Demand Ch. 4 Study Guide

... The demand of a specific good or service by one person 18. Law of diminishing marginal utility: you receive the most satisfaction from the first good or service than the second, third, etc. 19. Consumer expectation: future expectations can influence today’s buying habits 20. Why do tickets for local ...

... The demand of a specific good or service by one person 18. Law of diminishing marginal utility: you receive the most satisfaction from the first good or service than the second, third, etc. 19. Consumer expectation: future expectations can influence today’s buying habits 20. Why do tickets for local ...

yellow dollar amount

... A patent gives inventors the exclusive right to produce and market a product for a period of time. It has a patent for a unique antispyware program called Aspy. The companies patent on Aspy has expired. What will happen to the companies profits in the long run? ...

... A patent gives inventors the exclusive right to produce and market a product for a period of time. It has a patent for a unique antispyware program called Aspy. The companies patent on Aspy has expired. What will happen to the companies profits in the long run? ...

Intermediate Microeconomics

... Specifically, since monopolist chooses market supply, it essentially picks a point on the market demand curve to operate on. This means that for a monopolist, equilibrium price is a function of the quantity they supply, so they effectively get to choose both i.e. choose where to operate on p(q) (“ ...

... Specifically, since monopolist chooses market supply, it essentially picks a point on the market demand curve to operate on. This means that for a monopolist, equilibrium price is a function of the quantity they supply, so they effectively get to choose both i.e. choose where to operate on p(q) (“ ...

Chapter 7

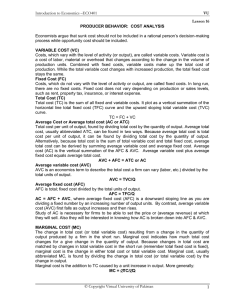

... B. Basic conclusion to be explained is that after long-run equilibrium is achieved, the product price will be exactly equal to, and production will occur at, each firm’s point of minimum average total cost. 1. Firms seek profits and shun losses. 2. Under competition, firms may enter and leave indust ...

... B. Basic conclusion to be explained is that after long-run equilibrium is achieved, the product price will be exactly equal to, and production will occur at, each firm’s point of minimum average total cost. 1. Firms seek profits and shun losses. 2. Under competition, firms may enter and leave indust ...

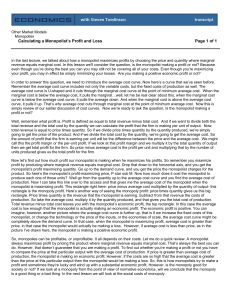

In the last lecture, we talked about how a monopolist maximizes

... In order to answer this question, we need to introduce the average cost curve. Now here’s a curve that we’ve seen before. Remember the average cost curve includes not only the variable costs, but the fixed costs of production as well. The average cost curve is U-shaped and it cuts through the margin ...

... In order to answer this question, we need to introduce the average cost curve. Now here’s a curve that we’ve seen before. Remember the average cost curve includes not only the variable costs, but the fixed costs of production as well. The average cost curve is U-shaped and it cuts through the margin ...

supply - Duluth High School

... Increasing returns B. Diminishing returns C. Equaling returns D. Negative returns The period of production that allows producers to change only the amount of the variable input called labor is: A. The long run B. The short run C. The production function D. A stage of production A production function ...

... Increasing returns B. Diminishing returns C. Equaling returns D. Negative returns The period of production that allows producers to change only the amount of the variable input called labor is: A. The long run B. The short run C. The production function D. A stage of production A production function ...

demand notes class

... At $1.00 per candy bar, about 16 Twix are If the price of Twix increases to $1.50 per demanded by students in this class. candy bar, the quantity demanded will DECREASE to ????? ...

... At $1.00 per candy bar, about 16 Twix are If the price of Twix increases to $1.50 per demanded by students in this class. candy bar, the quantity demanded will DECREASE to ????? ...

J Newhouse - Moral hazard-risk aversion tradeoff 0606

... paribus, firms with longer job tenure will provide insurance with less cost sharing if those services reduce future costs ...

... paribus, firms with longer job tenure will provide insurance with less cost sharing if those services reduce future costs ...

Demand Notes

... At $1.00 per candy bar, about 16 Twix are If the price of Twix increases to $1.50 per demanded by students in this class. candy bar, the quantity demanded will DECREASE to ????? ...

... At $1.00 per candy bar, about 16 Twix are If the price of Twix increases to $1.50 per demanded by students in this class. candy bar, the quantity demanded will DECREASE to ????? ...

Externality

In economics, an externality is the cost or benefit that affects a party who did not choose to incur that cost or benefit.For example, manufacturing activities that cause air pollution impose health and clean-up costs on the whole society, whereas the neighbors of an individual who chooses to fire-proof his home may benefit from a reduced risk of a fire spreading to their own houses. If external costs exist, such as pollution, the producer may choose to produce more of the product than would be produced if the producer were required to pay all associated environmental costs. Because responsibility or consequence for self-directed action lies partly outside the self, an element of externalization is involved. If there are external benefits, such as in public safety, less of the good may be produced than would be the case if the producer were to receive payment for the external benefits to others. For the purpose of these statements, overall cost and benefit to society is defined as the sum of the imputed monetary value of benefits and costs to all parties involved. Thus, unregulated markets in goods or services with significant externalities generate prices that do not reflect the full social cost or benefit of their transactions; such markets are therefore inefficient.