ECON 500 –Microeconomic Analysis and Policy Producer Theory

... II - The supply curve is shifted to the left by increases in the wage rate, III - The supply curve is shifted outward by increases in capital input IV - The rental rate of capital, v, is irrelevant to short-run supply decisions ...

... II - The supply curve is shifted to the left by increases in the wage rate, III - The supply curve is shifted outward by increases in capital input IV - The rental rate of capital, v, is irrelevant to short-run supply decisions ...

supply - Pearland ISD

... encourages the firm to produce more. Profits also appeal to people who may decide to join the marketplace. These companies will come in and compete with the already existing firms and try to get their share of the profit pie. ...

... encourages the firm to produce more. Profits also appeal to people who may decide to join the marketplace. These companies will come in and compete with the already existing firms and try to get their share of the profit pie. ...

The Impact of Standards Competition on Consumers

... Information about product performance can help consumers evaluate the two utility conditions, and this information also can be expressed in absolute or relative terms. In general, consumers value information about both absolute and relative performance of a product because it is predictive of the pr ...

... Information about product performance can help consumers evaluate the two utility conditions, and this information also can be expressed in absolute or relative terms. In general, consumers value information about both absolute and relative performance of a product because it is predictive of the pr ...

Pindyck/Rubinfeld Microeconomics

... For a factor market, economic rent is the difference between the payments made to a factor of production and the minimum amount that must be spent to obtain the use of that factor. Figure 14.11 ...

... For a factor market, economic rent is the difference between the payments made to a factor of production and the minimum amount that must be spent to obtain the use of that factor. Figure 14.11 ...

Pindyck/Rubinfeld Microeconomics

... For a factor market, economic rent is the difference between the payments made to a factor of production and the minimum amount that must be spent to obtain the use of that factor. Figure 14.11 ...

... For a factor market, economic rent is the difference between the payments made to a factor of production and the minimum amount that must be spent to obtain the use of that factor. Figure 14.11 ...

Quia - Quiz - Ladue Schools

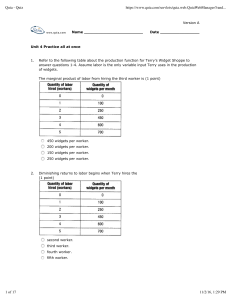

... 34. When a cherry orchard in Oregon adds an additional worker, the total cost of production increases by $24,000. Adding the worker increases total cherry output by 600 pounds. Therefore, the marginal cost of the last pound of cherries produced is: (1 point) ...

... 34. When a cherry orchard in Oregon adds an additional worker, the total cost of production increases by $24,000. Adding the worker increases total cherry output by 600 pounds. Therefore, the marginal cost of the last pound of cherries produced is: (1 point) ...

Market Definition, Elasticities and Surpluses

... Why? In the short run, there are often fewer substitutes to choose from, and consumers may find it difficult to adjust their behavior. For example, if the price of gasoline suddenly doubles, because we still have the same car and we still need to go to work, we will consume in the short run the same ...

... Why? In the short run, there are often fewer substitutes to choose from, and consumers may find it difficult to adjust their behavior. For example, if the price of gasoline suddenly doubles, because we still have the same car and we still need to go to work, we will consume in the short run the same ...

Integrating the Input Market and the Output Market

... When studying introductory college economics, students frequently do not grasp the workings of the input market. Toward the end of the semester, teachers may not have enough time to provide good nuanced teaching. In more instances, insufficient contrast between the input and output markets leaves st ...

... When studying introductory college economics, students frequently do not grasp the workings of the input market. Toward the end of the semester, teachers may not have enough time to provide good nuanced teaching. In more instances, insufficient contrast between the input and output markets leaves st ...

Chapter 3: Supply and Demand

... Equilibrium price: The price that equates the quantity demanded with the quantity supplied. Equilibrium quantity: The amount that people are willing to buy and sellers are willing to offer at the equilibrium price level. 2003 Prentice Hall Business Publishing ...

... Equilibrium price: The price that equates the quantity demanded with the quantity supplied. Equilibrium quantity: The amount that people are willing to buy and sellers are willing to offer at the equilibrium price level. 2003 Prentice Hall Business Publishing ...

2005.2nd Midterm.pp

... –A diminishing marginal rate of substitution is the key assumption of consumer theory. –A diminishing marginal rate of substitution is a general tendency for a person to be willing to give up less of good y to get one more unit of good x, and at the same time remain indifferent, as the quantity of g ...

