Market Equilibrium and Applications

... D. in the short-run, the monopoly will produce such that P > MC while perfectly competitive firms will produce such that P = MC. E. in the long-run monopolies can sustain positive economic profits while perfectly competitive firms cannot. 6. Price discrimination: A. tends to decrease the allocative ...

... D. in the short-run, the monopoly will produce such that P > MC while perfectly competitive firms will produce such that P = MC. E. in the long-run monopolies can sustain positive economic profits while perfectly competitive firms cannot. 6. Price discrimination: A. tends to decrease the allocative ...

SampleMidterm.pdf

... [3] PRINT your name clearly, and write your precept day and time, on the first page of EACH answer book you use. [4] Do not start writing answers until you are told you can. From that point, you have 80 minutes. Therefore you should plan to spend roughly 20 minutes on each question. At the end of th ...

... [3] PRINT your name clearly, and write your precept day and time, on the first page of EACH answer book you use. [4] Do not start writing answers until you are told you can. From that point, you have 80 minutes. Therefore you should plan to spend roughly 20 minutes on each question. At the end of th ...

Monopoly_Ch10

... – A monopoly exists because a single large firm has lower costs than any potential competitor – In addition, breaking up the firm into multiple competitors may increase costs as well ...

... – A monopoly exists because a single large firm has lower costs than any potential competitor – In addition, breaking up the firm into multiple competitors may increase costs as well ...

LECTURE 12: COMPETITIVE MARKETS A MARKET consists of all

... perfect knowledge as to present and future prices, costs, and economic opportunities in general. Thus, consumers will not pay a higher price than necessary for the product. Price differences are quickly eliminated, and a single price will prevail throughout the market for the product. Perfect compet ...

... perfect knowledge as to present and future prices, costs, and economic opportunities in general. Thus, consumers will not pay a higher price than necessary for the product. Price differences are quickly eliminated, and a single price will prevail throughout the market for the product. Perfect compet ...

CONTENT TEACHING OUTLINE Unit D: Marketing a Small

... (1) A product is said to have elastic demand if demand for the product is sensitive to a change in price. Such products tend to be non-essential products such as entertainment, specialty foods, and fashion. (2) A product is said to have inelastic demand if demand for the product is not sensitive to ...

... (1) A product is said to have elastic demand if demand for the product is sensitive to a change in price. Such products tend to be non-essential products such as entertainment, specialty foods, and fashion. (2) A product is said to have inelastic demand if demand for the product is not sensitive to ...

Ch.8

... – Quantity of output - all sellers in a market will produce at different prices – Add up the quantities of output supplied by all firms in the market at each price ...

... – Quantity of output - all sellers in a market will produce at different prices – Add up the quantities of output supplied by all firms in the market at each price ...

Intermediate Microeconomics – II

... incentive to undercut. The following discusses a situation where price competition does not lead to marginal cost pricing. Consider the following simplified model, where two firms take part in a twostage game. In the first stage, firms build capacity K1,K2 simultaneously. In the second stage (first ...

... incentive to undercut. The following discusses a situation where price competition does not lead to marginal cost pricing. Consider the following simplified model, where two firms take part in a twostage game. In the first stage, firms build capacity K1,K2 simultaneously. In the second stage (first ...

ECON308: Monopoly = Price Searcher

... Firms in the MOST competitive market (D4) are called price-takers and have no market power. 1. All firms that are not in perfectly competitive markets face a downward sloping demand curve. We can then use the (monopoly model = Price Searcher) to represent the pricing behavior and production decision ...

... Firms in the MOST competitive market (D4) are called price-takers and have no market power. 1. All firms that are not in perfectly competitive markets face a downward sloping demand curve. We can then use the (monopoly model = Price Searcher) to represent the pricing behavior and production decision ...

SAMPLE QUESTIONS : INTRODUCTORY MICROECONOMICS

... SAMPLE QUESTIONS: INTRODUCTORY MICROECONOMICS ...

... SAMPLE QUESTIONS: INTRODUCTORY MICROECONOMICS ...

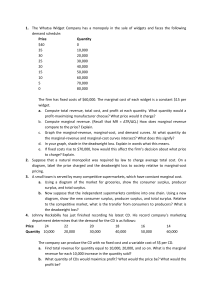

The Whatsa Widget Company has a monopoly in the sale of widgets

... the marginal-revenue and marginal-cost curves intersect? What does this signify? d. In your graph, shade in the deadweight loss. Explain in words what this means. e. If fixed costs rise to $70,000, how would this affect the firm’s decision about what price to charge? Explain. 2. Suppose that a natur ...

