microeconomics self-evaluation questions - UNC Kenan

... (15 *20), respectively. The increase in total revenue from 10 to 15 units is $100 ($300 -$200) and the increase in quantity is 5 (15-10). Thus, the slope is $20 ($100/5). In economic terms, the slope of the total revenue curve can be interpreted as the additional revenue from selling one additional ...

... (15 *20), respectively. The increase in total revenue from 10 to 15 units is $100 ($300 -$200) and the increase in quantity is 5 (15-10). Thus, the slope is $20 ($100/5). In economic terms, the slope of the total revenue curve can be interpreted as the additional revenue from selling one additional ...

Changes in Supply and Demand

... their prices to make more money. The higher price leads to an increase in the quantity supplied and a decrease in the quantity demanded. At the new equilibrium price, quantity supplied and quantity demanded are again equal. But the new equilibrium price is higher and the new equilibrium quantity is ...

... their prices to make more money. The higher price leads to an increase in the quantity supplied and a decrease in the quantity demanded. At the new equilibrium price, quantity supplied and quantity demanded are again equal. But the new equilibrium price is higher and the new equilibrium quantity is ...

APEconHW#3aFall2014

... accepted at a cost of 10% per day until they are graded and handed back (2 days after the due date). At that point, I will not accept your homework and you will receive a zero. Please be as neat as possible and show all of your work. If you need more room, use the back of each sheet and indicate you ...

... accepted at a cost of 10% per day until they are graded and handed back (2 days after the due date). At that point, I will not accept your homework and you will receive a zero. Please be as neat as possible and show all of your work. If you need more room, use the back of each sheet and indicate you ...

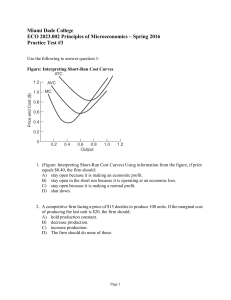

Spring 2016 Practice Test #3

... 37. If many firms enter a competitive market, and demand for raw materials increases, then the: A) SRATC curve will shift down. B) long-run industry supply curve will slope up. C) long-run industry supply curve will slope down. D) average fixed cost curve will slope up. ...

... 37. If many firms enter a competitive market, and demand for raw materials increases, then the: A) SRATC curve will shift down. B) long-run industry supply curve will slope up. C) long-run industry supply curve will slope down. D) average fixed cost curve will slope up. ...

Tutorial

... a. leftward shift of the supply curve. b. upward movement along the supply curve. c. firm to supply a larger quantity at any given price. d. downward movement along the supply curve. C. When price changes, the supply curve itself does not change, but when other things change, the whole curve will sh ...

... a. leftward shift of the supply curve. b. upward movement along the supply curve. c. firm to supply a larger quantity at any given price. d. downward movement along the supply curve. C. When price changes, the supply curve itself does not change, but when other things change, the whole curve will sh ...

ECO352_Precept_Wk07.pdf

... Each firm's output denoted by q . Firm's TC = ( 120 – 0.002 Q ) q + 0.5 q Thus higher industry output shifts down each firm's cost curves: this is external economy Possible reasons: An industry-wide input produced with economies of scale, or industry-wide know-how spreads more easily to individual f ...

... Each firm's output denoted by q . Firm's TC = ( 120 – 0.002 Q ) q + 0.5 q Thus higher industry output shifts down each firm's cost curves: this is external economy Possible reasons: An industry-wide input produced with economies of scale, or industry-wide know-how spreads more easily to individual f ...

Economics 101 Syllabus

... To find what happens in the short run, set the NEW demand curve equal to the short-run supply curve that you found in part (b). This is the immediate impact of the fall in demand, before firms have time to enter or exit. -130 + 13/2 P = 1800 – 20 P 1930 = 53/2 P P = $72.83; Q =343.60 (or 344) There ...

... To find what happens in the short run, set the NEW demand curve equal to the short-run supply curve that you found in part (b). This is the immediate impact of the fall in demand, before firms have time to enter or exit. -130 + 13/2 P = 1800 – 20 P 1930 = 53/2 P P = $72.83; Q =343.60 (or 344) There ...

Sect 1.4b Linear Models

... demand function. b. Interpret the slope. c. Find the equilibrium price. Remember that you found the supply function in problem 2. d. Use your graphing calculator to draw the graphs of the supply and demand functions and sketch the graphs. Then use the intersect function to confirm equilibrium price. ...

