CreditMetrics™ — Technical Document

... We wish to estimate the volatility of value due to changes in credit quality, not just the expected loss. In our view, as important as default likelihood estimation is, it is only one link in the long chain of modeling and estimation that is necessary to fully assess credit risk (volatility) within ...

... We wish to estimate the volatility of value due to changes in credit quality, not just the expected loss. In our view, as important as default likelihood estimation is, it is only one link in the long chain of modeling and estimation that is necessary to fully assess credit risk (volatility) within ...

DISCOUNT RATES IN PERSONAL INJURY CLAIMS

... to determine the discount rate that best reflects the specific circumstances of the plaintiff, while at the same time, does not create considerable inequities in damages that are awarded within the same province and within Canada. This paper will discuss the mandated discount rates for each province ...

... to determine the discount rate that best reflects the specific circumstances of the plaintiff, while at the same time, does not create considerable inequities in damages that are awarded within the same province and within Canada. This paper will discuss the mandated discount rates for each province ...

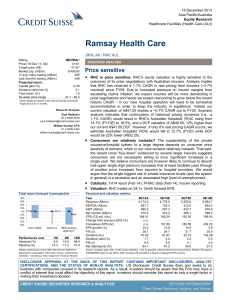

Ramsay Health Care 2013 12 18 - Price sensitive

... analysis indicates that continuation of historical pricing dynamics (i.e., a 1.1% CAGR) would result in RHC's Australian hospitals' ROIC rising from 14.7% (FY13E) to 18.5%, and a DCF valuation of A$46.50, 12% higher than our current A$41.50 DCF. However, if only 0% real pricing CAGR occurs, we estim ...

... analysis indicates that continuation of historical pricing dynamics (i.e., a 1.1% CAGR) would result in RHC's Australian hospitals' ROIC rising from 14.7% (FY13E) to 18.5%, and a DCF valuation of A$46.50, 12% higher than our current A$41.50 DCF. However, if only 0% real pricing CAGR occurs, we estim ...

The Capital Asset Pricing Model

... The traditional CAPM also assumes that there is a risk free asset as well as a potentially large collection of risky assets. Under these circumstances, as we’ve seen, all investors will hold some combination of the riskless asset and the tangency portfolio: the efficient portfolio of risky assets wi ...

... The traditional CAPM also assumes that there is a risk free asset as well as a potentially large collection of risky assets. Under these circumstances, as we’ve seen, all investors will hold some combination of the riskless asset and the tangency portfolio: the efficient portfolio of risky assets wi ...

Estimating and interpreting probability density functions

... conditions and market participants’ expectations. Most recently, techniques have been developed that use option prices to estimate or recover the entire expected distribution (probability density function, PDF) of future financial asset prices such as interest rates, exchange rates and equity prices ...

... conditions and market participants’ expectations. Most recently, techniques have been developed that use option prices to estimate or recover the entire expected distribution (probability density function, PDF) of future financial asset prices such as interest rates, exchange rates and equity prices ...

Consultation paper - Ministry of Justice

... future is inherently uncertain, we cannot know precisely how the costs of someone’s care will go up or down, we cannot always know what sort of earnings and pension they have lost out on, and we cannot always make accurate predictions about the way inflation will affect a sum of money. We do, howeve ...

... future is inherently uncertain, we cannot know precisely how the costs of someone’s care will go up or down, we cannot always know what sort of earnings and pension they have lost out on, and we cannot always make accurate predictions about the way inflation will affect a sum of money. We do, howeve ...

ESRB 2014 - European Systemic Risk Board

... Models (EWMs). These models identify indicators that signal economic vulnerabilities sufficiently early to enable policy-makers to take appropriate action in order to avoid crises or mitigate their severity. EWMs were first developed in the 1990s following currency crises in emerging market economie ...

... Models (EWMs). These models identify indicators that signal economic vulnerabilities sufficiently early to enable policy-makers to take appropriate action in order to avoid crises or mitigate their severity. EWMs were first developed in the 1990s following currency crises in emerging market economie ...

form 10-k toyota motor credit corporation

... automatically requests a credit bureau report from one of the major credit bureaus. We use a proprietary credit scoring system to evaluate an applicant’s risk profile. Factors used by the credit scoring system (based on the applicant’s credit history) include the terms of the contract, ability to pa ...

... automatically requests a credit bureau report from one of the major credit bureaus. We use a proprietary credit scoring system to evaluate an applicant’s risk profile. Factors used by the credit scoring system (based on the applicant’s credit history) include the terms of the contract, ability to pa ...

