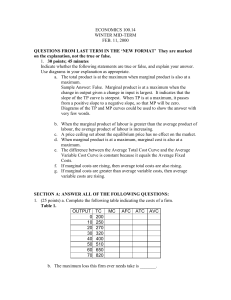

EFL Lesson 4

... actions by special interest groups that can impose costs on the general public, or because social goals other than economic efficiency are being pursued. Price controls are often advocated by special interest groups. Price controls reduce the quantity of goods and services consumer, thus depriving ...

... actions by special interest groups that can impose costs on the general public, or because social goals other than economic efficiency are being pursued. Price controls are often advocated by special interest groups. Price controls reduce the quantity of goods and services consumer, thus depriving ...

Prices in a Free-Market Economy

... be understood by anyone that is competent in Differential Equations. ...

... be understood by anyone that is competent in Differential Equations. ...

Existence proof for an exchange economy in the standard Arrow

... The basic hypotheses involve the utility function uh and the demand correspondence xh (p) of each consumer: the rst must be continuous and strictly increasing wheras the latter must take up values in RC+ and be homogeneous of degree zero so to "absorb" scalings of the parameter p by a factor α > 0. ...

... The basic hypotheses involve the utility function uh and the demand correspondence xh (p) of each consumer: the rst must be continuous and strictly increasing wheras the latter must take up values in RC+ and be homogeneous of degree zero so to "absorb" scalings of the parameter p by a factor α > 0. ...

3. Supply and Demand curves I answers

... The supply curve is P=$25. The demand curve = 900 - 30P. The quantity demanded is 150 so that is also the quantity supplied. ...

... The supply curve is P=$25. The demand curve = 900 - 30P. The quantity demanded is 150 so that is also the quantity supplied. ...

Section 5.3 Force and Motion in 2 Dimensions

... It is important to realize that equilibrium can occur no matter how many forces act on an object. As long as the resultant is zero, the net force is zero and the object is in equilibrium. Go over Figure 5-11 p. 131 Resultant Force – vector sum of 2 or more vectors. Equilibrium – condition in which n ...

... It is important to realize that equilibrium can occur no matter how many forces act on an object. As long as the resultant is zero, the net force is zero and the object is in equilibrium. Go over Figure 5-11 p. 131 Resultant Force – vector sum of 2 or more vectors. Equilibrium – condition in which n ...

Supply / Demand / Equilibrium

... Now, remember back to our activity one more time. How did the buyer and the seller come to an agreement? You had to agree on the same price. If the buyer wanted to buy for $1 and the seller wanted to sell the candy bar for $5, nothing would happen. But, if they could come to an agreement, a sale wou ...

... Now, remember back to our activity one more time. How did the buyer and the seller come to an agreement? You had to agree on the same price. If the buyer wanted to buy for $1 and the seller wanted to sell the candy bar for $5, nothing would happen. But, if they could come to an agreement, a sale wou ...

ECON 202 – 2 nd Quiz KEY

... 1. Suppose that in October the price of a cup of cafe latte was $1.50 and 400 lattes were consumed. In November the price of a latte was $2.00 and 200 lattes were consumed. What might have caused this change? The price of tea (a substitute for cafe lattes) fell. 2. A supply curve is defined as the r ...

... 1. Suppose that in October the price of a cup of cafe latte was $1.50 and 400 lattes were consumed. In November the price of a latte was $2.00 and 200 lattes were consumed. What might have caused this change? The price of tea (a substitute for cafe lattes) fell. 2. A supply curve is defined as the r ...

Chapter 2

... (a) Find the equilibrium price and quantity of seats for a football game (using algebra and a graph). (b) Suppose the government prohibits ticket scalping (selling tickets above their face value), and the face value of tickets is $50 (this policy places a pricing ceiling at $50). How many consumers ...

... (a) Find the equilibrium price and quantity of seats for a football game (using algebra and a graph). (b) Suppose the government prohibits ticket scalping (selling tickets above their face value), and the face value of tickets is $50 (this policy places a pricing ceiling at $50). How many consumers ...

