Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

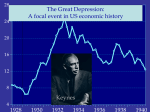

http://www.amatecon.com/gd/gdcandc.html Causes and Cures Introduction It should be noted that all of the cures have been tried and while we seem to be free of Depressions, it's not clear that business cycles have been eliminated. Causes The Stock Market Crash The Stock Market Crash in October of 1929 is often cited as the beginning of the Great Depression, but did it actually cause it? The answer is no. First, the stock price for a particular company merely reflects current information about the future income stream of that company. Thus, it is a change in available information that changes the stock price. When the Fed began to raise interest rates in early 1929, this began the tumble. However, a stock market crash could cause people to increase their liquidity preference which might lead them to hoard money. In the August 1990 issue of The Quarterly Journal of Economics, Christine D. Romer writes that "the negative effect of stock market variability is more than strong enough to account for the entire decline in real consumer spending on durables that occurred in late 1929 and 1930." Hoarding Money People hoard money because they have a liquidity preference. I.e., people want to have their assets in a readily convertible form, such as money. There are several misconceptions about hoarding money. First hoarding is not the same thing as saving. If I put my money into a savings account, that money is lent out to someone else who then spends it. Second, hoarding, by itself, cannot cause a recession or depression. As long as prices and wages drop instantly to reflect the lower amount of money in the economy, then hoarding causes no problems. Indeed, hoarding can even be seen as beneficial to those who don't hoard, since their money will be able to buy more goods as a result of the lower prices. If a country has a gold standard, then hoarding money can make the money supply drop dramatically since a gold standard makes the quantity of money difficult for the government to control. The Gold Standard At the time of the Great Depression,America had a 100% gold standard for its money. This meant that all cash was backed by a government promise to redeem it in a specific amount of gold (at the time, one ounce of gold was redeemable for twenty dollars). Because the amount of money circulating in the economy is wholly dependent on the amount of gold available, the money supply is very rigid. If people start to hoard money (see above) the money supply can drop drastically. As noted in the previous section on hoarding, this is not a problem as long as prices and wages drop instantly to reflect the lower amount of money circulating. Hall and Ferguson write: 1 The existence of the gold standard linked economic conditions across countries to a much greater extent than is currently the case, and it is because of this linkage that the Depression was a worldwide event. and: Except for minor adjustments, and the temporary suspensions of gold payments during wartimes, the price of gold was held standard from the establishment of the new United States of America in 1791 until gold was revalued in 1933. In "Gold Standards and the Real Bills Doctrine in U.S. Monetary Policy" (PDF), professor Richard Timberlake argues that the gold standard was not responsible for the Great Depression, since the Federal Reserve had not been following a strict gold standard prior to the onset of the Depression. The Smoot-Hawley Tariff In 1988, the Council of Economic Advisors proclaimed that the Smoot Hawley Tariff Act was "probably one of the most damaging pieces of legislation ever signed in the United States." The act was passed in June of 1930 and increased tariffs to a tax of 50 percent on goods imported into the United States. Since this occurred after the onset of the Depression, it's hard to see how it could have caused it. However, since the real effect of the increased tariffs was to increase prices and increase price rigidity, it is easy to see how the Act could have exacerbated the Depression. Enacting the tariff was exactly the wrong thing to do and about 1,000 economists signed a petition begging Congress not to pass it. Eventually, 60 other countries passed retaliatory tariffs in response. The Federal Reserve Board The Fed was ostensibly created to prevent bank panics and Depressions. Is it possible that the Fedwas actually responsible for the Depression? The answer is a qualified no. The Fed took several actions that, in retrospect, were quite bad. The first thing it did was to inflate the money supply by about 60% during the 1920's. If the Fed had been a little more careful in expanding the money supply, it might have prevented the artificial Stock market boom and subsequent crash. Second, there are indications that the economy was starting to cool off on its own in early 1929, thus making the interest rate hike in TBD completely unnecessary and avoiding the subsequent crash. The third mistake the Fed made was in early 1931. The Fed raised interest rates, exactly the wrong thing to do during a contraction. Ironically, the country's gold