chap008 - QC Economics

... • The market supply curve determines the equilibrium price faced by an individual producer. – Equilibrium price – The price at which the quantity of a good demanded in a given time period equals the quantity supplied. – Market supply – The total quantities of a good that sellers are willing and able ...

... • The market supply curve determines the equilibrium price faced by an individual producer. – Equilibrium price – The price at which the quantity of a good demanded in a given time period equals the quantity supplied. – Market supply – The total quantities of a good that sellers are willing and able ...

PDF

... perhaps others, may be included. For a short run study of demand, only the price variables might be included. An underlying reason for the reduced number of variables in the short run analysis is that the variables income, population, and tastes and preferences may be assumed constant during relativ ...

... perhaps others, may be included. For a short run study of demand, only the price variables might be included. An underlying reason for the reduced number of variables in the short run analysis is that the variables income, population, and tastes and preferences may be assumed constant during relativ ...

Lecture slides Chap 1-4 - University of Victoria

... • We will often take it as constant. • Fixed cost + constant marginal cost economies of scale ...

... • We will often take it as constant. • Fixed cost + constant marginal cost economies of scale ...

47-800 - Andrew.cmu.edu

... price effects are strictly negative. A commodity for which the price effects are sometimes strictly positive is called a Giffen good, otherwise the commodity is an ordinary good. We have some relationships between the wealth and price effects. Since x(p, w) is HD0, for all α > 0 we have x(αp, αw) − ...

... price effects are strictly negative. A commodity for which the price effects are sometimes strictly positive is called a Giffen good, otherwise the commodity is an ordinary good. We have some relationships between the wealth and price effects. Since x(p, w) is HD0, for all α > 0 we have x(αp, αw) − ...

Ch 24

... The Demand Curve a Monopolist Faces (cont'd) • Perfect competition versus monopoly – The perfect competitor doesn’t have to worry about lowering price to sell more – In a purely competitive situation, the firm accounts for a small part of the market • It can sell its entire output, whatever that ma ...

... The Demand Curve a Monopolist Faces (cont'd) • Perfect competition versus monopoly – The perfect competitor doesn’t have to worry about lowering price to sell more – In a purely competitive situation, the firm accounts for a small part of the market • It can sell its entire output, whatever that ma ...

Lecture notes

... Salvatore: International Economics, 10th Edition © 2010 John Wiley & Sons, Inc. ...

... Salvatore: International Economics, 10th Edition © 2010 John Wiley & Sons, Inc. ...

Scarcity and Choice

... The Income Effect A. A change in price affects consumers’ real income. B. This change in real income affects the consumer’s ability to buy all sorts of products, not just the one for which the price changed. C. Demand for all normal goods will increase when the price of any other good goes down (and ...

... The Income Effect A. A change in price affects consumers’ real income. B. This change in real income affects the consumer’s ability to buy all sorts of products, not just the one for which the price changed. C. Demand for all normal goods will increase when the price of any other good goes down (and ...

Product Differentiation, Collusion, and Empirical Analyses of Market

... (1992), Rothschild (1992, 1997), and Häckner (1994, 1995), among others have adapted Friedman’s supergame equilibrium concept to the study of collusion to illustrate how product di¤erentiation impacts price competition and ultimately the incentives to form non-cooperative agreements in oligopoly mod ...

... (1992), Rothschild (1992, 1997), and Häckner (1994, 1995), among others have adapted Friedman’s supergame equilibrium concept to the study of collusion to illustrate how product di¤erentiation impacts price competition and ultimately the incentives to form non-cooperative agreements in oligopoly mod ...

Portfolio diversification and internalization of production externalities through majority voting Hervé Crès

... of research reinforces the hope that super majority voting can lead to an efficient allocation of public goods. In the present paper, we address the problem of managing production externalities. Externalities are ordinary public goods. If there is no market mechanism to internalize them, then sharehol ...

... of research reinforces the hope that super majority voting can lead to an efficient allocation of public goods. In the present paper, we address the problem of managing production externalities. Externalities are ordinary public goods. If there is no market mechanism to internalize them, then sharehol ...

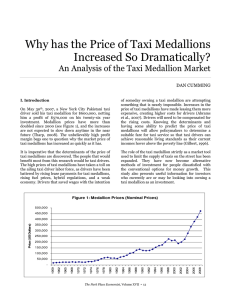

P M.

... For water, the price is low, total utility is large, and marginal utility is small. For diamonds, the price is high, total utility is small, and marginal utility is high. But marginal utility per dollar is the same for water and diamonds. ...

... For water, the price is low, total utility is large, and marginal utility is small. For diamonds, the price is high, total utility is small, and marginal utility is high. But marginal utility per dollar is the same for water and diamonds. ...

Principles of Economics, Case and Fair,9e

... At every level of output except 1 unit, a monopolist’s marginal revenue (MR) is below price. This is so because (1) we assume that the monopolist must sell all its product at a single price (no price discrimination) and (2) to raise output and sell it, the firm must lower the price it charges. Selli ...

... At every level of output except 1 unit, a monopolist’s marginal revenue (MR) is below price. This is so because (1) we assume that the monopolist must sell all its product at a single price (no price discrimination) and (2) to raise output and sell it, the firm must lower the price it charges. Selli ...

Introduction Economics Today

... – The more successful it is at differentiation, the more control it has over price Slide 25-11 ...

... – The more successful it is at differentiation, the more control it has over price Slide 25-11 ...

Income Differences and Prices of Tradables

... incomes. Hsieh and Klenow (2007) demonstrate that this relationship is particularly pronounced among tradable consumption goods. Since these goods comprise consumption bundles of individuals and their prices directly affect consumer welfare, it is of central importance to understand the underlying m ...

... incomes. Hsieh and Klenow (2007) demonstrate that this relationship is particularly pronounced among tradable consumption goods. Since these goods comprise consumption bundles of individuals and their prices directly affect consumer welfare, it is of central importance to understand the underlying m ...

Introduction to Microeconomics II OEC 107

... that throughout this course unit, we will be using some concepts and theories that have been presented in the former course unit more often than not. Just like in the Introduction to Microeconomics part I (OEC 101), we wish to emphasize that all lectures contained in this reading material have been ...

... that throughout this course unit, we will be using some concepts and theories that have been presented in the former course unit more often than not. Just like in the Introduction to Microeconomics part I (OEC 101), we wish to emphasize that all lectures contained in this reading material have been ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