Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Economic democracy wikipedia , lookup

Business cycle wikipedia , lookup

Fiscal multiplier wikipedia , lookup

Consumerism wikipedia , lookup

Long Depression wikipedia , lookup

Refusal of work wikipedia , lookup

Economic calculation problem wikipedia , lookup

Post–World War II economic expansion wikipedia , lookup

Transformation in economics wikipedia , lookup

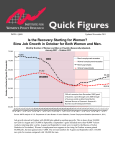

PRESIDENT'S REPORT TO THE BOARD OF DIRECTORS, FEDERAL RESERVE BANK OF BOSTON Current Economic Developments - February 13, 2003 Data released since your last Directors' meeting show the economy continues to expand, although at a slow pace. Concern about future stength remains high and data for the first quarter remains sparse. Nonfarm payroll employment rose by 143,000 in January, marking the biggest job gain since November 2000. Still December's payroll employment was revised further downward and the 3-month moving average, which is a better indicator of labor market strength, remains below zero. The unemployment rate fell to 5.7%. In January, auto and light truck sales slowed, as consumer confidence fell. And on the supply side, the ISM index edged slightly downward. During the fourth quarter, real GDP growth slowed, led by a pullback in consumer spending on durable goods. The deceleration in consumer spending was partly offset by an increase in fixed investment and an acceleration in government spending. Nonfarm payroll employment rose in January for the first time in three months, by 143,000 yet the 3-month moving average remains below zero. Nonfarm Payroll Employment Change from Previous Month 200 Recession Began Payroll Employment 100 0 -100 3-Month Moving Average -200 -300 -400 -500 Jan-01 May-01 Mar-01 Sep-01 Jul-01 Source: Bureau of Labor Statistics. Jan-02 Nov-01 May-02 Mar-02 Sep-02 Jul-02 Jan-03 Nov-02 Initial claims edged downward in January to its lowest level since July 2002, yet claims have been relatively flat over the past six months. The unemployment rate fell in January to 5.7 precent. Unemployment Rate and Initial Claims Thousands of Units at Annual Rates Percent 6.5 500 6.0 450 Recession Began 5.5 400 5.0 4.5 Initial Claims 4-Week Moving Average Ending February 1st 384,750 Unemployment Rate 350 4.0 300 Jan-01 May-01 Mar-01 Sep-01 Jul-01 Jan-02 Nov-01 May-02 Mar-02 Sep-02 Jul-02 Jan-03 Nov-02 Source: Department of Labor. Total auto and light truck sales slowed in January, compared to December. January's estimate was also slightly lower than the average seen during the fourth quarter. Auto and Light Truck Sales Millions of Units at Annual Rates 22.0 Recession Began 21.0 2002:Q1 2002:Q2 2002:Q3 2002:Q4 16.3 16.3 17.6 20.0 16.5 January 16.1 19.0 18.0 17.0 16.0 15.0 Jan-01 May-01 Mar-01 Sep-01 Jul-01 Source: Bureau of Economic Analysis. Jan-02 Nov-01 May-02 Mar-02 Sep-02 Jul-02 Jan-03 Nov-02 Consumer confidence and expectations fell in January, as concern about weak economic growth increased and geo-political risks rose. Confidence and Expectations Index, 1985 = 100 Recession Began 140 Consumer Expectations 120 100 Consumer Confidence 80 60 Jan-00 Jan-01 Jan-02 Jan-03 Source: The Conference Board. Sentiment and Expectations Index, 1966:Q1 = 100 120 Recession Began 110 Consumer Sentiment 100 90 Consumer Expectations 80 70 Jan-00 Jan-01 Jan-02 Jan-03 Source: The University of Michigan. The ISM index slowed in January, compared to December. Still estimates over the past two