Econ Unit 3 Micro Study Guide

... 18. New York established rent controls for apartments in the city. What happened to as a result of this mandated price ceiling? 19. What type of price control is the government mandated minimum wage? 20. Draw and correctly label these Supply and Demand graphs, showing the correct shift and new equil ...

... 18. New York established rent controls for apartments in the city. What happened to as a result of this mandated price ceiling? 19. What type of price control is the government mandated minimum wage? 20. Draw and correctly label these Supply and Demand graphs, showing the correct shift and new equil ...

today

... When q = 13.90388, p is given by p = 15 − 14 q = 11.524. When q = 3.5961, p is given by p = 15 − 14 q = 14.1009. So there are actually two equilibria. (b) Suppose the government imposes a tax of $1.50 per unit. Modify the system above to reflect this fact. (You should write both the demand and suppl ...

... When q = 13.90388, p is given by p = 15 − 14 q = 11.524. When q = 3.5961, p is given by p = 15 − 14 q = 14.1009. So there are actually two equilibria. (b) Suppose the government imposes a tax of $1.50 per unit. Modify the system above to reflect this fact. (You should write both the demand and suppl ...

The Market SD

... tea increases its popularity among consumers. The company is ready to make any amount of iced tea necessary to satisfy changes in demand. ...

... tea increases its popularity among consumers. The company is ready to make any amount of iced tea necessary to satisfy changes in demand. ...

Demand and Supply

... The amounts of a product that consumers are able and willing to purchase at various different prices ...

... The amounts of a product that consumers are able and willing to purchase at various different prices ...

Document

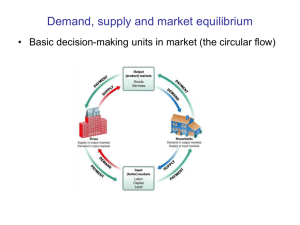

... • Market demand: The sum of the quantities of a good demanded per period by all the households buying in that market. ...

... • Market demand: The sum of the quantities of a good demanded per period by all the households buying in that market. ...

Lesson 3.1 WHAT IS AN ECONOMY?

... • Fixed costs are costs that must be paid regardless of how much of a good or service is produced. • Fixed costs are also called sunk costs. • Variable costs are costs that go up and down depending on the quantity of the good or service produced. ...

... • Fixed costs are costs that must be paid regardless of how much of a good or service is produced. • Fixed costs are also called sunk costs. • Variable costs are costs that go up and down depending on the quantity of the good or service produced. ...

Project Dr. Sharp

... zero, with price at $5 represents the fixed cost amount the seller will pay regardless of how much they produce. Supply increases after the price of $5 (law of supply) as price increases it becomes more attractive for sellers to produce more of a good. b. (4 points) Explain in words why the demand i ...

... zero, with price at $5 represents the fixed cost amount the seller will pay regardless of how much they produce. Supply increases after the price of $5 (law of supply) as price increases it becomes more attractive for sellers to produce more of a good. b. (4 points) Explain in words why the demand i ...

ECONOMICS 2306

... for the exam. You should know definitions of terms; formulas and how to use them; graphs, what they represent, and how to draw and read them; tables of data and how to work with them. CHAPTER 1 Economics, scarcity, and choice Resources and payments to resource owners Economic decision makers and the ...

... for the exam. You should know definitions of terms; formulas and how to use them; graphs, what they represent, and how to draw and read them; tables of data and how to work with them. CHAPTER 1 Economics, scarcity, and choice Resources and payments to resource owners Economic decision makers and the ...

problem_set_3

... A local seafood restaurant is incredibly popular with the town, and is especially loved for its fried calamari. However, the restaurant’s surrounding neighbors complain that whenever the chefs are cooking, they cannot rid their homes of the unpleasant, fishy aroma. ii. A parking lot, which offers pa ...

... A local seafood restaurant is incredibly popular with the town, and is especially loved for its fried calamari. However, the restaurant’s surrounding neighbors complain that whenever the chefs are cooking, they cannot rid their homes of the unpleasant, fishy aroma. ii. A parking lot, which offers pa ...

Econ 111: Principles of Economics

... tickets per day, while at $ 7.5 per ticket, it will sell 600 tickets per day. What is the price elasticity of demand for movies at this theater for a price change from $ 7.5 to $ 8.5? ...

... tickets per day, while at $ 7.5 per ticket, it will sell 600 tickets per day. What is the price elasticity of demand for movies at this theater for a price change from $ 7.5 to $ 8.5? ...

Shift in the Demand Curve

... I. Producing ____________ and ____________ A. Economic ____________ includes goods and services. B. Four Factors of Production 1. ____________ resources. a. gifts of nature 2. ____________ resources a. labor (nation’s workforce) 3. ____________(goods) a. tools, machinery, and buildings used to make ...

... I. Producing ____________ and ____________ A. Economic ____________ includes goods and services. B. Four Factors of Production 1. ____________ resources. a. gifts of nature 2. ____________ resources a. labor (nation’s workforce) 3. ____________(goods) a. tools, machinery, and buildings used to make ...

CHAPTER 3: Demand and Supply

... As the price a good rises, it become relatively more expensive and other goods become relatively cheaper → Quantity Demanded↓ The Income Effect of a Change in Price on the Quantity Demanded (Pg. 59) As the price a good rises, Real Income or Purchasing Power↓ → Cannot afford to buy the same amount of ...

... As the price a good rises, it become relatively more expensive and other goods become relatively cheaper → Quantity Demanded↓ The Income Effect of a Change in Price on the Quantity Demanded (Pg. 59) As the price a good rises, Real Income or Purchasing Power↓ → Cannot afford to buy the same amount of ...

Civics Unit 2 Study Guide

... 2. A drought will cause the supply curve of vegetables to shift which way? 3. A legal maximum price at which a good can be sold is called what? 4. According to the Law of Demand, quantity demanded goes up as price moves 5. According to the Law of Supply, if price increases, supply does what? 6. Adam ...

... 2. A drought will cause the supply curve of vegetables to shift which way? 3. A legal maximum price at which a good can be sold is called what? 4. According to the Law of Demand, quantity demanded goes up as price moves 5. According to the Law of Supply, if price increases, supply does what? 6. Adam ...

PowerPoint: Market Equilibrium & Disequilibrium

... the demand to producers 300 from will 500accept at a lower prices. Lower price of £5. Suppliers prices turn the attract do notinhave some consumers to to information or time buy. Thesupply process adjust continues untiland thestill immediately surplus disappears and offer 600 for sale at equilibrium ...

... the demand to producers 300 from will 500accept at a lower prices. Lower price of £5. Suppliers prices turn the attract do notinhave some consumers to to information or time buy. Thesupply process adjust continues untiland thestill immediately surplus disappears and offer 600 for sale at equilibrium ...

Section 2.4 Linear Functions and Models

... X-axis time since purchase Y-axis value Use two intercepts (0, initial value) and (time until value is zero, 0) to form line ...

... X-axis time since purchase Y-axis value Use two intercepts (0, initial value) and (time until value is zero, 0) to form line ...

The Demand Curve and The Demand Schedule

... A table showing how much of a good or service consumers will want to buy at different prices See pg. 50; Figure 5.1 ...

... A table showing how much of a good or service consumers will want to buy at different prices See pg. 50; Figure 5.1 ...

Economics - Seneca High School

... people are actually willing and able to buy given the prices and choices available. ...

... people are actually willing and able to buy given the prices and choices available. ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