Lecture 5 - people.vcu.edu

... curves in the panel on the right. Either relationship is possible. For some goods (such as automobiles, education and housing) consumption usually increases with income. For other goods (macaroni and cheese in a box, second hand clothing and generic beer) consumption diminishes with income increases ...

... curves in the panel on the right. Either relationship is possible. For some goods (such as automobiles, education and housing) consumption usually increases with income. For other goods (macaroni and cheese in a box, second hand clothing and generic beer) consumption diminishes with income increases ...

PPA 723: Managerial Economics

... Key Concepts/Results Firms enter the market in response to economic profits and exit in response to losses—thereby altering the market price. LR equilibrium exists when no firms have an incentive to enter or exit, i.e. when economic profits equal zero. In LR equilibrium P = minimum LR AC Wi ...

... Key Concepts/Results Firms enter the market in response to economic profits and exit in response to losses—thereby altering the market price. LR equilibrium exists when no firms have an incentive to enter or exit, i.e. when economic profits equal zero. In LR equilibrium P = minimum LR AC Wi ...

A professor hires two aides, assigning them the tasks of reading

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

Consumption & Exchange

... difference between total use value (TUV) and total exchange value (I.e. total expenditure) (TEV) of a good. That is the extra amount of consumer is willing to pay over and above what he or she ...

... difference between total use value (TUV) and total exchange value (I.e. total expenditure) (TEV) of a good. That is the extra amount of consumer is willing to pay over and above what he or she ...

Marginal Revenue

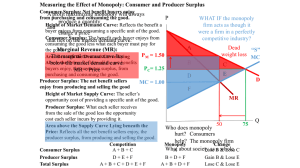

... Connecting the Pareto approach to efficiency with consumer and producer surplus Question: How did we argue that P monopoly was inefficient? We chose an individual, Joe, who Did not by a hamburger when the price was $1.50, the monopoly price. But would be a hamburger at a PM = 1.50 price of $1.40, a ...

... Connecting the Pareto approach to efficiency with consumer and producer surplus Question: How did we argue that P monopoly was inefficient? We chose an individual, Joe, who Did not by a hamburger when the price was $1.50, the monopoly price. But would be a hamburger at a PM = 1.50 price of $1.40, a ...

Econ 101, Sections 4 and 5, S09

... *. increases the firm's profit by $3/week. b. increases the firm's average total cost by $7/unit. c. increases the firm's average revenue by $10/unit. d. all of the above. 12. A firm in a competitive industry operates in the short-run at a price above its average total cost of production. In the lon ...

... *. increases the firm's profit by $3/week. b. increases the firm's average total cost by $7/unit. c. increases the firm's average revenue by $10/unit. d. all of the above. 12. A firm in a competitive industry operates in the short-run at a price above its average total cost of production. In the lon ...

Econ 101, Sections 4 and 5, S09

... 8. To say that a firm is a "price-taker" means that a. the firm would have to take a price cut in order to sell more. b. the firm's marginal revenue is less than its average revenue. *. the firm has no influence on market price. d. both b and c. 9. At an output level at which marginal cost is less t ...

... 8. To say that a firm is a "price-taker" means that a. the firm would have to take a price cut in order to sell more. b. the firm's marginal revenue is less than its average revenue. *. the firm has no influence on market price. d. both b and c. 9. At an output level at which marginal cost is less t ...

Economics 160

... 1. Short run: a period of time over which at least one input is fixed. A fixed input is an input whose quantity cannot be varied (over some non-trivial period of time). 2. a. Labor (L) Total Product (Q) Marginal Product (MP) ...

... 1. Short run: a period of time over which at least one input is fixed. A fixed input is an input whose quantity cannot be varied (over some non-trivial period of time). 2. a. Labor (L) Total Product (Q) Marginal Product (MP) ...

I. Output Decisions by Firms

... cannot determine the market price. That is if a firm in a perfectly competitive industry decides to increase production, that will have no effect on the market price. (2) The products sold are identical. We say that firms sell homogeneous products. There is nothing to differentiate between Firm A’s ...

... cannot determine the market price. That is if a firm in a perfectly competitive industry decides to increase production, that will have no effect on the market price. (2) The products sold are identical. We say that firms sell homogeneous products. There is nothing to differentiate between Firm A’s ...

Monopolistic firms can increase sales by reducing the price. As the

... which total revenue is rising at the same rate as total cost. For this firm, as output is increased up to about 300 units, total revenue is rising more rapidly than total cost for each additional unit produced and profits are getting larger. Up to this point costs increase at a diminishing rate—the ...

... which total revenue is rising at the same rate as total cost. For this firm, as output is increased up to about 300 units, total revenue is rising more rapidly than total cost for each additional unit produced and profits are getting larger. Up to this point costs increase at a diminishing rate—the ...