... the marginal-revenue and marginal-cost curves intersect? What does this signify? d. In your graph, shade in the deadweight loss. Explain in words what this means. e. If fixed costs rise to $70,000, how would this affect the firm’s decision about what price to charge? Explain. 2. Suppose that a natur ...

Economics and Entrepreneurship Test – II

... Economics and Entrepreneurship Test – II For questions 1 – 8, choose one word from the box below that best fits the sentence. You will not use all the words, so don’t worry if you have words left over. ...

... Economics and Entrepreneurship Test – II For questions 1 – 8, choose one word from the box below that best fits the sentence. You will not use all the words, so don’t worry if you have words left over. ...

Chapter Outline

... just breaks even. If the demand shifts below the break-even point (including a normal profit), some firms will leave the industry in the long run. 2. If firms were making a loss in the short run, some firms will leave the industry. This will raise the demand curve facing each remaining firm as there ...

... just breaks even. If the demand shifts below the break-even point (including a normal profit), some firms will leave the industry in the long run. 2. If firms were making a loss in the short run, some firms will leave the industry. This will raise the demand curve facing each remaining firm as there ...

Economics Holiday Homework - Kendriya Vidyalaya No.1 Devlali

... 12. Explain how the demand for a good is affected by the prices of its related goods. Give examples. 13. Derive the law of demand from the single commodity equilibrium condition “marginal utility =price”. Or Derive the inverse relation between price of a good and its demand from the single commodity ...

... 12. Explain how the demand for a good is affected by the prices of its related goods. Give examples. 13. Derive the law of demand from the single commodity equilibrium condition “marginal utility =price”. Or Derive the inverse relation between price of a good and its demand from the single commodity ...

Lecture2.monopoly

... B and C are lost from CS and PS A is transferred from PS to CS ΔCS = +A –B (could be gain or loss) ΔPS = -A –C (loss) Δoverall economic welfare = -B –C Even this calculation assumes that it is those who value the good most who consume the reduced ...

... B and C are lost from CS and PS A is transferred from PS to CS ΔCS = +A –B (could be gain or loss) ΔPS = -A –C (loss) Δoverall economic welfare = -B –C Even this calculation assumes that it is those who value the good most who consume the reduced ...

2A Task 1 Markets and prices Marking guide 2011

... Homogeneous products. Firms are price makers. Easy entry conditions. ...

... Homogeneous products. Firms are price makers. Easy entry conditions. ...

Econ 1 UT2 F16 - Bakersfield College

... a. only in the short-run. b. only in the long-run. c. in both the short-run and the long-run. d. in neither the short-run nor the long-run. 12. For a firm in perfect competition, the owner has real control which of the following? a. Both the price he charges and the quantity of product he makes. b. ...

... a. only in the short-run. b. only in the long-run. c. in both the short-run and the long-run. d. in neither the short-run nor the long-run. 12. For a firm in perfect competition, the owner has real control which of the following? a. Both the price he charges and the quantity of product he makes. b. ...

econ - Homework Market

... C. continue growing soy beans only if the new price covers average fixed costs. D. continue growing soy beans only if the new price covers average variable costs. E. continue growing soy beans only if the new price covers average total costs. 24. Individual firms in a purely competitive industry do ...

... C. continue growing soy beans only if the new price covers average fixed costs. D. continue growing soy beans only if the new price covers average variable costs. E. continue growing soy beans only if the new price covers average total costs. 24. Individual firms in a purely competitive industry do ...

ANSWERS PS#2 - Economics 352

... c) Since monopolists produce less than what would be produced under competitive conditions, monopolists create shortages. ANS: False. At PSM all the units demanded, XSM, are supplied, so there is no shortage. d) Monopolists will never earn zero economic profit since entry does not force profits down ...

... c) Since monopolists produce less than what would be produced under competitive conditions, monopolists create shortages. ANS: False. At PSM all the units demanded, XSM, are supplied, so there is no shortage. d) Monopolists will never earn zero economic profit since entry does not force profits down ...

P 1

... In competitive price-taker markets, firms a. can sell all of their output at the market price. b. produce differentiated products. c. can influence the market price by altering their output level. d. are large relative to the total market. When we say that a firm is a price taker, we are indicatin ...

... In competitive price-taker markets, firms a. can sell all of their output at the market price. b. produce differentiated products. c. can influence the market price by altering their output level. d. are large relative to the total market. When we say that a firm is a price taker, we are indicatin ...