Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

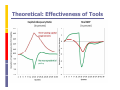

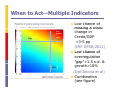

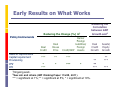

Connecting the Dots: Designing i i Macroprudential d i l Tools that Work L Laura E E. Kodres K d Assistant Director Monetary and Capital Markets Department September 27, 2012 Outline What types of systemic risks are we attempting tt ti tto mitigate? iti t ? Connecting systemic risks to e te nalities/ma ket failures externalities/market fail es Connecting externalities to indicators of systemic risks Connecting indicators to practical policy tools Existing limitations and limiting expectations Connecting the Dots Externalities Systemic Risk Indicators Policy Tools ? Minimize effects of externalities Types of Systemic Risks Time-series dimension Procyclicality of credit Asset/collateral booms and busts Cross-section/interconnectedness dimension Counterparty credit risks Interbank freezes Externalities and Systemic Risks Coordination failures Fire sales Procyclicality of credit/leverage Similar position taking/reaction to common incentives Dependence on bailouts/benchmarking Marked to market accounting/credit ratings Margin/collateral calls VaR systems Cross-sectional/Interconnectedness Interbank/wholesale funding freezes H d i Hedging and d portfolio tf li rebalancing b l i Externalities and Tools (I) Require tools to address type of externality Excess credit/leverage is solvency issue—consider tools to limit insolvency Runs in wholesale funding markets is a liquidity issue—consider tools to limit illiquidity Decide who/what to apply the tool Types of institutions/people “Market” Market functioning/structure Decide price-based or quantity-based? Decide where systemic risks go? Still with institution or with public sector? Externalities and Tools (II) How much does institution or market “contribute” contribute to systemic risk? Need a specific measure of the systemic risk or externality How granular/specific does it need to be? Consider these “contributions” as intermediate t target t measures or iindicators di t off systemic t i risk i k Indicators/Measures (I) Coordination failures and fires sales Various credit measures – credit to GDP, credit to GDP gap, real credit growth Leverage – assets/equity House prices – real house price indices deflated by CPI Liquidity – non-core non core funding (bank credit/deposits) Capital flows – foreign liabilities/foreign assets for banks Margining/collateral practices Indicators/Measures (II) (Mostly) cross-sectional/interconnectedness dimension Marginal Expected Shortfall (MES) Conditional Value-at-Risk (CoVar) Systemic Contingent Claims Analysis (SCCA) Systemic liquidity risk index (SLRI) Joint Probability of Default (JPoD) Network-based metrics Typically T i ll measures use market k t data d t on institutions (with some balance sheet information or some bilateral exposure data) Connecting Indicators to Tools (I) Time-series tools are applied to institutions but since measure is relatively “fuzzy” fuzzy both mitigates “regular” risk and systemic risk Reserve requirements q Capital requirements Provisioning Loan-to-value ratios Debt-to-income ratios Some tools can be applied to “markets” Through-the-cycle margin/haircuts R Removal l off investment i t t grade d credit dit ratings ti Connecting Indicators to Tools (II) Cross-section/interconnectedness tools young G-SIFI G SIFI surcharge h Basel 2.5 risk-weights for counterparty credit risk Other solvency surcharges Liquidity charge/premium Network modeling and CreditRisk+ CCA used to calculate solvency distress Stress tests CCA used to calculate liquidity distress: “market market risk” risk NSFR Actuarially-fair insurance based on “contribution” to Systemic Liquidity Index Tools T l tend t d to t b be more complex, l but b t more precisely aimed at externality Connecting Indicators to Tools (III) How to connect to solvency surcharge Calculate C l l t aggregate t loss l given i default d f lt (LGD) using i credit VaR (monetary losses for the entire system with and without Bank X’s interbank exposures) based on individual bank’s probability of default, assets, and LGDs Multiply by probability of default of Bank X Gives expected loss to system of default of Bank X – g Bank X this amount (as ( percent p of capital). p ) charge Can average these through the cycle to add a countercyclical component (GFSR April A il 2010) Indicators and policies A stitch in time Theoretical: Effectiveness of Tools When to Act—Multiple Indicators Low chance of missing a crisis: change in Credit/GDP >3-5 pp (IMF GFSR,2011) Low chance of overregulation ”gap”>1.5 g p s.d. & growth>10% (Dell’Ariccia et al) Combination b (see figure) Crisis probability 20-25% >5 pp >15% Policies costly if source of shocks (ex: Squashing healthy gro.… with time-varying capital) When Not To Act When to Act—Near-Coincident Indicators Performance of marketmarket-based indicators Source: Arsov, Canetti, Kodres, and Mitra (forthcoming) Early Results on What Works Policy Instruments Reserve requirements Capital requirement Provisioning LTV DTI 1Ongoing Reducing the Change (%) in1 Banks' F i Foreign Real Liabilities/ House Foreign Real Price Credit/GDP Credit / Assets *** * *** ** *** * *** * *** * work. 2See Lim and others (IMF Working Paper 11/238, 11/238 2011) *** = significant at 1%; ** = significant at 5%; * = significant at 10%. Reducing the Correlation between GDP Growth and2 Real Credit Growth *** ** ** *** Assets/ Equity Growth *** ** *** *** Existing g Limitations ((I)) Cross-sectional assignment of systemic risk incomplete Institution needs to know direct and indirect connections /knock-on effects to judge risk of a direct counterparty exposure exposure. Institution A does not want to be “charged” for exposing distant counterparties to its risks (not its “f lt”) “fault”). Should market data be relied upon to assess these risks? Would removing asymmetric information by publishing all exposure data fix the externality? Or wreck the smooth functioning of markets? Designing Tools with Networks Bank 1 Bank X Bank A Bank 2 Bank 3 Bank Y Bank 4 Bank 6 Bank 5 Existing g Limitations ((II)) How much reliance on market discipline? How can incentives be harnessed to control systemic y risk? Can systemic risk, by it very nature, be solved by more market discipline? How much confidentiality should institutions be allowed? The more systemic you are, the more you pay to be part of the system? Can one reasonably reduce one one’s s systemic-ness? systemic ness? What about the beneficiaries of safe systems? Should they pay? Can simplicity be encouraged? Mandated? Limiting Expectations How much systemic risk is optimal to mitigate? Not all… How much can policymakers realistically plan to offset with macroprudential tool? Versus microprudential tools? Versus monetary policy? Exchange rate policy? Versus fiscal policy? What about ex post tools to deal with realization of systemic y risks? Resolution LOLR B il Bail-outs/Bail-ins /B il i Connecting the Dots: Designing Macroprudential Tools that Work L Laura E E. Kodres K d Assistant Director Monetary and Capital Markets Department September 27, 2012