FREE Sample Here - Find the cheapest test bank for your

... C. the greater the level of inflation. D. none of the statements associated with this question are correct. 2. If the interest rate is 10% and cash flows are $1,000 at the end of year one and $2,000 at the end of year two, then the present value of these cash flows is A. $2,562. B. $3,200. C. $439. ...

... C. the greater the level of inflation. D. none of the statements associated with this question are correct. 2. If the interest rate is 10% and cash flows are $1,000 at the end of year one and $2,000 at the end of year two, then the present value of these cash flows is A. $2,562. B. $3,200. C. $439. ...

tactical timing of low volatility equity strategies

... the low volatility strategy was still above 9%. Moreover, in terms of risk-adjusted returns as measured by the Sharpe Ratio the two were even closer (0.09 difference). Though the expectation of interest rates increasing further might be widespread, generally central banks have indicated that this wi ...

... the low volatility strategy was still above 9%. Moreover, in terms of risk-adjusted returns as measured by the Sharpe Ratio the two were even closer (0.09 difference). Though the expectation of interest rates increasing further might be widespread, generally central banks have indicated that this wi ...

Going mainstream – how absolute return is moving into the

... which permitted hedge fund-like investment techniques in regulated funds. This legislation precipitated sharply rising inflows into absolute return strategies between 2002 and 2008 – although there were marked outflows during the peak of the credit crisis. Subsequently, net inflows have partially re ...

... which permitted hedge fund-like investment techniques in regulated funds. This legislation precipitated sharply rising inflows into absolute return strategies between 2002 and 2008 – although there were marked outflows during the peak of the credit crisis. Subsequently, net inflows have partially re ...

PDF

... Turvey (2002) empirically show that there is a negative relationship between export values and credit risks tagged on different importing countries. This implies that the export supply to an importing country with a high credit risk of non-payments is less elastic relative to the export supply to th ...

... Turvey (2002) empirically show that there is a negative relationship between export values and credit risks tagged on different importing countries. This implies that the export supply to an importing country with a high credit risk of non-payments is less elastic relative to the export supply to th ...

DP2012/05 The macroeconomic effects of a stable funding requirement

... general equilibrium models.7 Goodfriend and McCallum (2007) consider the roles of interest rate spreads in monetary policy analysis in a model with money and a banking sector. Christiano et al (2010) and Meh and Moran (2010) apply credit frictions of Bernanke et al (1999) to bank balance sheets. Kat ...

... general equilibrium models.7 Goodfriend and McCallum (2007) consider the roles of interest rate spreads in monetary policy analysis in a model with money and a banking sector. Christiano et al (2010) and Meh and Moran (2010) apply credit frictions of Bernanke et al (1999) to bank balance sheets. Kat ...

Financial Optimization Problems in Life and Pension Insurance

... they manage their policies? How should the systematic surplus that typically emerges over the policy terms (due to the prudent assessment of future interest rates) be redistributed to the policyholder(s)? What criteria should be imposed to ensure that policies are fair ? What happens if the actual y ...

... they manage their policies? How should the systematic surplus that typically emerges over the policy terms (due to the prudent assessment of future interest rates) be redistributed to the policyholder(s)? What criteria should be imposed to ensure that policies are fair ? What happens if the actual y ...

Effects of the Simultaneous Holding of Equity and Debt by Non

... Downloaded from rfs.oxfordjournals.org at Columbia University Libraries on February 22, 2011 ...

... Downloaded from rfs.oxfordjournals.org at Columbia University Libraries on February 22, 2011 ...

2016 Euro Commercial Paper Programme

... No person is authorised by the Issuer to give any information or to make any representation not contained in this Information Memorandum or any Pricing Supplement and any information or representation not contained therein must not be relied upon as having been authorised. Neither the Arranger nor ...

... No person is authorised by the Issuer to give any information or to make any representation not contained in this Information Memorandum or any Pricing Supplement and any information or representation not contained therein must not be relied upon as having been authorised. Neither the Arranger nor ...

Changing Business Practices in a New Regulatory Environment

... States Federal Reserve bank (the Fed) and its powerful tool: setting a target interest rate for banks to charge when they lend to each other. This tool essentially works as a money spigot; the target interest rate simply influences inter-bank lending rates. Typically, setting a higher rate tightens ...

... States Federal Reserve bank (the Fed) and its powerful tool: setting a target interest rate for banks to charge when they lend to each other. This tool essentially works as a money spigot; the target interest rate simply influences inter-bank lending rates. Typically, setting a higher rate tightens ...