stock was increasing at this point all on its own, so doing nothing would have increased the money supply and helped the recovery. Hall and Ferguson write that: The Federal Reserve began expressing concern in early 1928 and at that time began a policy of monetary restriction in an effort to stem the stock market advance. This policy continued through May 1929. The monetary restriction was carried out by selling $405 million in government securities and raising the discount rate in three stages from 3.5 percent to 5 percent at all Federal Reserve banks. and: the monetary expansion of 1927 is considered by many economists to be an important factor in setting off the U.S. stock market advances of the lates 1920s. Hall and Ferguson also write that: But a further irony is the fact that the very existence of the Federal Reserve caused banks to wait for the central bank to act and not turn to the solutions they had devised in the face of the banking crises of the nineteenth century. But even with all that bungling, it is not clear that we can lay responsibility for the Great Depression at the feet of the Fed. Malinvestment "Malinvestment" is a term coined by the Austrian school of economics to sum up their explanation of the causes of business cycles. According to this theory, all business cycles are caused by government intervention in the market. Specifically, the central bank (the Fed in the case of the 2 U.S.) artificially lowers the interest rate, flooding the economy with money. This money is then invested in capital goods that would not be justified at a market level of interest rates. The low interest rate cannot be sustained forever without an increase in inflation, so the Fed inevitably has to raise interest rates. When this happens, the investments that were "justified" under a lower interest rate must be liquidated. Any prevention of this liquidation by further government intervention will simply prolong the re-adjustment and thus exacerbate the recovery. This view is held by very few economists. Sticky Prices/Sticky Wages Prices and wages change in accordance to the scarcity of goods and labor relative to the amount of money that is available to buy them. For example, if the Federal Reserve Boardincreases the nation's money supply, then prices and wages will tend togo up, reflecting the fact that more money is chasing the same amount of goods and labor. When the Fed does too much of this, it is called inflation. But what happens if the money supply goes down relative to the amount of goods and labor? Eventually, the price of goods and labor will go down as well in the long run. But in the short run, prices and wages can "stick" at a higher level than the market clearing price or wage. When this happens, people buy less and employers hire less, thus causing cut backs in production and employment. There are a number of reasons why prices and wages might stick. One reason is referred to as "menu costs," meaning that it often costs money to change a price. A good example is a restaurant that has to print new menus every time the prices change. Income Inequality In American Inequality: A Macroeconomic History (1980), by Jeffrey G. Williamson and Peter H. Lindert, it is reported that the period of 1928 through the first three quarters of 1929, using any number of income inequality measures, the U.S. may have experienced "the highest income inequalities in American History" . In The Great Depression: An International Disaster of Perverse Economic Policies, Hall & Ferguson write that: Wages grew more slowly than output per worker, which suggests that corporate profits were rising. This change shows up as rising dividends, which constituted 4.3 percent of national income in 1920 and rose to 7.2 percent of national income by 1929 (Soule 1947, 284). Since 82 percent of all dividends were paid to the top 5 percent of income earners, this clearly helped contribute to the change in income inequality (Potter 1974). and: But critics of that view contend that increase inequality of income and wealth is an unlikely candidate to cause an economic decline on the order of the Great Depression. Their criticism of the underconsumptionist view is that it ignores an obvious adjustment mechanism; if deficient demand for goods and services is caused by unequal distribution of income, then the price level would fall to cause the quantity of goods and services demanded to rise. Underconsumptionists respond that prices could not fall because of various rigidities built into the economic system (see, for example, Strikcer 1983-84). However, as economist Arnold Kling explains while reviewing Randall E. Parker's Reflections on the Great Depression, a collection of interviews of economists who lived through the Great Depression: A number of myths that are popular in conventional histories of the Depression are punctured in Parker's book. For example, the Wikipedia echoes many textbooks in saying, "A fundamental misdistribution of purchasing power, the greatly unequal distribution of wealth throughout the 1920s, was a factor contributing to the depression." None of the economists interviewed by Parker cites this so-called causal factor. 3