08 short run co sts

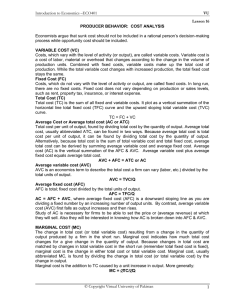

... Although the easiest way to derive marginal cost is to look at total variable cost and subtract, do not lose sight of the fact that when a firm increases its output level, it hires or demands more inputs. Marginal cost measures the additional cost of inputs required to produce each successive unit o ...

... Although the easiest way to derive marginal cost is to look at total variable cost and subtract, do not lose sight of the fact that when a firm increases its output level, it hires or demands more inputs. Marginal cost measures the additional cost of inputs required to produce each successive unit o ...

is the cost. - SNS Courseware

... The firm must pay proportional amount for rawmaterials, labour and other inputs, which is the TVC represented by bQ in the equation. The equation for Total Cost = Total Fixed Cost + Total Variable Cost Will thus be given as TC = a + bQ. At Zero output TC = a + bxo = a =TFC Average Total Cost = TC ...

... The firm must pay proportional amount for rawmaterials, labour and other inputs, which is the TVC represented by bQ in the equation. The equation for Total Cost = Total Fixed Cost + Total Variable Cost Will thus be given as TC = a + bQ. At Zero output TC = a + bxo = a =TFC Average Total Cost = TC ...

Microeconomics Instructor Miller Technology, Production

... 35. The president of Toyota's Georgetown plant was quoted as saying, "Demand for high volumes saps your energy. Over a period of time, it eroded our focus [and] thinned out the expertise and knowledge we painstakingly built up over the years." This quote suggests that A) Toyota was experiencing an e ...

... 35. The president of Toyota's Georgetown plant was quoted as saying, "Demand for high volumes saps your energy. Over a period of time, it eroded our focus [and] thinned out the expertise and knowledge we painstakingly built up over the years." This quote suggests that A) Toyota was experiencing an e ...

Cost and Costing Techniques in Managerial Economics

... analysis involves the study of revenues and costs of a firm in relation to its volume of sales. Similarly, firms develop an understanding of cost-volume-price-profit abbreviated as “CVPP analysis by supplementary and additional dimension namely ‘price’. This analysis mainly deals with cost-output re ...

... analysis involves the study of revenues and costs of a firm in relation to its volume of sales. Similarly, firms develop an understanding of cost-volume-price-profit abbreviated as “CVPP analysis by supplementary and additional dimension namely ‘price’. This analysis mainly deals with cost-output re ...

Ch 3 - PPT

... Balancing Benefits and Costs In chapter 1, one of the most basic principles of economics was that “Tradeoffs are unavoidable”. In this chapter, we look at the basics of how we juggle these trade-offs to find the best choice. We will look at… Maximizing benefits less costs Thinking on the margin ...

... Balancing Benefits and Costs In chapter 1, one of the most basic principles of economics was that “Tradeoffs are unavoidable”. In this chapter, we look at the basics of how we juggle these trade-offs to find the best choice. We will look at… Maximizing benefits less costs Thinking on the margin ...

The Economic Way of Thinking 10e ©Prentice Hall 2003

... Relative prices further informs producers of the marginal cost, and the marginal benefits, of their alternative production plans. The supply curve for corn is an upward sloping curve which reflects the marginal cost of producing corn. The area under the curve reflects the total cost of production. T ...

... Relative prices further informs producers of the marginal cost, and the marginal benefits, of their alternative production plans. The supply curve for corn is an upward sloping curve which reflects the marginal cost of producing corn. The area under the curve reflects the total cost of production. T ...

chapter overview

... 3. Constant returns to scale will occur when ATC is constant over a variety of plant sizes. D. Both economies of scale and diseconomies of scale can be demonstrated in the real world. Larger corporations at first may be successful in lowering costs and realizing economies of scale. To keep from expe ...

... 3. Constant returns to scale will occur when ATC is constant over a variety of plant sizes. D. Both economies of scale and diseconomies of scale can be demonstrated in the real world. Larger corporations at first may be successful in lowering costs and realizing economies of scale. To keep from expe ...

Document

... Iso cost curve refers to that cost curve which will be show the various commodities of two inputs which can be purchased with a given amount of total money. In the Below diagram it can be seen that as the level of production changes. The total cost will change and automatically the iso cost curve ...

... Iso cost curve refers to that cost curve which will be show the various commodities of two inputs which can be purchased with a given amount of total money. In the Below diagram it can be seen that as the level of production changes. The total cost will change and automatically the iso cost curve ...

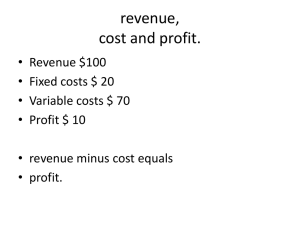

revenue, cost and profit.

... 3. At P2, will the firm make a profit, break even or have an economic loss? Will it continue to produce? Why or why not?Visual 3.6 answer 3 4. At P1 , will the firm make a profit, break even or have an economic loss? Will it continue to produce? Why or why not?Visual 3.6 answer 4 ...

... 3. At P2, will the firm make a profit, break even or have an economic loss? Will it continue to produce? Why or why not?Visual 3.6 answer 3 4. At P1 , will the firm make a profit, break even or have an economic loss? Will it continue to produce? Why or why not?Visual 3.6 answer 4 ...

