Product Diversification and the MultiProduct Firm

... total number of units of output will remain net output cost of the xth product. The the same. In another case, when the intro- second expression from (15) states that for duction of an additional product reduces the optimality of the xth product, the x+ 1 prodsales of the previous products by an amo ...

... total number of units of output will remain net output cost of the xth product. The the same. In another case, when the intro- second expression from (15) states that for duction of an additional product reduces the optimality of the xth product, the x+ 1 prodsales of the previous products by an amo ...

The Art and Science of Economics

... quantity of one good consumed and the quantity of another consumed ...

... quantity of one good consumed and the quantity of another consumed ...

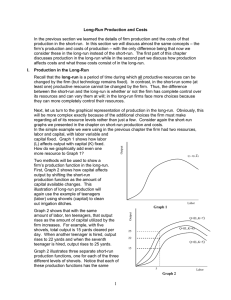

Long-Run Production and Costs

... Now it becomes clearer which of these three methods will the firm prefer to use. First note that the firm’s total revenue is the same regardless of the method used because in each the firm produces the same level of output. Hence, a profit maximizing firm would choose method 3 because costs of produ ...

... Now it becomes clearer which of these three methods will the firm prefer to use. First note that the firm’s total revenue is the same regardless of the method used because in each the firm produces the same level of output. Hence, a profit maximizing firm would choose method 3 because costs of produ ...

Chapter 6 CONSUMER CHOICE: INDIVIDUAL AND MARKET

... ● Using Marginal Utility: The Optimal Purchase Rule ♦ Buy the quantity of each good at which price and marginal utility are exactly equal. ♦ If marginal utility is greater (less) than price, the consumer can improve well being by purchasing more (less). ...

... ● Using Marginal Utility: The Optimal Purchase Rule ♦ Buy the quantity of each good at which price and marginal utility are exactly equal. ♦ If marginal utility is greater (less) than price, the consumer can improve well being by purchasing more (less). ...

Income effect - McGraw Hill Higher Education - McGraw

... consumer welfare, whether through demand curves or cost-of-living indexes • Economists find it useful to dissect the effects of a price change into one that depends only on the change in purchasing power (income effect) and one that depends only on the changes in relative price (substitution effect) ...

... consumer welfare, whether through demand curves or cost-of-living indexes • Economists find it useful to dissect the effects of a price change into one that depends only on the change in purchasing power (income effect) and one that depends only on the changes in relative price (substitution effect) ...

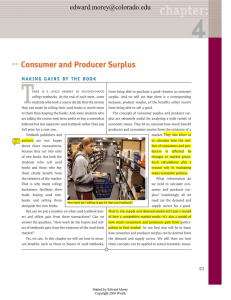

Consumer and Producer Surplus - University of Colorado Boulder

... and sellers benefit from a competitive market and how big those benefits are. In addi tion, these concepts play important roles in analyzing what happens when competitive markets don't work well or there is interference in the market. So let's begin by looking at the market for used textbooks, start ...

... and sellers benefit from a competitive market and how big those benefits are. In addi tion, these concepts play important roles in analyzing what happens when competitive markets don't work well or there is interference in the market. So let's begin by looking at the market for used textbooks, start ...

Lecture 04.2b

... • Decreased “specialization” or productivity of an input, e.g., labor – Less well-suited for production of this good ...

... • Decreased “specialization” or productivity of an input, e.g., labor – Less well-suited for production of this good ...

Supply And Demand

... The law of supply is accounted for by two factors: In the face of rising prices, firms arrange their activities to supply more of the good to the market, substituting production of that good for the production of other goods. Assuming firms' costs are constant, a higher price means ...

... The law of supply is accounted for by two factors: In the face of rising prices, firms arrange their activities to supply more of the good to the market, substituting production of that good for the production of other goods. Assuming firms' costs are constant, a higher price means ...

chap006Answers

... The distinction can be made because there are some costs that do not vary with total output. These are the fixed costs that, fundamentally, are related to the scale or size of the plant. In the short run, by definition, the scale of the plant cannot change: The firm cannot bring in more machinery or ...

... The distinction can be made because there are some costs that do not vary with total output. These are the fixed costs that, fundamentally, are related to the scale or size of the plant. In the short run, by definition, the scale of the plant cannot change: The firm cannot bring in more machinery or ...

Chapter 29 - The Citadel

... goods are produced and services are performed in those countries where the opportunity costs are lowest, then global economic growth is enhanced. ...

... goods are produced and services are performed in those countries where the opportunity costs are lowest, then global economic growth is enhanced. ...

PDF

... Perhaps the major limitation of the Raunikar et that all consumers face the same prices at a given al. study was its dependence on quantity data point in time. This assumption is invalidated to from a localized panel of households. There is a some extent by the existence of regional price concern ab ...

... Perhaps the major limitation of the Raunikar et that all consumers face the same prices at a given al. study was its dependence on quantity data point in time. This assumption is invalidated to from a localized panel of households. There is a some extent by the existence of regional price concern ab ...

Chapter 2 Models of Economic Systems

... will suppose that X ⊂ R+N and call it consumption set. The elements of X are called consumption bundles. Excepted this physical constraints on consumer’s consumption set there are economic constraints which consumer must consider in making his optimal decisions. The most important economic constrain ...

... will suppose that X ⊂ R+N and call it consumption set. The elements of X are called consumption bundles. Excepted this physical constraints on consumer’s consumption set there are economic constraints which consumer must consider in making his optimal decisions. The most important economic constrain ...

Ch10

... Because firms are trying to maximize their profits, they try to make the difference between total revenue and total cost as large as possible. The attractiveness of a resource, then, varies with what the resource can add to the revenues received by the firm relative to what it adds to costs. ...

... Because firms are trying to maximize their profits, they try to make the difference between total revenue and total cost as large as possible. The attractiveness of a resource, then, varies with what the resource can add to the revenues received by the firm relative to what it adds to costs. ...

Chapter 3 The Concept of Elasticity and Consumer and Producer

... • With a linear demand curve (meaning a demand curve that has a single value for the slope) elasticity is greater at higher prices ...

... • With a linear demand curve (meaning a demand curve that has a single value for the slope) elasticity is greater at higher prices ...

Distribution channel choice in a market with complementary goods

... scope; that is, selling higher volumes implies lower unit costs of distribution. Further, using an independent distributor may imply access to a lower distribution cost function than if a manufacturer distributed his product himself. We also consider the demand benefits offered through ‘one-stop sho ...

... scope; that is, selling higher volumes implies lower unit costs of distribution. Further, using an independent distributor may imply access to a lower distribution cost function than if a manufacturer distributed his product himself. We also consider the demand benefits offered through ‘one-stop sho ...

Quantity Discounts and Capital Misallocation in Vertical Relationships

... Another important literature that the paper contributes to is the literature on non-linear pricing and vertical relationships. The screening aspect of the non-linear pricing has been extensively studied. Stole (1995) shows that second degree price discrimination is sustainable even in a multifirm set ...

... Another important literature that the paper contributes to is the literature on non-linear pricing and vertical relationships. The screening aspect of the non-linear pricing has been extensively studied. Stole (1995) shows that second degree price discrimination is sustainable even in a multifirm set ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.