Power Point

... Supply and Elasticity Supply is elastic when a small price change leads to a big change in quantity supplied Supply is inelastic when a big price change still has little effect on quantity supplied ...

... Supply and Elasticity Supply is elastic when a small price change leads to a big change in quantity supplied Supply is inelastic when a big price change still has little effect on quantity supplied ...

Chapter 3 The Concept of Elasticity and Consumer and Producer

... price is charged. It is also likely to be one for which a lower price will not induce substantially greater consumption. Thus, as price changes there is very little change in consumption, i.e. demand is inelastic and the demand curve is steep. • Inexpensive goods that take up little of your income c ...

... price is charged. It is also likely to be one for which a lower price will not induce substantially greater consumption. Thus, as price changes there is very little change in consumption, i.e. demand is inelastic and the demand curve is steep. • Inexpensive goods that take up little of your income c ...

Supply - Social Studies

... More the selling price increased, the more willing producers were to produce more of a good/service. (this is law of supply – why not supply more when you make more per item?) ...

... More the selling price increased, the more willing producers were to produce more of a good/service. (this is law of supply – why not supply more when you make more per item?) ...

Chapter 4 Demand_only

... Demand Curve shifts ◦ Price of complement increases, then demand for “GIQ” shifts in as total cost of consumption has increased ◦ Price of complement decreases, then demand for “GIQ” shifts out as total cost of consumption has decreased ◦ For complements: total cost of consumption matters! ...

... Demand Curve shifts ◦ Price of complement increases, then demand for “GIQ” shifts in as total cost of consumption has increased ◦ Price of complement decreases, then demand for “GIQ” shifts out as total cost of consumption has decreased ◦ For complements: total cost of consumption matters! ...

CHAPTER 3

... good by consumers and the price of the good. • The relationship between demand and price can be represented in different ways: in words, in a diagram or by using algebra. • We express this relationship in words as follows: the lower the price, the greater the quantity demanded. • We can also express ...

... good by consumers and the price of the good. • The relationship between demand and price can be represented in different ways: in words, in a diagram or by using algebra. • We express this relationship in words as follows: the lower the price, the greater the quantity demanded. • We can also express ...

The Short-run Condition For Profit Maximization

... The Invisible Hand Why are competitive markets attractive from the perspective of society as a whole? Price is equal to Marginal Cost (P=MC) • The last unit of output consumed is worth exactly the same to the buyer as the resources required to produce it, i.e. no gouging of consumers by firms. ...

... The Invisible Hand Why are competitive markets attractive from the perspective of society as a whole? Price is equal to Marginal Cost (P=MC) • The last unit of output consumed is worth exactly the same to the buyer as the resources required to produce it, i.e. no gouging of consumers by firms. ...

Price elasticity of Demand PowerPoint

... • Price elasticity of demand is a measure of how much the quantity demanded of a good responds to a change in the price of that good. • Price elasticity of demand is the percentage change in quantity demanded given a percent change in the price. ...

... • Price elasticity of demand is a measure of how much the quantity demanded of a good responds to a change in the price of that good. • Price elasticity of demand is the percentage change in quantity demanded given a percent change in the price. ...

CH. 3 STUDY GUIDE - BONUS TASKS

... shift of the supply curve. If the price of the goods that they sell is expected to fall in the future, sellers will want to sell more now; this increases supply and shifts the supply curve to the right. Taxes imposed by the government raise firms’ costs of production and, like increases in input pri ...

... shift of the supply curve. If the price of the goods that they sell is expected to fall in the future, sellers will want to sell more now; this increases supply and shifts the supply curve to the right. Taxes imposed by the government raise firms’ costs of production and, like increases in input pri ...

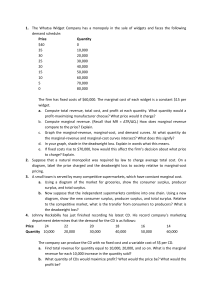

The Whatsa Widget Company has a monopoly in the sale of widgets

... a. Using a diagram of the market for groceries, show the consumer surplus, producer surplus, and total surplus. b. Now suppose that the independent supermarkets combine into one chain. Using a new diagram, show the new consumer surplus, producer surplus, and total surplus. Relative to the competitiv ...

... a. Using a diagram of the market for groceries, show the consumer surplus, producer surplus, and total surplus. b. Now suppose that the independent supermarkets combine into one chain. Using a new diagram, show the new consumer surplus, producer surplus, and total surplus. Relative to the competitiv ...

non-price determinants of - College of Business Administration

... monopoly is a market with one seller (monopsony is a market with one buyer). The monopolist profit maximizes by controlling its quantity supplied to the quantity underneath MR = MC. There are four steps. Step 1, find MR = MC; step 2, drop to the X-axis and set Qπ max; step 3, rise to the demand curv ...

... monopoly is a market with one seller (monopsony is a market with one buyer). The monopolist profit maximizes by controlling its quantity supplied to the quantity underneath MR = MC. There are four steps. Step 1, find MR = MC; step 2, drop to the X-axis and set Qπ max; step 3, rise to the demand curv ...

Ch06 my ppt

... The perfectly competitive firm’s supply curve is its marginal cost curve Every quantity of output along the market supply represents the summation of all the quantities individual sellers offer at the corresponding price At every point along the market supply curve, price measures what it would cost ...

... The perfectly competitive firm’s supply curve is its marginal cost curve Every quantity of output along the market supply represents the summation of all the quantities individual sellers offer at the corresponding price At every point along the market supply curve, price measures what it would cost ...

Week 2

... If the interest rate is 7% and cash flows are $4,000 at the end of year one and $6,000 at the end of year two, then the present value of these cash flows is ...

... If the interest rate is 7% and cash flows are $4,000 at the end of year one and $6,000 at the end of year two, then the present value of these cash flows is ...

Handout #9

... monopolist can set price differently for every unit of goods sold. Recall that, for a single monopoly, marginal revenue (MR) is less than price since when the price is cut in order to sell a larger quantity, the price is lower on all units sold. However, for the first-degree price discrimination, MR ...

... monopolist can set price differently for every unit of goods sold. Recall that, for a single monopoly, marginal revenue (MR) is less than price since when the price is cut in order to sell a larger quantity, the price is lower on all units sold. However, for the first-degree price discrimination, MR ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