Document

... – we could examine how a firm would choose k and l to maximize profit • “derived demand” theory of labor and capital inputs ...

... – we could examine how a firm would choose k and l to maximize profit • “derived demand” theory of labor and capital inputs ...

Lesson 1 - VU LMS - Virtual University

... efficiency, better utilization of resources etc.); in other words, it faces a downward sloping LRAC curve. ii. After the scale of operation is increased further, however, the firm achieve constant costs i.e., LRAC become flat. iii. If the firm further increases its scale of operation, diseconomies o ...

... efficiency, better utilization of resources etc.); in other words, it faces a downward sloping LRAC curve. ii. After the scale of operation is increased further, however, the firm achieve constant costs i.e., LRAC become flat. iii. If the firm further increases its scale of operation, diseconomies o ...

Document

... – we could examine how a firm would choose k and l to maximize profit • “derived demand” theory of labor and capital inputs ...

... – we could examine how a firm would choose k and l to maximize profit • “derived demand” theory of labor and capital inputs ...

Economic Costs and Their Use in CEA/CBA Bottom Line Outline

... or reduced by the program in their next best use. – We want to value resources consumed (social), not just money spent ...

... or reduced by the program in their next best use. – We want to value resources consumed (social), not just money spent ...

Nellis and Parker Chapter 3 – The analysis of production costs

... long-run, everything was variable ⇒ we can increase production by changing any inputs, even capital. We can also go in the other direction. Consider a firm that has a very large factory (8-track tape factory) – if demand for that product decreases, the firm might be stuck with excess capacity in the ...

... long-run, everything was variable ⇒ we can increase production by changing any inputs, even capital. We can also go in the other direction. Consider a firm that has a very large factory (8-track tape factory) – if demand for that product decreases, the firm might be stuck with excess capacity in the ...

The Supply of Goods

... Introduction • The theory of supply, like demand theory, assumes that decision makers face alternatives and choices. – Choices based on comparing expected benefits and costs ...

... Introduction • The theory of supply, like demand theory, assumes that decision makers face alternatives and choices. – Choices based on comparing expected benefits and costs ...

Total Variable costs.

... adjust such as labor, raw material, fuel and power but some resources need much more time to adjust such as building, machinery and equipment. Because of this differences in adjustment time, economists consider everything into two conceptual periods: the short run and the long run. ...

... adjust such as labor, raw material, fuel and power but some resources need much more time to adjust such as building, machinery and equipment. Because of this differences in adjustment time, economists consider everything into two conceptual periods: the short run and the long run. ...

LECTURE 2

... This may be considered by correlating energy efficiency with the annual expense of operation. For example an electrical device such as a pump or motor will require more power consumption in case of lower energy efficiency. Typically, a more energyefficient device requires a higher capital investment ...

... This may be considered by correlating energy efficiency with the annual expense of operation. For example an electrical device such as a pump or motor will require more power consumption in case of lower energy efficiency. Typically, a more energyefficient device requires a higher capital investment ...

On the geometry of the consumer`s surplus line integral

... from the initial state to the new state, of the difference between the willingness to pay and the amount actually paid for the good. The extension to the case of a set of inter-related goods was first tackled by Hotelling (1938) who proposed a line integral in the quantity space as generalisation of ...

... from the initial state to the new state, of the difference between the willingness to pay and the amount actually paid for the good. The extension to the case of a set of inter-related goods was first tackled by Hotelling (1938) who proposed a line integral in the quantity space as generalisation of ...

Slide 1

... Returns to Scale • Economies of Scale – when a firm’s long-run average total cost declines as it’s output increases. • Increasing Returns to Scale – when output increases more than in proportion to an increase in all inputs • Diseconomies of Scale - when a firm’s long-run average total cost increas ...

... Returns to Scale • Economies of Scale – when a firm’s long-run average total cost declines as it’s output increases. • Increasing Returns to Scale – when output increases more than in proportion to an increase in all inputs • Diseconomies of Scale - when a firm’s long-run average total cost increas ...

Fourth Edition - pearsoncmg.com

... Can Government Policies Help Protect the Environment? • Government policies to reduce pollution have proven to be controversial. • In the past, Congress often ordered firms to use particular methods to reduce pollution, but many economists are critical of this approach—known as command and control— ...

... Can Government Policies Help Protect the Environment? • Government policies to reduce pollution have proven to be controversial. • In the past, Congress often ordered firms to use particular methods to reduce pollution, but many economists are critical of this approach—known as command and control— ...

Costs 5.2

... Value of the next best alternative not chosen Value of the thing given up when you choose between two things A business can measure the outcome of a decision by comparing it with the benefits (probably measured in profits or revenue) it could have had if it had taken the next best option. Th ...

... Value of the next best alternative not chosen Value of the thing given up when you choose between two things A business can measure the outcome of a decision by comparing it with the benefits (probably measured in profits or revenue) it could have had if it had taken the next best option. Th ...

Production & Cost in the Firm

... Economic Costs • Costs exists because resources are scarce and have alternative uses • When society uses a combination of resources to produce a particular product, it foregoes all alternative opportunities to use those resources for other purposes. • The measure of the economic cost or the opportu ...

... Economic Costs • Costs exists because resources are scarce and have alternative uses • When society uses a combination of resources to produce a particular product, it foregoes all alternative opportunities to use those resources for other purposes. • The measure of the economic cost or the opportu ...