividends, sales, cash flow, and book value. Value orientation is determined using the following steps: 3 Calculate five prospective yields (earnings, dividend, cash flow, revenue and book value) for each stock within each of the cap indexes. 3 Compute a cumulative value score for each security relative to other stocks in the cap band. 3 Index constituents are assigned so that within each of the large-cap, mid-cap, small-cap and micro-cap size bands, the three indexes that reflect each of the three levels of value orientation account for roughly a third of the total floatadjusted of the size band. ©2011 Morningstar, Inc. All rights reserved. Morningstar and the Morningstar logo are either trademarks or service marks of Morningstar, Inc. 02-09-11 Step 4: Applying Factor Tilt. We developed a model that allows us to set separately degrees of value tilting and size tilting, each on a scale from 0 (no tilt) to 1 (full tilt). To select which combination of settings for thee tilting parameters, we first create 25 portfolios by using values of 0.1, 0.2, 0.3, 0.4, 0.5 for each of two parameters. We then used the threefactor Fama French (FF) model to guide us toward one of these 25 portfolios to use. (See Fama and Franch 1993, 1995, 1996.) (The three factors of the FF model are the excess return on the market portfolio; SMB, which is the difference between the returns of a small-cap and a large-cap portfolio; and HML, which is the difference in returns between a high book/market and low book/market portfolio.) Setting the size tilt factor to 0.4 and value tilt factor to 0.1 results in FF regression coefficients over the 14 plus year history of SMB and HML of 0.18 and 0.23, respectively. Since these coefficients are close to our target sensitivities to the FF factors, we selected this portfolio. At each reconstitution, the Morningstar Index Committee will review the long-term sensitivities of the candidate portfolios to value and size factors, using at least in part the FF model to ensure the tilt factors continue to be appropriate. Constituent Weight Calculation Each index constituent is weighted according to its modified free float value, which is the product of free float shares, the most recently traded price of the security and a weight adjustment factor. While the modified free float value is calculated continually for each index constituent, the free float shares of each potential Total U.S. Market constituent is only calculated at each rebalancing. Adjustment factors for each constituent are calculated at each reconstitution. Rebalancing and Reconstitution The Morningstar U.S. Market Factor Tilt Index is rebalanced —i.e. the security weights (the product of the number of free float shares and the indicated dividend per share of each constituent) are adjusted—four times annually. The index is reconstituted—i.e., the index membership is reset— twice annually.