... demand function. b. Interpret the slope. c. Find the equilibrium price. Remember that you found the supply function in problem 2. d. Use your graphing calculator to draw the graphs of the supply and demand functions and sketch the graphs. Then use the intersect function to confirm equilibrium price. ...

Economics 1 - Bakersfield College

... b. that person can produce a good for a lower opportunity cost than another person. c. that person can produce a certain good and the other person can not. d. that person is stronger than the other person. 29. Anything that raises the cost of production causes: a. the demand curve to move right. b. ...

... b. that person can produce a good for a lower opportunity cost than another person. c. that person can produce a certain good and the other person can not. d. that person is stronger than the other person. 29. Anything that raises the cost of production causes: a. the demand curve to move right. b. ...

Economics in the Headlines

... and ability of a supplier to produce a product. Supply can be affected by the number of firms in the industry, the cost of production, productivity, government policy, and natural disasters. ...

... and ability of a supplier to produce a product. Supply can be affected by the number of firms in the industry, the cost of production, productivity, government policy, and natural disasters. ...

Form C

... hotel room is $30 a night. In the summer, all of the rooms are occupied and the price of a room is $100 per night. In the winter, only half of the rooms are occupied and the room rate is $30 a night. The local authorities introduce an ”occupancy tax” of $10 per night. That is, the motel owners must ...

... hotel room is $30 a night. In the summer, all of the rooms are occupied and the price of a room is $100 per night. In the winter, only half of the rooms are occupied and the room rate is $30 a night. The local authorities introduce an ”occupancy tax” of $10 per night. That is, the motel owners must ...

Market Structures

... 1. Public ownership (nationalization): government takes over the running of the monopoly, decides output and prices. However- this solution doesn’t have any competition and hence inefficiency can arise 2. Public regulation, separates role of producer and supervisor, allow efficiency of profit motive ...

... 1. Public ownership (nationalization): government takes over the running of the monopoly, decides output and prices. However- this solution doesn’t have any competition and hence inefficiency can arise 2. Public regulation, separates role of producer and supervisor, allow efficiency of profit motive ...

Equilibrium Review

... and assist lower-income groups. The laws cause disequilibrium, resulting in a shortage. When rent control is repealed, the prices increase to equilibrium, and lowerincome residents are forced to leave. ...

... and assist lower-income groups. The laws cause disequilibrium, resulting in a shortage. When rent control is repealed, the prices increase to equilibrium, and lowerincome residents are forced to leave. ...

HWPS#2

... displays the various quantities demanded at different prices, holding other things constant (ceteris paribus) such as income, the number of buyers in the market, the prices of related goods, and other non-price factors or variables that affect demand. A “change in demand” shifts the demand curve (or ...

... displays the various quantities demanded at different prices, holding other things constant (ceteris paribus) such as income, the number of buyers in the market, the prices of related goods, and other non-price factors or variables that affect demand. A “change in demand” shifts the demand curve (or ...

Economics Chapter 4

... • Ceteris paribus is a Latin phrase economists use meaning “all other things held constant.” • A demand curve is accurate only as long as the ceteris paribus assumption is true. • When the ceteris paribus assumption is dropped, movement no longer occurs along the demand curve. Rather, the entire dem ...

... • Ceteris paribus is a Latin phrase economists use meaning “all other things held constant.” • A demand curve is accurate only as long as the ceteris paribus assumption is true. • When the ceteris paribus assumption is dropped, movement no longer occurs along the demand curve. Rather, the entire dem ...

ECON 160 Spring 2011 Week 05 Classnotes February 22

... ECON 160 Spring 2011 Week 05 Classnotes February 22-24, 2011 (Chapter 5) 1. Market Demand determines Price : As you look at all the goods available to be purchased, the food, the clothing, the cars, etc. the price you have to pay is determined by all the other buyers, and what they are willing to pa ...

... ECON 160 Spring 2011 Week 05 Classnotes February 22-24, 2011 (Chapter 5) 1. Market Demand determines Price : As you look at all the goods available to be purchased, the food, the clothing, the cars, etc. the price you have to pay is determined by all the other buyers, and what they are willing to pa ...

Demand Supply Increase Indeterminate

... original equilibrium quantity. Buyers want to buy more and sellers want to sell more. The quantity increases. What about price? In this little illustration, the new equilibrium price happens to be unchanged at Po, the original equilibrium price. Maintaining the same equilibrium price, however, is me ...

... original equilibrium quantity. Buyers want to buy more and sellers want to sell more. The quantity increases. What about price? In this little illustration, the new equilibrium price happens to be unchanged at Po, the original equilibrium price. Maintaining the same equilibrium price, however, is me ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