... –A diminishing marginal rate of substitution is the key assumption of consumer theory. –A diminishing marginal rate of substitution is a general tendency for a person to be willing to give up less of good y to get one more unit of good x, and at the same time remain indifferent, as the quantity of g ...

Demand and Supply I. Demand Defined

... D. The Number of Demanders (Buyers) in the Market Recall that market demand is found by summing up all of the quantity demanded by individuals in the market at the various prices. Clearly, then, if the number of individuals in the market increases, then this sum will also increase, thereby increasi ...

... D. The Number of Demanders (Buyers) in the Market Recall that market demand is found by summing up all of the quantity demanded by individuals in the market at the various prices. Clearly, then, if the number of individuals in the market increases, then this sum will also increase, thereby increasi ...

CHAPTER 6

... ____ 11. Deregulation refers to the substitution of government rules and regulations for competition produced by the marketplace. ____ 12. As firms enter a perfectly competitive industry, the market supply curve shifts to the right. ____ 13. If firms are making zero economic profit, they will tend t ...

... ____ 11. Deregulation refers to the substitution of government rules and regulations for competition produced by the marketplace. ____ 12. As firms enter a perfectly competitive industry, the market supply curve shifts to the right. ____ 13. If firms are making zero economic profit, they will tend t ...

Chapter 6 Competitive Markets

... D) In the short run, a perfectly competitive firm can earn: 1. an economic profit when price is greater than min ATC. 2. a normal profit when price is equal to min ATC. 3. an economic loss when price is less than min ATC. E) The supply curve of a perfectly competitive firm is its marginal cost curve ...

... D) In the short run, a perfectly competitive firm can earn: 1. an economic profit when price is greater than min ATC. 2. a normal profit when price is equal to min ATC. 3. an economic loss when price is less than min ATC. E) The supply curve of a perfectly competitive firm is its marginal cost curve ...

MOSELEY ASSA 2014

... (rental rate), and the price of land (I will ignore land in what follows). According to marginal productivity theory, the prices of the factors of production are determined by the supply and demand ...

... (rental rate), and the price of land (I will ignore land in what follows). According to marginal productivity theory, the prices of the factors of production are determined by the supply and demand ...

budget constraint

... Marginal Rate of Substitution The Consumer’s Preferences The consumer is indifferent, or equally happy, with the combinations shown at points A, B, and C because they are all on the same curve. The Marginal Rate of Substitution The slope at any point on an indifference curve is the marginal ...

... Marginal Rate of Substitution The Consumer’s Preferences The consumer is indifferent, or equally happy, with the combinations shown at points A, B, and C because they are all on the same curve. The Marginal Rate of Substitution The slope at any point on an indifference curve is the marginal ...

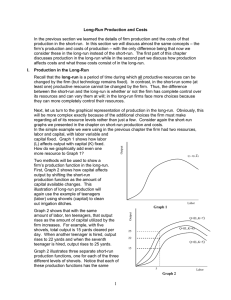

Long-Run Production and Costs

... Now it becomes clearer which of these three methods will the firm prefer to use. First note that the firm’s total revenue is the same regardless of the method used because in each the firm produces the same level of output. Hence, a profit maximizing firm would choose method 3 because costs of produ ...

... Now it becomes clearer which of these three methods will the firm prefer to use. First note that the firm’s total revenue is the same regardless of the method used because in each the firm produces the same level of output. Hence, a profit maximizing firm would choose method 3 because costs of produ ...

BEC1614 - FBL: My Reference Page

... Introduction to Economics Analysis Definition and reasons to study economics. The economic problem: scarce resources and unlimited wants. The circular flow. Differences between microeconomics and macroeconomics. Rational self-interest. Differences between positive and normative economics. The scienc ...

... Introduction to Economics Analysis Definition and reasons to study economics. The economic problem: scarce resources and unlimited wants. The circular flow. Differences between microeconomics and macroeconomics. Rational self-interest. Differences between positive and normative economics. The scienc ...

Chapter 3

... In actually applying this theory to the labor market, it is usually more interesting to look at what happens to labor when the price of the other input changes, but the same basic principles apply. In such situations, if labor and capital are gross complements, the firm’s long-run labor demand curve ...

