Chapter 6 Equilibrium Surplus Shortage 11-14-11

... Surplus- is the result of quantity supplied of a product is greater than quantity demanded. This is caused by a price greater than market equilibrium price. ...

... Surplus- is the result of quantity supplied of a product is greater than quantity demanded. This is caused by a price greater than market equilibrium price. ...

6.2 Notes

... 1. What happens at the point where buyers and sellers agree? Use these terms in your answer: market equilibrium, equilibrium price, equilibrium quantity. 2. Why do competitive markets move toward equilibrium? 3. Look at the balance scale in this section, which represents equilibrium. Create your own ...

... 1. What happens at the point where buyers and sellers agree? Use these terms in your answer: market equilibrium, equilibrium price, equilibrium quantity. 2. Why do competitive markets move toward equilibrium? 3. Look at the balance scale in this section, which represents equilibrium. Create your own ...

Microeconomics I Syllabus Instructor

... Course Overview: The course will cover standard models in microeconomics, such as individual decision-making with and without uncertainty, models of consumer behavior and producer behavior under perfect competition, the Arrow-Debreu general equilibrium model, and some basic issues in welfare economi ...

... Course Overview: The course will cover standard models in microeconomics, such as individual decision-making with and without uncertainty, models of consumer behavior and producer behavior under perfect competition, the Arrow-Debreu general equilibrium model, and some basic issues in welfare economi ...

Which of the following influences does NOT shift the supply curve?

... Both equilibrium price and output will increase Equilibrium quantity will decrease but we don’t have enough information to determine the change in equilibrium price Equilibrium price will increase but we don’t have enough information to determine the change in equilibrium quantity ...

... Both equilibrium price and output will increase Equilibrium quantity will decrease but we don’t have enough information to determine the change in equilibrium price Equilibrium price will increase but we don’t have enough information to determine the change in equilibrium quantity ...

Homework Quiz 3 - Change your password

... 2. A report is published that the pesticide Alar has very harmful health effects on apple eaters. The same report mentions that growing conditions for apples will be unusually favorable this year. Graph markets for regular apples and organic apples. Should consumers expect higher or lower prices thi ...

... 2. A report is published that the pesticide Alar has very harmful health effects on apple eaters. The same report mentions that growing conditions for apples will be unusually favorable this year. Graph markets for regular apples and organic apples. Should consumers expect higher or lower prices thi ...

Problem Set #3 - University of Notre Dame

... 1. What happens to equilibrium supply and demand if a price floor is set below the equilibrium price? 2. What happens to producer surplus when a price ceiling (below the equilibrium price) is enacted? What happens to consumer surplus? Will there be a shortage or a surplus in the new equilibrium? 3. ...

... 1. What happens to equilibrium supply and demand if a price floor is set below the equilibrium price? 2. What happens to producer surplus when a price ceiling (below the equilibrium price) is enacted? What happens to consumer surplus? Will there be a shortage or a surplus in the new equilibrium? 3. ...

Chapter 8.1 Market Equilbrium

... signals or wants by employing more factors of production to make sweaters. No one is telling them they have to do it. They do so because they want to make more money. Suppliers or producers make what people want based on what they will buy. ...

... signals or wants by employing more factors of production to make sweaters. No one is telling them they have to do it. They do so because they want to make more money. Suppliers or producers make what people want based on what they will buy. ...

Walras` Law

... There is no way to make some strictly better off without making someone else worse off; All of the gains from trade have been exhausted; There are no (further) mutually advantageous trades to be made. ...

... There is no way to make some strictly better off without making someone else worse off; All of the gains from trade have been exhausted; There are no (further) mutually advantageous trades to be made. ...

Neoclassical

... achieve optimal outcomes for all Economic decisions are made on the basis of ‘utility maximization’ The economy is a dynamic system with a multitude of individual players, none the less it reaches an equilibrium where these forces are in balance. ...

... achieve optimal outcomes for all Economic decisions are made on the basis of ‘utility maximization’ The economy is a dynamic system with a multitude of individual players, none the less it reaches an equilibrium where these forces are in balance. ...

Quiz1

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=1000-10P and the market supply curve is given by Qs = -50+25P a) [2 marks] What are the equilibrium price and quantity in this market? To find the equilibrium set Qd=Qs 1000-10P=-50+25P P=30 At a price of 30, the mark ...