CH. 6, Sec. 1 DEMAND

... parts of the total economy—the choices we make as individuals. Demand = the quantities of a good that consumers are willing and able to purchase at various prices during a given period of time. ...

... parts of the total economy—the choices we make as individuals. Demand = the quantities of a good that consumers are willing and able to purchase at various prices during a given period of time. ...

w06ex1 - Rose

... A. the tax burden on consumers and firms is the same. B. firms pay all the tax. C. both the consumers and firms pay the tax, but the tax burden on consumers is greater. D. both the consumers and the firms pay the tax, but the tax burden on firms is greater. E. consumers pay all the tax. Page 2 ...

... A. the tax burden on consumers and firms is the same. B. firms pay all the tax. C. both the consumers and firms pay the tax, but the tax burden on consumers is greater. D. both the consumers and the firms pay the tax, but the tax burden on firms is greater. E. consumers pay all the tax. Page 2 ...

Study guide 2005 1 st mid-term

... 1. (30 points) Assume that a retail clothing store is operating under conditions of monopolistic competition. First draw a diagram showing the firm when the industry is in long-run equilibrium. Then draw a diagram showing the impact of an increase in the demand for clothing on its output, price and ...

... 1. (30 points) Assume that a retail clothing store is operating under conditions of monopolistic competition. First draw a diagram showing the firm when the industry is in long-run equilibrium. Then draw a diagram showing the impact of an increase in the demand for clothing on its output, price and ...

Review of Basics

... Defining the Relevant Market A market refers to the interaction between consumers and producers to exchange a well-defined commodity Defining the market context is one of the more critical steps in economic analysis Specifying the Market Model The form of the model varies with the objectiv ...

... Defining the Relevant Market A market refers to the interaction between consumers and producers to exchange a well-defined commodity Defining the market context is one of the more critical steps in economic analysis Specifying the Market Model The form of the model varies with the objectiv ...

EC202 Sample Exam Paper - DARP

... 10. Anne has an initial stock of wealth W and risks losing some of this wealth through re. The probability of such a re is known to be π and the loss if the re occurs would be L (where L < W ). Insurance cover against a re is available at a premium κ, where κ > πL; it is also possible to take o ...

... 10. Anne has an initial stock of wealth W and risks losing some of this wealth through re. The probability of such a re is known to be π and the loss if the re occurs would be L (where L < W ). Insurance cover against a re is available at a premium κ, where κ > πL; it is also possible to take o ...

uwcmaastricht-econ

... As I had already mentioned in class, except for the last question, your answers should be in essay form, which means that a simple list of points is not enough. Abbreviations such as P or Q are only accepted in the diagram: your answers should include full words, so supply (not S!), demand (not ...

... As I had already mentioned in class, except for the last question, your answers should be in essay form, which means that a simple list of points is not enough. Abbreviations such as P or Q are only accepted in the diagram: your answers should include full words, so supply (not S!), demand (not ...

MicroPreS_Part 1

... consumers, workers, firms or managers. This study involves both the behavior of these economic agents on their own and the way their behavior interacts to form larger units, such as markets. ...

... consumers, workers, firms or managers. This study involves both the behavior of these economic agents on their own and the way their behavior interacts to form larger units, such as markets. ...

Econ 101, sections 4 and 5, S09

... a. Positive statements can, in principle, be confirmed or refuted by examining evidence. b. Normative statements involve value judgments. *. Any statement making a claim about the future is necessarily normative. d. Deciding what is good or bad policy is not just a matter of science. 14. Which of th ...

... a. Positive statements can, in principle, be confirmed or refuted by examining evidence. b. Normative statements involve value judgments. *. Any statement making a claim about the future is necessarily normative. d. Deciding what is good or bad policy is not just a matter of science. 14. Which of th ...

Finding Equilibrium

... reduce prices to sell their products. This creates a new market equilibrium. ...

... reduce prices to sell their products. This creates a new market equilibrium. ...