... In actually applying this theory to the labor market, it is usually more interesting to look at what happens to labor when the price of the other input changes, but the same basic principles apply. In such situations, if labor and capital are gross complements, the firm’s long-run labor demand curve ...

Supply And Demand LESSON 14

... are at the same level. In this case, the quantity of items available for sale is equal to customer demand for those items. In a situation of equilibrium, prices tend to remain stable. When a product is at equilibrium, business owners are happy because their stock is selling well and customers are ha ...

... are at the same level. In this case, the quantity of items available for sale is equal to customer demand for those items. In a situation of equilibrium, prices tend to remain stable. When a product is at equilibrium, business owners are happy because their stock is selling well and customers are ha ...

- ePub WU - Wirtschaftsuniversität Wien

... about comparative advantage in the economic textbooks, in order to be able to study without prejudice the insights and implications of the numerical demonstration of comparative advantage in the Principles. While reading the Principles, I discovered that for truly understanding Ricardo’s proposition ...

... about comparative advantage in the economic textbooks, in order to be able to study without prejudice the insights and implications of the numerical demonstration of comparative advantage in the Principles. While reading the Principles, I discovered that for truly understanding Ricardo’s proposition ...

UNIT 3 (18 MARKS) PRODUCER BEHAVIOUR AND SUPPLY

... (a).Firstly, the economy has to decide what goods and services are to be produced .for instance which of the consumer goods like sugar, clothes, wheat, ghee etc, are to be produced and which of the capital goods like machines, tractors etc, are to be produced. Similarly, choice has also to be made b ...

... (a).Firstly, the economy has to decide what goods and services are to be produced .for instance which of the consumer goods like sugar, clothes, wheat, ghee etc, are to be produced and which of the capital goods like machines, tractors etc, are to be produced. Similarly, choice has also to be made b ...

Chapter 3

... Materials include content from Pearson Addison-Wesley which has been modified by the instructor and displayed with permission of the publisher. All rights reserved. ...

... Materials include content from Pearson Addison-Wesley which has been modified by the instructor and displayed with permission of the publisher. All rights reserved. ...

The Basics of Game Theory

... (in other words, they will undercut the opponent so long as lowering price does not imply incurring a loss. Always keep in mind that we are assuming rational behavior for the companies!) NOTE: If the products were differentiated the equilibrium would be reached for prices above MC and firms would be ...

... (in other words, they will undercut the opponent so long as lowering price does not imply incurring a loss. Always keep in mind that we are assuming rational behavior for the companies!) NOTE: If the products were differentiated the equilibrium would be reached for prices above MC and firms would be ...

English - CBSE Academic

... guns and butter, the famous example given by Samuelson. The guns symbolize defense goods and butter, the civilian goods. The example, therefore, symbolizes the problem of choice between civilian goods and war goods. In fact it is a problem of choice before all the countries of the world. Suppose if ...

... guns and butter, the famous example given by Samuelson. The guns symbolize defense goods and butter, the civilian goods. The example, therefore, symbolizes the problem of choice between civilian goods and war goods. In fact it is a problem of choice before all the countries of the world. Suppose if ...

No Slide Title

... sale so long as the MC is less than P. The value of the last unit produced and sold [bought] will be equal to the price, P. ...

... sale so long as the MC is less than P. The value of the last unit produced and sold [bought] will be equal to the price, P. ...

Comparative advantage

The theory of comparative advantage is an economic theory about the work gains from trade for individuals, firms, or nations that arise from differences in their factor endowments or technological progress. In an economic model, an agent has a comparative advantage over another in producing a particular good if he can produce that good at a lower relative opportunity cost or autarky price, i.e. at a lower relative marginal cost prior to trade. One does not compare the monetary costs of production or even the resource costs (labor needed per unit of output) of production. Instead, one must compare the opportunity costs of producing goods across countries. The closely related law or principle of comparative advantage holds that under free trade, an agent will produce more of and consume less of a good for which he has a comparative advantage.David Ricardo developed the classical theory of comparative advantage in 1817 to explain why countries engage in international trade even when one country's workers are more efficient at producing every single good than workers in other countries. He demonstrated that if two countries capable of producing two commodities engage in the free market, then each country will increase its overall consumption by exporting the good for which it has a comparative advantage while importing the other good, provided that there exist differences in labor productivity between both countries. Widely regarded as one of the most powerful yet counter-intuitive insights in economics, Ricardo's theory implies that comparative advantage rather than absolute advantage is responsible for much of international trade.