Valuation of Bonds

Valuation of Asian Options

VALUATION IN DERIVATIVES MARKETS

Using Scenario Analysis to Look at a Company`s Range of Outcomes

Using futures and options to manage price volatility in food imports: practice

URL - StealthSkater

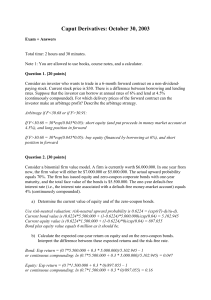

Question 1

Puts and calls

put

PSF Portfolio Optimization Conservative

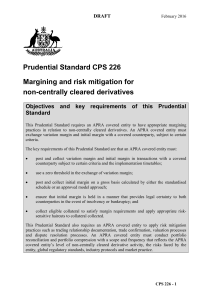

Prudential Standard CPS 226 Margining and risk mitigation for non

Prudential Standard CPS 226 Margining and risk mitigation for non

Project Recommended by United Technologies

Professor Banko`s Presentation

Problem Set 7 Solution

probability prediction with static Merton-D-Vine copula model

Pricing Volatility Derivatives with General Risk Functions Alejandro Balbás University Carlos III

Pricing Swing Options and other Electricity Derivatives

Pricing Short-Term Market Risk: Evidence from

Pricing of Interest Rate Derivatives