Micro Extra Credit Free Response 1. Steverail, the only provider of

... (d) Suppose that when the price of toy cars increases by 10 percent, Theresa buys 5 percent fewer toy cars and 4 percent less of a different toy, blocks. Calculate the cross-price elasticity for toy cars and blocks and indicate if it is positive or negative. ...

... (d) Suppose that when the price of toy cars increases by 10 percent, Theresa buys 5 percent fewer toy cars and 4 percent less of a different toy, blocks. Calculate the cross-price elasticity for toy cars and blocks and indicate if it is positive or negative. ...

LECT5F03

... The LAW OF DEMAND – THE HIGHER THE PRICE THE LOWER WILL BE THE QUANTITY DEMANDED. ...

... The LAW OF DEMAND – THE HIGHER THE PRICE THE LOWER WILL BE THE QUANTITY DEMANDED. ...

Answer Monopoly, Regulated Monopoly

... Regulation is necessary because unregulated monopolies produce too little and cause a deadweight loss by using too few resources in this industry compared to others. Regulation of utilities, however, if forcing them to earn only a risk-adjusted normal rate of return on invested capital, results (in ...

... Regulation is necessary because unregulated monopolies produce too little and cause a deadweight loss by using too few resources in this industry compared to others. Regulation of utilities, however, if forcing them to earn only a risk-adjusted normal rate of return on invested capital, results (in ...

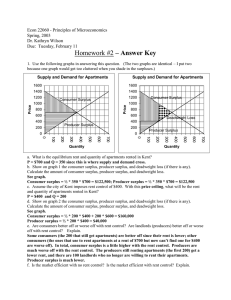

Homework #2

... a. Calculate the equilibrium price and quantity without the price floor, and plot the demand and supply curves in a graph. In your graph mark the initial equilibrium price and quantity. On your graph identify the y-intercept and x-intercept for the demand curve and the y-intercept for the supply cur ...

... a. Calculate the equilibrium price and quantity without the price floor, and plot the demand and supply curves in a graph. In your graph mark the initial equilibrium price and quantity. On your graph identify the y-intercept and x-intercept for the demand curve and the y-intercept for the supply cur ...

Document

... • Demand curves can show the demand for an individual, or for a “market” of any defined size (classroom, CPHS, Pleasant Hill, etc.) ...

... • Demand curves can show the demand for an individual, or for a “market” of any defined size (classroom, CPHS, Pleasant Hill, etc.) ...

MONOPOLY

... • A monopoly firm is the sole seller in its market. Monopolies arise due to barriers to entry, including: government-granted monopolies, the control of a key resource, or economies of scale over the entire range of output. • A monopoly firm faces a downward-sloping demand curve for its product. As a ...

... • A monopoly firm is the sole seller in its market. Monopolies arise due to barriers to entry, including: government-granted monopolies, the control of a key resource, or economies of scale over the entire range of output. • A monopoly firm faces a downward-sloping demand curve for its product. As a ...

Problem Set #4 - MIT OpenCourseWare

... firms in the industry are actually producing while other potential firms are sitting on the sidelines perhaps producing other goods. Explain why there is not enough information in the problem to determine whether all potential farms are producing cloves or not. ANS: The missing information is how re ...

... firms in the industry are actually producing while other potential firms are sitting on the sidelines perhaps producing other goods. Explain why there is not enough information in the problem to determine whether all potential farms are producing cloves or not. ANS: The missing information is how re ...

Q 1 - The Ohio State University

... Profit-Maximization for Competitive Firm • So in the long run equilibrium in competitive industries, firm produce at the minimum point of both the short-run and long-run ATC curve. ...

... Profit-Maximization for Competitive Firm • So in the long run equilibrium in competitive industries, firm produce at the minimum point of both the short-run and long-run ATC curve. ...

File

... 1. Does a price ceiling create a shortage or surplus? 2. What is one thing that causes a change in quantity demanded? 3. What is the law of supply? 4. What is the law of demand? 5. Price ceilings are an example of a true free market economy. True or False 6. Price floors are designed to keep prices: ...

... 1. Does a price ceiling create a shortage or surplus? 2. What is one thing that causes a change in quantity demanded? 3. What is the law of supply? 4. What is the law of demand? 5. Price ceilings are an example of a true free market economy. True or False 6. Price floors are designed to keep prices: ...

Marginal Revenue

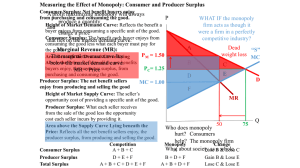

... Connecting the Pareto approach to efficiency with consumer and producer surplus Question: How did we argue that P monopoly was inefficient? We chose an individual, Joe, who Did not by a hamburger when the price was $1.50, the monopoly price. But would be a hamburger at a PM = 1.50 price of $1.40, a ...

... Connecting the Pareto approach to efficiency with consumer and producer surplus Question: How did we argue that P monopoly was inefficient? We chose an individual, Joe, who Did not by a hamburger when the price was $1.50, the monopoly price. But would be a hamburger at a PM = 1.50 price of $1.40, a ...

krugman_mods_3e_irm_micro_econ_mod26

... The cost curve graph is useful for helping students understand when firms make positive versus negative profit. There is sure to be some confusion at first regarding how to identify the profit-maximizing level of output on the graph and how to identify profit itself on the graph. Students will need ...

... The cost curve graph is useful for helping students understand when firms make positive versus negative profit. There is sure to be some confusion at first regarding how to identify the profit-maximizing level of output on the graph and how to identify profit itself on the graph. Students will need ...

Test 3 Microeconomics – ERAU --Machiorlatti

... indicating that it is perfect competition. This goes back to the idea that there are many sellers and if they did raise price they would lose all demand. ...

... indicating that it is perfect competition. This goes back to the idea that there are many sellers and if they did raise price they would lose all demand. ...

Shift in the Demand Curve

... A. The U.S. has a ____________Economy 1. most economic decisions made by individuals looking out for _________________________. a. ____________ gov’t interference 2. is ____________ a. the ____________ you make as a consumer affects the products made and prices you pay for them. b. vice-versa, the p ...

... A. The U.S. has a ____________Economy 1. most economic decisions made by individuals looking out for _________________________. a. ____________ gov’t interference 2. is ____________ a. the ____________ you make as a consumer affects the products made and prices you pay for them. b. vice-versa, the p ...

Externality

In economics, an externality is the cost or benefit that affects a party who did not choose to incur that cost or benefit.For example, manufacturing activities that cause air pollution impose health and clean-up costs on the whole society, whereas the neighbors of an individual who chooses to fire-proof his home may benefit from a reduced risk of a fire spreading to their own houses. If external costs exist, such as pollution, the producer may choose to produce more of the product than would be produced if the producer were required to pay all associated environmental costs. Because responsibility or consequence for self-directed action lies partly outside the self, an element of externalization is involved. If there are external benefits, such as in public safety, less of the good may be produced than would be the case if the producer were to receive payment for the external benefits to others. For the purpose of these statements, overall cost and benefit to society is defined as the sum of the imputed monetary value of benefits and costs to all parties involved. Thus, unregulated markets in goods or services with significant externalities generate prices that do not reflect the full social cost or benefit of their transactions; such markets are therefore inefficient.