Pricing and Hedging Volatility Derivatives

Pricing and Hedging of swing options in the European electricity and

Pricing and hedging in exponential Lévy models: review of recent

Price Comparison Results and Super-replication: An

Press release

Presentation

United States & Canada

Understanding Volatility

Understanding Different Contracting Methods for Marketing

Understanding Bonds

Unconstrained Fitting of Non-Central Risk-Neutral

UCITS Alternatives

U1S09_Su10_Lesson_04 - U1S09-2010

U.S. EQUITY HIGH VOLATILITY PUT WRITE INDEX FUND (NYSE

Transactional Energy Market Information Exchange (TeMIX) using

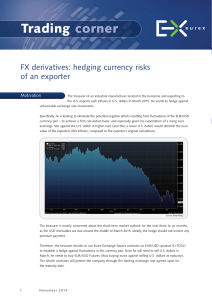

Trading Corner - Eurex Exchange

tr-1: notification of major interest in shares

Towards a Theory of Volatility Trading

Total Product of Labor (cakes per worker)

Topics in Financial Mathematics