The State of Small Business Lending: Credit Access during the

... small business borrowers less creditworthy today. Small business credit scores are lower now than before the Great Recession. The Federal Reserve’s 2003 Survey of Small Business Finances indicated that the average PAYDEX score of those surveyed was 53.4. By contrast, the 2011 NFIB ...

... small business borrowers less creditworthy today. Small business credit scores are lower now than before the Great Recession. The Federal Reserve’s 2003 Survey of Small Business Finances indicated that the average PAYDEX score of those surveyed was 53.4. By contrast, the 2011 NFIB ...

PRESS RELEASE - Erste Group Bank AG

... Net interest income, which represents the most important income component, rose by 3% in 2016, from EUR 1.57 bn to EUR 1.62 bn. Commission income decreased by 5.7% from EUR 810 mn to EUR 764.2 mn. The bulk of this decrease was attributable to a revision of intra-group processes. On the customer side ...

... Net interest income, which represents the most important income component, rose by 3% in 2016, from EUR 1.57 bn to EUR 1.62 bn. Commission income decreased by 5.7% from EUR 810 mn to EUR 764.2 mn. The bulk of this decrease was attributable to a revision of intra-group processes. On the customer side ...

Regulatory impact assessment of Basel III capital requirements in New Zealand.

... medium term growth. Bank failures can have negative impacts over and above losses for the creditors and shareholders of banks. Banks are usually the major providers of financial intermediation services and they play a central role in transferring funds between parties through their position in payme ...

... medium term growth. Bank failures can have negative impacts over and above losses for the creditors and shareholders of banks. Banks are usually the major providers of financial intermediation services and they play a central role in transferring funds between parties through their position in payme ...

Have big banks gotten safer?

... the General Manager of the Bank for International Settlements, claim that properly risk-adjusted capital levels brought about by Basel III for systemically important financial institutions are seven times Basel II levels (Carney 2014, Caruana 2012). Policymakers and political commentators alike have ...

... the General Manager of the Bank for International Settlements, claim that properly risk-adjusted capital levels brought about by Basel III for systemically important financial institutions are seven times Basel II levels (Carney 2014, Caruana 2012). Policymakers and political commentators alike have ...

The Crisis Aftermath: New Regulatory Paradigms

... economic agents in the banking system and questioned the capacity of financial markets to channel resources to their best use. While it is essential for the well functioning of economic activity that financial institutions do take risk, the decisions taken by financial intermediaries have proven ex ...

... economic agents in the banking system and questioned the capacity of financial markets to channel resources to their best use. While it is essential for the well functioning of economic activity that financial institutions do take risk, the decisions taken by financial intermediaries have proven ex ...

Deregulation of Bank Entry and Bank Failures

... state deregulation. Our results suggest that at least using the bank failures till the period of enactment of the Regal-Neil Act of 1994, such moral hazard did not seem to affect banking sector fragility. These contrasting results are consistent with the effect of the regulation being greater in envi ...

... state deregulation. Our results suggest that at least using the bank failures till the period of enactment of the Regal-Neil Act of 1994, such moral hazard did not seem to affect banking sector fragility. These contrasting results are consistent with the effect of the regulation being greater in envi ...

Supervisory Strategy 2014-2018

... Although banks have undeniably taken measures to improve the situation, there is still a great deal of distrust. To recapture trust, banks must continue working on an ethical culture, sound remuneration policies and sustainable business models. What is more, in a climate of distrust no news is bad n ...

... Although banks have undeniably taken measures to improve the situation, there is still a great deal of distrust. To recapture trust, banks must continue working on an ethical culture, sound remuneration policies and sustainable business models. What is more, in a climate of distrust no news is bad n ...

1 Trends and developments in the Spanish

... expresses data. opinions or estimations regarding the date of issue of the report. prepared by BBVA or obtained from or based on sources we consider to be reliable. and have not been independently verified by BBVA. Therefore. BBVA offers no warranty. either express or implicit. regarding its accurac ...

... expresses data. opinions or estimations regarding the date of issue of the report. prepared by BBVA or obtained from or based on sources we consider to be reliable. and have not been independently verified by BBVA. Therefore. BBVA offers no warranty. either express or implicit. regarding its accurac ...

1) Which of the following statements are true

... Bank capital is listed on the _____ side of the bank’s balance sheet because it represents a _____ of funds. liability; use liability; source asset; use asset; source Question Status: Previous Edition Banks acquire funds from such sources as checkable deposits. savings accounts. reserves. all of the ...

... Bank capital is listed on the _____ side of the bank’s balance sheet because it represents a _____ of funds. liability; use liability; source asset; use asset; source Question Status: Previous Edition Banks acquire funds from such sources as checkable deposits. savings accounts. reserves. all of the ...

