Examples on Monopoly and Third Degree Price Discrimination

... each unit of the product. Although, the price to the second group is more than twice the price to the first it would be a mistake to conclude that the firm should increase sales to the second group. Why? The key indicators are the marginal revenues. In order to maximize profits, the firm equates the ...

... each unit of the product. Although, the price to the second group is more than twice the price to the first it would be a mistake to conclude that the firm should increase sales to the second group. Why? The key indicators are the marginal revenues. In order to maximize profits, the firm equates the ...

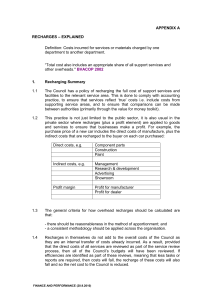

(Attachment: 20)Appendix A

... 1. As stated at 1.4, recharges do not add to the overall costs of the Council as they are an internal transfer of costs already incurred. However, this also means that, if a service or function stops and therefore provides savings, then the areas generating recharges should also review their servic ...

... 1. As stated at 1.4, recharges do not add to the overall costs of the Council as they are an internal transfer of costs already incurred. However, this also means that, if a service or function stops and therefore provides savings, then the areas generating recharges should also review their servic ...

m5l3decisionmakingexplicitandimplicitcostspc

... Market constraints are conditions under which a firm buys input and sells output. On the input side, limited supply of resources means higher prices for additional units. On the output side, limited demand for goods & services means lower prices for additional units. Technology constraints are limit ...

... Market constraints are conditions under which a firm buys input and sells output. On the input side, limited supply of resources means higher prices for additional units. On the output side, limited demand for goods & services means lower prices for additional units. Technology constraints are limit ...

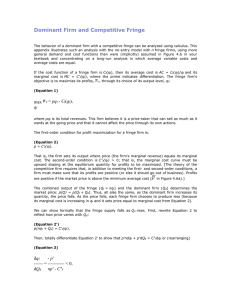

Monopoly

... the monopolist. At point E, MR=MC hence OQ =(BQ). BQ being more than long-run average cost CQ (AR>AC), the monopolist will get supernormal profit. The monopolist earns (BQ-CQ=BC) super normal profit per unit. His total super –normal profit will be BCDP as shown by shaded area. ...

... the monopolist. At point E, MR=MC hence OQ =(BQ). BQ being more than long-run average cost CQ (AR>AC), the monopolist will get supernormal profit. The monopolist earns (BQ-CQ=BC) super normal profit per unit. His total super –normal profit will be BCDP as shown by shaded area. ...

PART IV

... “The Economic Organization of a POW Camp,” Economica (November 1945). Students find the definition of Pareto optimality (an allocation is Pareto-efficient if goods cannot be reallocated to make someone better off without making someone else worse off) confusing because of its “double negative” expre ...

... “The Economic Organization of a POW Camp,” Economica (November 1945). Students find the definition of Pareto optimality (an allocation is Pareto-efficient if goods cannot be reallocated to make someone better off without making someone else worse off) confusing because of its “double negative” expre ...

Supply and Demand

... concept is demand elasticity. If quantities are being brought to market for sale, the concept is supply elasticity. ...

... concept is demand elasticity. If quantities are being brought to market for sale, the concept is supply elasticity. ...

Supply

... • Assessing the best level of output can be done by determining when marginal revenue is equal to marginal cost. • Marginal cost is the additional cost of producing one more unit. • Marginal revenue is the additional income from selling one more unit of a good; sometimes equal to price. • Simply, th ...

... • Assessing the best level of output can be done by determining when marginal revenue is equal to marginal cost. • Marginal cost is the additional cost of producing one more unit. • Marginal revenue is the additional income from selling one more unit of a good; sometimes equal to price. • Simply, th ...

Answer Key 4 - personal.kent.edu

... False. In order for profits for the industry to be maximized, all firms must cooperate. However, if any given firm sells more than the agreed to amount, it can increase its profit but at the cost of profits to other firms. See question 2. e. If there are many firms and a homogenous product then the ...

... False. In order for profits for the industry to be maximized, all firms must cooperate. However, if any given firm sells more than the agreed to amount, it can increase its profit but at the cost of profits to other firms. See question 2. e. If there are many firms and a homogenous product then the ...

Tutorial 1 - Problems

... b.) Suppose that a poor harvest season raises the price of apples to PA = 2. Find the new equilibrium price and quantity of apple juice. Draw a graph to illustrate your answer. c.) Suppose PA = 1 but the price of tea drops to PT = 3. Find the new equilibrium price and quantity of apple juice. d.) Su ...

... b.) Suppose that a poor harvest season raises the price of apples to PA = 2. Find the new equilibrium price and quantity of apple juice. Draw a graph to illustrate your answer. c.) Suppose PA = 1 but the price of tea drops to PT = 3. Find the new equilibrium price and quantity of apple juice. d.) Su ...

Study Questions

... g. An increase in market demand will lead to a larger price increase in the short run than in the long run. h. An increase in market demand will lead to a larger market output increase in the short run than in the long run. i. A 10% profit tax will have the same impact on firm output as an excise ta ...

... g. An increase in market demand will lead to a larger price increase in the short run than in the long run. h. An increase in market demand will lead to a larger market output increase in the short run than in the long run. i. A 10% profit tax will have the same impact on firm output as an excise ta ...

File

... o Inferior Good: a good for which demand decreases as income increases (e.g., used cars, bus tickets) o Substitutes: two or more goods that satisfy a similar need, so that one good can be used in place of another (e.g., Coke and Pepsi; Metro fares and taxi fares) o Complements: two or more goods tha ...

... o Inferior Good: a good for which demand decreases as income increases (e.g., used cars, bus tickets) o Substitutes: two or more goods that satisfy a similar need, so that one good can be used in place of another (e.g., Coke and Pepsi; Metro fares and taxi fares) o Complements: two or more goods tha ...

law of demand

... The Law of Supply • The law of supply holds that other things equal, as the price of a good rises, its quantity supplied will rise, and vice versa. • Why do producers produce more output when prices rise? – They seek higher profits – They can cover higher marginal costs of production ...

... The Law of Supply • The law of supply holds that other things equal, as the price of a good rises, its quantity supplied will rise, and vice versa. • Why do producers produce more output when prices rise? – They seek higher profits – They can cover higher marginal costs of production ...

Externality

In economics, an externality is the cost or benefit that affects a party who did not choose to incur that cost or benefit.For example, manufacturing activities that cause air pollution impose health and clean-up costs on the whole society, whereas the neighbors of an individual who chooses to fire-proof his home may benefit from a reduced risk of a fire spreading to their own houses. If external costs exist, such as pollution, the producer may choose to produce more of the product than would be produced if the producer were required to pay all associated environmental costs. Because responsibility or consequence for self-directed action lies partly outside the self, an element of externalization is involved. If there are external benefits, such as in public safety, less of the good may be produced than would be the case if the producer were to receive payment for the external benefits to others. For the purpose of these statements, overall cost and benefit to society is defined as the sum of the imputed monetary value of benefits and costs to all parties involved. Thus, unregulated markets in goods or services with significant externalities generate prices that do not reflect the full social cost or benefit of their transactions; such markets are therefore inefficient.