months show some improvement, compared to the previous five months. ISM Indexes Index (50+ = Economic Expansion) 60.0 Recession Began 55.0 50.0 45.0 40.0 35.0 Jan-00 May-00 Sep-00 Jan-01 Source: Institute for Supply Management. May-01 Sep-01 Jan-02 May-02 Sep-02 30.0 Jan-03 Economic growth slowed during the fourth quarter. The deceleration was led by a sharp pullback in consumption. Real Gross Domestic Product Annualized Percent Change 8.0 Recession Began 7.0 6.0 5.0 4.0 3.0 2.0 1.0 0.0 -1.0 -2.0 -3.0 99:Q4 00:Q1 00:Q2 00:Q3 00:Q4 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 Source: Bureau of Economic Analysis. During the fourth quarter, the slowdown in consumer spending was led by a drop in durable goods consumption. Real Consumption Annualized Percent Change 40 7.0 Recession Began 6.0 30 Durable Goods Total Consumption 20 5.0 4.0 3.0 10 2.0 0 1.0 -10 0.0 99:Q4 00:Q1 00:Q2 00:Q3 00:Q4 Source: Bureau of Economic Analysis. 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 The weaker consumer spending was offset somewhat by increases in residential and business investment. Business investment posted its first gain in over two years. Residential and Business Investment Annualized Percent Change 20.0 Recession Began Residential Investment 10.0 0.0 Business Investment -10.0 -20.0 99:Q4 00:Q1 00:Q2 00:Q3 00:Q4 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 Source: Bureau of Economic Analysis. Slower consumer spending was also offset somewhat by an increase in government spending. Government Spending Annualized Percent Change 12.0 Recession Began 10.0 8.0 6.0 4.0 2.0 0.0 -2.0 99:Q4 00:Q1 00:Q2 00:Q3 00:Q4 Source: Bureau of Economic Analysis. 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 And productivity fell during the fourth quarter for the first time since the second quarter of 2001. Despite the drop in productivity, compensation costs eased somewhat. Productivity and Costs Annualized Percent Change 20.0 15.0 Recession Began 10.0 Compensation Costs 5.0 0.0 Output per Hour -5.0 99:Q4 00:Q1 00:Q2 00:Q3 00:Q4 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 Source: Bureau of Labor Statistics. During the fourth quarter, the ECI's total compensation eased somewhat, following the recent pattern of wages and salaries, despite an increase in benefit costs. Employment Cost Index Percent Change, Year-Over-Year 5.5 Benefit Costs Civilian Workers Recession Began 5.0 Total Compensation Civilian Workers 4.5 4.0 3.5 Wages and Salaries Civilian Workers 3.0 2.5 99:Q4 00:Q1 00:Q2 00:Q3 Source: Bureau of Labor Statistics. 00:Q4 01:Q1 01:Q2 01:Q3 01:Q4 02:Q1 02:Q2 02:Q3 02:Q4 Over the past year, inflation at both the consumer and producer levels have remained low. Producer Prices Consumer Prices Percent Change, Year-to-Year Percent Change, Year-to-Year 6.0 4.0 Producer Price Index Consumer Price Index, excluding food and energy 5.0 3.5 4.0 Producer Price Index, excluding food and energy 3.0 3.0 2.0 2.5 1.0 2.0 0.0 Recession Began 1.5 Recession Began -1.0 -2.0 1.0 -3.0 Consumer Price Index Dec-99 Dec-00 Jun-00 0.5 Dec-02 Dec-01 Jun-01 Jun-02 Dec-99 Dec-00 Jun-00 Source: Bureau of Labor Statistics. -4.0 Dec-02 Dec-01 Jun-01 Jun-02 Source: Bureau of Labor Statistics. Overall, the economy is expanding, but increasing geopolitical risks and falling consumer confidence have raised downside risks. Federal Funds Rate Percent 7.0 6.0 5.0 4.0 3.0 2.0 1.0 0.0 Jan-01 May-01 Sep-01 Source: Federal Reserve Board of Governors. Jan-02 May-02 Sep-02 Jan-03