Bank leverage and monetary policy`s risk-taking - ECB

... provide evidence in support of a more causal interpretation of the link between interest rates, bank capital, and bank risk taking, in the sense that our findings are unlikely to be explained by monetary policy rates reacting to our measures of bank risk taking. The paper makes two important contrib ...

... provide evidence in support of a more causal interpretation of the link between interest rates, bank capital, and bank risk taking, in the sense that our findings are unlikely to be explained by monetary policy rates reacting to our measures of bank risk taking. The paper makes two important contrib ...

Regulatory Constraints on Leverage: The

... The regulatory measure of leverage in Canada is the ratio of total balance sheet assets and certain off-balance-sheet items to total regulatory capital (adjusted net Tier 1 and Tier 2 capital).3 The off-balance-sheet items include all direct contractual exposures to credit risk—including letters of ...

... The regulatory measure of leverage in Canada is the ratio of total balance sheet assets and certain off-balance-sheet items to total regulatory capital (adjusted net Tier 1 and Tier 2 capital).3 The off-balance-sheet items include all direct contractual exposures to credit risk—including letters of ...

Sovereign Money in Critical Context PDF

... The typical case in point is banking regulation according to Basel III (bank equity and liquidity requirements in relation to various classes of assets and liabilities). Basel III supporters believe that implementing such higher requirements would solve the problem.9 However, one has good reason to ...

... The typical case in point is banking regulation according to Basel III (bank equity and liquidity requirements in relation to various classes of assets and liabilities). Basel III supporters believe that implementing such higher requirements would solve the problem.9 However, one has good reason to ...

2013 - Central Bank of Sri Lanka

... The Banking sector continued to be resilient in a challenging environment. The soundness of the sector was reflected by the satisfactory levels of liquidity and capital maintained by the sector. The strengthening of the regulatory and supervisory framework for banks and the enhanced risk management ...

... The Banking sector continued to be resilient in a challenging environment. The soundness of the sector was reflected by the satisfactory levels of liquidity and capital maintained by the sector. The strengthening of the regulatory and supervisory framework for banks and the enhanced risk management ...

Documentation - APEC SME Crisis Management Center

... It is more difficult for them to get finance, especially from risk averse lenders (eg banks) who might actually have the funds, but are not as effective at mobilising them; even though there are entrepreneurial opportunities arising from restructuring and bankruptcy/exits, a generation of growth ori ...

... It is more difficult for them to get finance, especially from risk averse lenders (eg banks) who might actually have the funds, but are not as effective at mobilising them; even though there are entrepreneurial opportunities arising from restructuring and bankruptcy/exits, a generation of growth ori ...

Fundamentals of Central Banking – Lessons from the

... Almost from their beginnings, over three centuries ago, the ultimate objective of central banks has been to support sustainable economic growth through the pursuit of price stability and financial stability. Over time, however, the balance of each goal has fluctuated according to existing cultural, ...

... Almost from their beginnings, over three centuries ago, the ultimate objective of central banks has been to support sustainable economic growth through the pursuit of price stability and financial stability. Over time, however, the balance of each goal has fluctuated according to existing cultural, ...

Why are Central Banks Delegated Macroprudential Responsibilities?

... Next to addressing adverse political economy problems and the opportunities for corruption that bedevil MPR policy, the complexity of macroprudential policy is a further reason that justifies its delegation to an ‘expert’ central banks. A systemic approach to financial stability entails understandin ...

... Next to addressing adverse political economy problems and the opportunities for corruption that bedevil MPR policy, the complexity of macroprudential policy is a further reason that justifies its delegation to an ‘expert’ central banks. A systemic approach to financial stability entails understandin ...

PDF

... efficient decision making and investments will not develop. Many CEE countries have tried to rectify this problem by providing debt rescheduling and new loans at subsidised interest rates, often zero, for previous “old” debts e.g. Romania. This is just correcting the symptoms, not the cause, which i ...

... efficient decision making and investments will not develop. Many CEE countries have tried to rectify this problem by providing debt rescheduling and new loans at subsidised interest rates, often zero, for previous “old” debts e.g. Romania. This is just correcting the symptoms, not the cause, which i ...

New Capital Rules for Community Banks

... Cumulative preferred stock no longer qualifies as Tier 1 capital of any kind (subject to phase-out) Certain hybrid capital instruments, including trust preferred securities, no longer qualifies as Tier 1 capital of any kind (subject to phase-out) But such non-qualifying capital instruments iss ...

... Cumulative preferred stock no longer qualifies as Tier 1 capital of any kind (subject to phase-out) Certain hybrid capital instruments, including trust preferred securities, no longer qualifies as Tier 1 capital of any kind (subject to phase-out) But such non-qualifying capital instruments iss ...