Estimating the Effects of Foreclosure Counseling for Troubled Borrowers Assistant Professor

... what public programs are available to them. The counselor has repeated experiences with clients and familiarity with the array of programs available. The role of information on individuals’ take-up of social programs has been examined in a number of contexts [11; 12]. Any program that requires an af ...

... what public programs are available to them. The counselor has repeated experiences with clients and familiarity with the array of programs available. The role of information on individuals’ take-up of social programs has been examined in a number of contexts [11; 12]. Any program that requires an af ...

Avison Young 2016 Forecast Commercial Real Estate Canada, U.S.

... that negatively affect pricing or trading velocity are, in turn, countered with opportunistic buyers and lessees. ...

... that negatively affect pricing or trading velocity are, in turn, countered with opportunistic buyers and lessees. ...

Expected Returns on Major Asset Classes

... equity risk premium is an artifact, a derived quantity that depends on the time and place for which it is being estimated. Other premia, or differences of asset class expected returns, have the same characteristic. Ibbotson and Sinquefield’s (1976a, 1976b) work exemplifies the next period, the class ...

... equity risk premium is an artifact, a derived quantity that depends on the time and place for which it is being estimated. Other premia, or differences of asset class expected returns, have the same characteristic. Ibbotson and Sinquefield’s (1976a, 1976b) work exemplifies the next period, the class ...

IOSR Journal of Agriculture and Veterinary Science (IOSR-JAVS)

... extension agents who in most cases failed to deliver the information needed by them. In addition, the women and children who were mostly responsible for the rearing of the poultry were mostly left out of extension plans. This might have contributed to the negative sign of the extension variable. The ...

... extension agents who in most cases failed to deliver the information needed by them. In addition, the women and children who were mostly responsible for the rearing of the poultry were mostly left out of extension plans. This might have contributed to the negative sign of the extension variable. The ...

THE LINK BETWEEN DEFAULT AND RECOVERY RATES

... Applying the same methods and definitions as in Altman, Resti and Sironi (2005) this thesis seeks to empirically explain the relationship between default and recovery rates in the global corporate bond market. Findings in this thesis show that global default rates explain as much as 80 percent of th ...

... Applying the same methods and definitions as in Altman, Resti and Sironi (2005) this thesis seeks to empirically explain the relationship between default and recovery rates in the global corporate bond market. Findings in this thesis show that global default rates explain as much as 80 percent of th ...

Expected Returns on Major Asset Classes

... equity risk premium is an artifact, a derived quantity that depends on the time and place for which it is being estimated. Other premia, or differences of asset class expected returns, have the same characteristic. Ibbotson and Sinquefield’s (1976a, 1976b) work exemplifies the next period, the class ...

... equity risk premium is an artifact, a derived quantity that depends on the time and place for which it is being estimated. Other premia, or differences of asset class expected returns, have the same characteristic. Ibbotson and Sinquefield’s (1976a, 1976b) work exemplifies the next period, the class ...

ESSAYS ON DETERMINANTS OF FINANCIAL BEHAVIOR OF

... the author from an Internet-based marketplace for peer-to-peer lending. Peer-to-peer lending is a financial innovation consisting in direct lending and borrowing among individuals without intermediation of financial institutions. An advantage of using these data is that they include detailed informa ...

... the author from an Internet-based marketplace for peer-to-peer lending. Peer-to-peer lending is a financial innovation consisting in direct lending and borrowing among individuals without intermediation of financial institutions. An advantage of using these data is that they include detailed informa ...

Chapter 7 Bequests and the modified golden rule

... The optimality conditions (7.6), (7.7), and (7.8) illustrate a general principle of intertemporal optimization. First, no gain should be achievable by a reallocation of resources between two periods or between two generations. This is taken care of by the Euler equations (7.6) and (7.7).2 Second, th ...

... The optimality conditions (7.6), (7.7), and (7.8) illustrate a general principle of intertemporal optimization. First, no gain should be achievable by a reallocation of resources between two periods or between two generations. This is taken care of by the Euler equations (7.6) and (7.7).2 Second, th ...

Credit rationing

Credit rationing refers to the situation where lenders limit the supply of additional credit to borrowers who demand funds, even if the latter are willing to pay higher interest rates. It is an example of market imperfection, or market failure, as the price mechanism fails to bring about equilibrium in the market. It should not be confused with cases where credit is simply ""too expensive"" for some borrowers, that is, situations where the interest rate is deemed too high. On the contrary, the borrower would like to acquire the funds at the current rates, and the imperfection refers to the absence of equilibrium in spite of willing borrowers. In other words, at the prevailing market interest rate, demand exceeds supply, but lenders are not willing to either loan more funds, or raise the interest rate charged, as they are already maximising profits.