AP Econ Midterm Review 2016

... o Inferior good: demand decreases as income increases Prices of related goods (substitutes and complements) ...

... o Inferior good: demand decreases as income increases Prices of related goods (substitutes and complements) ...

Managerial Economics in a Global Economy

... by an individual per time period PX = price per unit of commodity X I = consumer’s income PY = price of related (substitute or complementary) commodity T = tastes of the consumer ...

... by an individual per time period PX = price per unit of commodity X I = consumer’s income PY = price of related (substitute or complementary) commodity T = tastes of the consumer ...

1 - BrainMass

... A. Is really no different from a marginal cost curve. B. Shows the decrease in unit cost as more of the same product is produced over time. C. Calculates average cost at a particular point in time. D. None of the above 6. The distinction between sunk and incremental costs is most helpful in answerin ...

... A. Is really no different from a marginal cost curve. B. Shows the decrease in unit cost as more of the same product is produced over time. C. Calculates average cost at a particular point in time. D. None of the above 6. The distinction between sunk and incremental costs is most helpful in answerin ...

PRICE DETERMINATION IN MARKETS

... People come to believe that eating apples is good for them. The more apples they eat, the more likely they are to stay well. What is the effect on the market for ...

... People come to believe that eating apples is good for them. The more apples they eat, the more likely they are to stay well. What is the effect on the market for ...

Week 2 Questionnaire Choose any good form table below that you

... increase or decrease as a result of change in price? Would the revenue for your chosen good increase or decrease in response to the increase in price? Would you spend more or less on your good if price increased (relate that to the change of the quantity your of the good you’d purchase). This is ano ...

... increase or decrease as a result of change in price? Would the revenue for your chosen good increase or decrease in response to the increase in price? Would you spend more or less on your good if price increased (relate that to the change of the quantity your of the good you’d purchase). This is ano ...

advanced placement microeconomics

... Class preparation and participation are extremely important. The classroom is a place of mutual respect with learning as our goal. Students are expected to model such respect and encouragement. Incomplete or late assignments will be severely penalized. If a student is absent on the day an assignment ...

... Class preparation and participation are extremely important. The classroom is a place of mutual respect with learning as our goal. Students are expected to model such respect and encouragement. Incomplete or late assignments will be severely penalized. If a student is absent on the day an assignment ...

Demand - NSocialStudies

... “The price will settle at the point where the number of dogs for sale exactly matches the number of dogs that consumers want to buy. If there are more potential pet owners than dogs available, then the price of dogs will go up. Some consumers will then decide to buy ferrets instead and some pet shop ...

... “The price will settle at the point where the number of dogs for sale exactly matches the number of dogs that consumers want to buy. If there are more potential pet owners than dogs available, then the price of dogs will go up. Some consumers will then decide to buy ferrets instead and some pet shop ...

ECON 201 – Honors Macro Principles Spring 2013 Answers to

... of production, expected future price, the price of alternative output, and the number of suppliers. An improvement (retardation) in technology increases (decreases) supply; an increase (decrease) in the price of an input decreases (increases) supply; an increase (decrease) in expected future price w ...

... of production, expected future price, the price of alternative output, and the number of suppliers. An improvement (retardation) in technology increases (decreases) supply; an increase (decrease) in the price of an input decreases (increases) supply; an increase (decrease) in expected future price w ...

Economics and Entrepreneurship Test – II

... For questions 1 – 8, choose one word from the box below that best fits the sentence. You will not use all the words, so don’t worry if you have words left over. ...

... For questions 1 – 8, choose one word from the box below that best fits the sentence. You will not use all the words, so don’t worry if you have words left over. ...

Notes for Chapter 3 - FIU Faculty Websites

... Only one price and one quantity are compatible with the existing intentions of both buyers and sellers. In other words, there exist only one price where both quantity demanded is equal to quantity supplied. Invisible hand Adam Smith in The Wealth of Nations (1776) explained that market mechanisms wi ...

... Only one price and one quantity are compatible with the existing intentions of both buyers and sellers. In other words, there exist only one price where both quantity demanded is equal to quantity supplied. Invisible hand Adam Smith in The Wealth of Nations (1776) explained that market mechanisms wi ...

Economic Survey

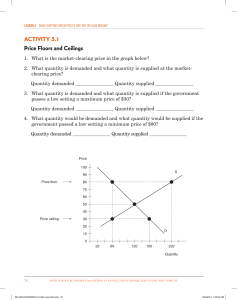

... Chapter 6 exam – Prices 1. In a free market, if the minimum wage is set below the market equilibrium wage rate, a) it will have no effect on employment. b) the result is an increase in unemployment. c) employers will find many workers willing to accept the lower wage. d) the result is a decrease in ...

... Chapter 6 exam – Prices 1. In a free market, if the minimum wage is set below the market equilibrium wage rate, a) it will have no effect on employment. b) the result is an increase in unemployment. c) employers will find many workers willing to accept the lower wage. d) the result is a decrease in ...

Economic Rent - WordPress.com

... The demand for land depends on its MRP The rent that will paid for land depends on its marginal rate of productivity (MRP) MRP in return is related to the selling price of the finished good. Therefore, we can conclude that the selling price of the good will determine the rent to be paid for the l ...

... The demand for land depends on its MRP The rent that will paid for land depends on its marginal rate of productivity (MRP) MRP in return is related to the selling price of the finished good. Therefore, we can conclude that the selling price of the good will determine the rent to be paid for the l ...

Price ($ per tonnes)

... the same soft drink for the same price, some people might buy from one machine and some from the other. However, if one machine's price is higher than the other, by even a small amount, the quantity demanded will drop to zero. The demand for a good that has a perfect substitute is perfectly elastic. ...

... the same soft drink for the same price, some people might buy from one machine and some from the other. However, if one machine's price is higher than the other, by even a small amount, the quantity demanded will drop to zero. The demand for a good that has a perfect substitute is perfectly elastic. ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