Fund Transfer Pricing in a Commercial Bank

... Storing money allowed for facilitation of payments between bank’s customers. If two merchants had coins stored in one bank, it was easier to clear their positions through a bank than to actually move coins, especially at a distance or when large amounts were involved.8 Banks allow not only for execu ...

... Storing money allowed for facilitation of payments between bank’s customers. If two merchants had coins stored in one bank, it was easier to clear their positions through a bank than to actually move coins, especially at a distance or when large amounts were involved.8 Banks allow not only for execu ...

Banking on Preemption: Allowing National Bank Act Preemption for

... into question whether deference continues after a national bank has sold its interest in the original loan.5 This question is important because it affects the interest rates that consumers will be charged on their loans and could affect how national banks manage their balance sheets.6 A restriction ...

... into question whether deference continues after a national bank has sold its interest in the original loan.5 This question is important because it affects the interest rates that consumers will be charged on their loans and could affect how national banks manage their balance sheets.6 A restriction ...

What Money Market Mutual Fund Reform Means for Banks And

... bank accounts.19 MMMFs typically generate greater yields on “idle funds” than interest-bearing bank accounts.20 For example, while funds in a bank savings deposit account accrue interest at “artificially low” rates set by the bank, MMMF shareholders receive interest based on the current market rates ...

... bank accounts.19 MMMFs typically generate greater yields on “idle funds” than interest-bearing bank accounts.20 For example, while funds in a bank savings deposit account accrue interest at “artificially low” rates set by the bank, MMMF shareholders receive interest based on the current market rates ...

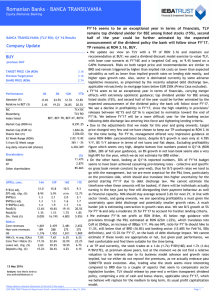

Romanian Banks – BANCA TRANSILVANIA

... reccomendation at BUY; we used a dividend discount model exercise to value TLV, with base case scenario at FY’16E and a targeted CoE avg. at 9.4% based on a CAPM framework. Risks on both target price and recommendation are similar to BRD and remain triggered by higher than implied risk costs on lowe ...

... reccomendation at BUY; we used a dividend discount model exercise to value TLV, with base case scenario at FY’16E and a targeted CoE avg. at 9.4% based on a CAPM framework. Risks on both target price and recommendation are similar to BRD and remain triggered by higher than implied risk costs on lowe ...

The ECB`s non-standard monetary policy measures

... particular, the prohibition of monetary financing by the central bank (Article 123), 1 the prohibition of privileged access by public institutions or governments to financial institutions (Article 124), 2 the “no-bailout” clause (Article 125), the fiscal provisions for avoiding excessive government ...

... particular, the prohibition of monetary financing by the central bank (Article 123), 1 the prohibition of privileged access by public institutions or governments to financial institutions (Article 124), 2 the “no-bailout” clause (Article 125), the fiscal provisions for avoiding excessive government ...

Why are Banks Highly Interconnected?

... of 0.05 to bank 3, and both banks would remain solvent and the payoffs of both banks would be 0. Offering them even slightly more would make them better off than being liquidated. There are two reasons why the interbank loan is successful in averting liquidations: First, the solvent bank, which itse ...

... of 0.05 to bank 3, and both banks would remain solvent and the payoffs of both banks would be 0. Offering them even slightly more would make them better off than being liquidated. There are two reasons why the interbank loan is successful in averting liquidations: First, the solvent bank, which itse ...

deposit protection board

... • Coverage should be set in the region of one to two times per capita GDP (Garcia:2000). • However this approach may fail to produce the desired result due to the following reasons; • Income distribution is not the same in different countries, • what is considered a “small depositor” depends on the ...

... • Coverage should be set in the region of one to two times per capita GDP (Garcia:2000). • However this approach may fail to produce the desired result due to the following reasons; • Income distribution is not the same in different countries, • what is considered a “small depositor” depends on the ...

Bank

A bank is a financial intermediary that creates credit by lending money to a borrower, thereby creating a corresponding deposit on the bank's balance sheet. Lending activities can be performed either directly or indirectly through capital markets. Due to their importance in the financial system and influence on national economies, banks are highly regulated in most countries. Most nations have institutionalized a system known as fractional reserve banking under which banks hold liquid assets equal to only a portion of their current liabilities. In addition to other regulations intended to ensure liquidity, banks are generally subject to minimum capital requirements based on an international set of capital standards, known as the Basel Accords.Banking in its modern sense evolved in the 14th century in the rich cities of Renaissance Italy but in many ways was a continuation of ideas and concepts of credit and lending that had their roots in the ancient world. In the history of banking, a number of banking dynasties — notably, the Medicis, the Fuggers, the Welsers, the Berenbergs and the Rothschilds — have played a central role over many centuries. The oldest existing retail bank is Monte dei Paschi di Siena, while the oldest existing merchant bank is Berenberg Bank.