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=1000-10P and the market supply curve is given by Qs = -50+25P a) [2 marks] What are the equilibrium price and quantity in this market? To find the equilibrium set Qd=Qs 1000-10P=-50+25P P=30 At a price of 30, the mark ...

Excess Demands

... solution to maximization problem (2) could be written xiM (p, p · ei) where xiM is the vector of Marshallian demand functions Cobb–Douglas example : (xi1)a(xi2)1−a then ...

... solution to maximization problem (2) could be written xiM (p, p · ei) where xiM is the vector of Marshallian demand functions Cobb–Douglas example : (xi1)a(xi2)1−a then ...

Quiz1

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=150-15 Pa+10Pb and the market supply curve is given by Qs = -250+10 P a+ 5Pb. a) [3 marks] What are the ranges of Pa and Pb if the equilibrium prices and quantity are positive in this market? 150-15 Pa+10Pb= -250+10 P ...

... Question 1. [5 marks] Suppose the market demand curve for a product is given by Qd=150-15 Pa+10Pb and the market supply curve is given by Qs = -250+10 P a+ 5Pb. a) [3 marks] What are the ranges of Pa and Pb if the equilibrium prices and quantity are positive in this market? 150-15 Pa+10Pb= -250+10 P ...

Document

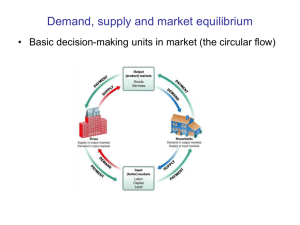

... • Market demand: The sum of the quantities of a good demanded per period by all the households buying in that market. ...

... • Market demand: The sum of the quantities of a good demanded per period by all the households buying in that market. ...

Supply and demand in math form

... and Qs = 6 and so we would have a shortage of 8 units. A price ceiling of 4 would be mean Qd = 10 and Qs = 18. This would mean a surplus of 8 units and a surplus leads to a lower price. Price could fall with a ceiling it just can not go above. A price ceiling of 4 would not change the market equilib ...

... and Qs = 6 and so we would have a shortage of 8 units. A price ceiling of 4 would be mean Qd = 10 and Qs = 18. This would mean a surplus of 8 units and a surplus leads to a lower price. Price could fall with a ceiling it just can not go above. A price ceiling of 4 would not change the market equilib ...

Assume that demand and supply are given be the following

... Assume that demand and supply are given be the following equations: Demand: ...

... Assume that demand and supply are given be the following equations: Demand: ...

Algorithmic Game Theory and Internet Computing

... on the Jacobian of the excess demand functions (the determinants of the minors be positive if of even order and negative if of odd order) ...

... on the Jacobian of the excess demand functions (the determinants of the minors be positive if of even order and negative if of odd order) ...

ECON-2.10-13.12 Market Intro

... Would you expect prison life to be as bad if inmates were allowed to freely participate in market exchanges as in the “outside” economy? Explain. ...

... Would you expect prison life to be as bad if inmates were allowed to freely participate in market exchanges as in the “outside” economy? Explain. ...

Appendix Summary

... Chapter 1 Summary Linear Functions Distance Slope: Parallel slope Perpendicular slope Write the Equation of a Line: Given different information (2 pts, parallel or perpendicular, etc.) Interest: ...

... Chapter 1 Summary Linear Functions Distance Slope: Parallel slope Perpendicular slope Write the Equation of a Line: Given different information (2 pts, parallel or perpendicular, etc.) Interest: ...

Changes in Price

... Students will identify the determinants that create changes in price Students will explain how a market reacts to a fall in supply by moving to a new equilibrium Students will explain how a market reacts to shifts in demand by moving to a new equilibrium Changes in Price Factors that affect ...

... Students will identify the determinants that create changes in price Students will explain how a market reacts to a fall in supply by moving to a new equilibrium Students will explain how a market reacts to shifts in demand by moving to a new equilibrium Changes in Price Factors that affect ...

Practice Exam 1

... ____ 1. Scarcity is a problem only for the poor. ____ 2. Because resources are limited, people must learn to make decisions with opportunity costs. ____ 3. To the left of a minimum point, the slope is negative, to the right, the slope is positive. ____ 4. Production efficiency requires producing at ...

... ____ 1. Scarcity is a problem only for the poor. ____ 2. Because resources are limited, people must learn to make decisions with opportunity costs. ____ 3. To the left of a minimum point, the slope is negative, to the right, the slope is positive. ____ 4. Production efficiency requires producing at ...