6-2: Prices as Signals and Incentives

... exceed a certain level ◦ This leads to a shortage of rental properties ◦ Often these rental properties are not well-maintained due to the fact that the rent cannot go above a certain point ...

... exceed a certain level ◦ This leads to a shortage of rental properties ◦ Often these rental properties are not well-maintained due to the fact that the rent cannot go above a certain point ...

Schiller, Ch - GEOCITIES.ws

... The key questions addressed in this chapter are: How much output can a firm produce? How do the costs of production vary with the rate of output? Do larger firms have a cost advantage over smaller firms? THE PRODUCTION FUNCTION Factors of production – Resource inputs used to produce goods and servic ...

... The key questions addressed in this chapter are: How much output can a firm produce? How do the costs of production vary with the rate of output? Do larger firms have a cost advantage over smaller firms? THE PRODUCTION FUNCTION Factors of production – Resource inputs used to produce goods and servic ...

Ahliman Abbasov Microeconomic (qrup 1061) Draw a demand

... power. 60) Explain how will the monopolistic firm decide on the profit maximizing production quantity? 61) Explain the welfare costs of monopolies to the society. 62) Indicate the public policy alternatives that governments may use to deal with monopolies. 63) Discuss price discrimination and its ef ...

... power. 60) Explain how will the monopolistic firm decide on the profit maximizing production quantity? 61) Explain the welfare costs of monopolies to the society. 62) Indicate the public policy alternatives that governments may use to deal with monopolies. 63) Discuss price discrimination and its ef ...

PROBLEMS

... In a monopoly market, the monopolist produces at the point where MC=MR. In this case, MC = MR at 50 cans per day, thus students would pay $1.50 per can. ...

... In a monopoly market, the monopolist produces at the point where MC=MR. In this case, MC = MR at 50 cans per day, thus students would pay $1.50 per can. ...

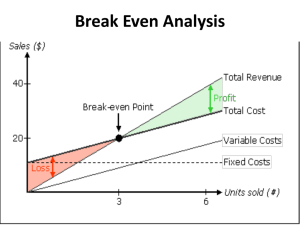

10a. Break Even Analysis

... price at which to sell a product or service • Marketers will play with different prices in order to see how many sales need to be made in order to make the companies cover all of their costs • In order to calculate the Break-Even Analysis – Need to know Variable Costs (VC) & Fixed Costs (FC) ...

... price at which to sell a product or service • Marketers will play with different prices in order to see how many sales need to be made in order to make the companies cover all of their costs • In order to calculate the Break-Even Analysis – Need to know Variable Costs (VC) & Fixed Costs (FC) ...

MIDTERM EXAMINATION 1

... The own price elasticity of apples is –0.8 and the cross elasticity of apples with respect to the price of oranges is 0.5. Suppose that the price of apples rises by 10 percent and the price of oranges falls by 4 percent. What will happen to apple demand? a. a 10 percent increase. b.* a 10 percent de ...

... The own price elasticity of apples is –0.8 and the cross elasticity of apples with respect to the price of oranges is 0.5. Suppose that the price of apples rises by 10 percent and the price of oranges falls by 4 percent. What will happen to apple demand? a. a 10 percent increase. b.* a 10 percent de ...

Chapter 5: Supply Section 1

... producers of a good. • Subsidies generally lower cost, which allows a firm to produce more goods. • Reasons for subsidizing products include: – To provide for people during food shortages – To protect young industries from foreign competition. ...

... producers of a good. • Subsidies generally lower cost, which allows a firm to produce more goods. • Reasons for subsidizing products include: – To provide for people during food shortages – To protect young industries from foreign competition. ...

Supply and Demand

... producer is willing to sell – Quantity Supplied: the amount of a good or service producers are willing and able to offer for sale at a given price ...

... producer is willing to sell – Quantity Supplied: the amount of a good or service producers are willing and able to offer for sale at a given price ...

Chapter 6: Prices Section 1

... to solve a shortage. It reduces quantity demanded and only people who have enough money will be able to pay the higher prices. This will cause the market to settle at a new equilibrium. ...

... to solve a shortage. It reduces quantity demanded and only people who have enough money will be able to pay the higher prices. This will cause the market to settle at a new equilibrium. ...

Chapter 6 - How Firms Make Decisions: Profit Maximization

... This rule is very useful—allows us to look at a diagram of MC and MR curves and immediately identify profit-maximizing output level ...

... This rule is very useful—allows us to look at a diagram of MC and MR curves and immediately identify profit-maximizing output level ...

A professor hires two aides, assigning them the tasks of reading

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

... (C) The price will decrease. (D) Economic profits will increase. (E) Economic profits will decrease. 42. Assume a firm uses only two inputs, capital (K) and labor (L), to produce its output. Let the marginal product of capital be MPK, the marginal product of labor be MPL, the price of capital be PK, ...

Old Midterm Examinations With Answers

... plants, with high fixed costs, can spread the fixed costs over so many units that the cost per unit is lower than can possibly be achieved in smaller plants. 14. So many sellers that no one can affect the price; perfect information; easy entry and exit; identical products One seller with high barrie ...

... plants, with high fixed costs, can spread the fixed costs over so many units that the cost per unit is lower than can possibly be achieved in smaller plants. 14. So many sellers that no one can affect the price; perfect information; easy entry and exit; identical products One seller with high barrie ...

MBA Cph - factor markets

... where factor markets are competitive and only one factor (labour) is variable and the other factor (capital) is fixed ...

... where factor markets are competitive and only one factor (labour) is variable and the other factor (capital) is fixed ...

Economics: Principles and Applications, 2e by Robert E. Hall & Marc

... Competition Imperfect competition: market structures between perfect competition and monopoly • more than one seller, but too few to create a perfectly competitive market • often violate other conditions of perfect competition, such as the requirement of a standardized product or free entry and exit ...

... Competition Imperfect competition: market structures between perfect competition and monopoly • more than one seller, but too few to create a perfectly competitive market • often violate other conditions of perfect competition, such as the requirement of a standardized product or free entry and exit ...

Chapter_Nine_lecture

... The demand curve faced by an individual firm may be different from the demand curve for the industry as a whole. Market structure plays a central role in determining the efficiency of the market. In this chapter we focus on competitive market structures. ...

... The demand curve faced by an individual firm may be different from the demand curve for the industry as a whole. Market structure plays a central role in determining the efficiency of the market. In this chapter we focus on competitive market structures. ...

Slide 1

... the debate about globalization Most experts believe that while there is a trend towards global markets, cultural and economic differences among nations act as a major brake on any trend toward global consumer tastes and preferences In addition, trade barriers and differences in product and techn ...

... the debate about globalization Most experts believe that while there is a trend towards global markets, cultural and economic differences among nations act as a major brake on any trend toward global consumer tastes and preferences In addition, trade barriers and differences in product and techn ...