Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

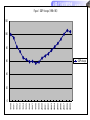

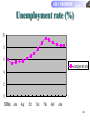

The economic crisis in Russia: Fragility and Robustness of Globalisation Satoshi Mizobata KIER, Kyoto University Workshop in Vietnam, September 2009 Introduction • Transition economies and the global crisis: Is transition over? • The economic growth and the crisis: The crisis spread to the success market. Dual surpluses are the base of the growth, but they become weak points. • Is the Russian market normal or abnormal? 1.Reconsidered economic growth in the 2000s High economic growth by energy and resources: an increase of reserve and export revenue Heavily dependent on the mineral resources: fragility and sensitivity of the Russian economy to the global market The state budgets depend on the global markets. 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 Figure 1 GDP change (1990=100) 120 100 80 60 GDPchange 40 20 0 Macroeconomic indicator 1993 1994 1995 1996 1997 1998 2003 2004 2005 2006 2007 GDPannual growth rate -8.7 -12.6 -4.0 -5.0 0.4 -4.9 7.3 7.2 6.4 6.7 8.1 Consumer price growth rate 840 215 131 21.8 11.0 56.4 12.0 11.7 10.9 9.0 12.2 Investment increase rate -12 -26 -13 -18 -6 -5.1 12.5 13.7 10.9 13.7 21.1 -0.4 -2.8 -2.6 -3.8 4.1 -2.9 6.7 10.2 11.4 9.9 Federal budget, deficit and surplus -10.4 -9.8 -5.2 -7.9 -7.0 -3.0 1.3 4.5 8.1 8.4 6.0 Oil production (t, million) 345 310 298 293 297 294 408 453 462 491 491 Consumption increase rate Export of petroleum and gas in Russia: changing into Middle East 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 114 118 116 144 165 190 228 260 253 248 259 243 13.4 8.8 12.9 25.3 25.0 29.1 39.7 59.0 83.4 102.3 121.5 161.1 60.2 57.5 53.9 62.6 63.3 75.5 77.7 82.4 97.1 103.5 112.3 118 7.0 3.9 5.1 10.9 9.4 11.3 14.1 19.3 33.8 44.7 52.2 79.9 Natural gas Cubic meter billion $ billion 121 125 131 194 181 186 189 200 209 203 192 195 10.7 11.1 11.6 16.6 17.8 15.9 20.0 21.9 31.7 43.8 44.8 69.1 Total $ billion 31.1 23.8 29.6 52.5 52.2 56.3 73.8 100.2 148.9 190.8 218.5 310.1 Share of export (%) 34.9 31.8 39.1 50.0 51.2 52.5 54.3 54.7 61.1 62.9 61.7 65.8 Crude Oil export price $/barrel 23.9 20.8 21.0 23.8 31.0 45.2 56.3 64.3 90.7 Gas export price $/ m3 thousand 85.8 98.3 85.7 105.5 109.1 151.4 216.0 233.7 353.7 Crude oil tonnes million $ billion Oil products tonnes million $ billion Share of export in the main products products Share (%, 2005-2007) Crude oil 54-58 Petroleum products 46-48 Natural gas 28-32 Coal 49-53 Mineral fertilizer 75-85 Cellulose 80-84 Newspaper 60-65 Rolled iron 45-48 Nickel 90-95 Cobalt 90-95 Aluminum 80-85 Titan 70-75 zinc 30-40 7 Integrated government finance 1995 1998 2000 2004 2007 Financial deficit and surplus -11.2(5.2) -22.6(-3.0) 12.6(1.9) 14.0(4.5) 23.1(6.0) Tax on the corporate profits 26.9 14.5 19.0 16.0 8.2 VAT 21.9 24.8 21.8 19.7 29.1 Tariffs on the natural 2.8 resources use 3.3 3.7 10.7 14.9 Customs and others 5.0 10.9 15.8 31.0 5.7 Foreign trade in Russia ($ billion) 220 200 180 160 140 120 100 80 60 40 20 0 export import 2008Q1 Q2 Q3 Q4 2009Q1 Q2 Oil export price ($/barrel) 10 Export of energy ($ billion) 11 Foreign trade changes 1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 Change 2000-2008 export 78.2 105.0 101.9 107.3 135.9 183.2 243.8 303.6 354.4 469.0 347% import 46.7 44.9 53.8 61.0 76.1 97.4 125.4 164.3 223.5 292.5 551% balance 31.5 60.1 48.1 46.3 59.8 85.8 118.4 139.3 130.9 176.5 - Domestic market heavily depends on import. • Russian market expanded, and now it is No.1 in Europe. • Low technology and quality of consumption goods like automobile • Imported food and medicine, automobile (like Toyota and Nissan) • Russians cannot live without the global market. Russia became a Bubble economy • Skyrocket of asset price like stock and real estate (housing): The stock bubble supported another bubble, residential bubble. (in big cities) The regional gaps are large. Partial bubble economy • Continuous inflation • mismanagement of the government and inflow of cheap money Balance of payments year Current account Trade balance services Capital and financial account Changes in reserve assets Errors and omissions 1992 -0.1 3.7 -3.1 2.4 -1.9 -0.4 1993 9.0 12.6 -2.1 -4.4 -3.9 -0.7 1994 7.8 16.9 -7.0 -10.2 1.9 0.5 1995 7.0 19.8 -9.6 12.1 -10.4 -8.7 1996 10.8 21.6 -5.4 -6.4 2.8 -7.3 1997 -0.1 14.9 -5.9 10.8 -1.9 -8.8 1998 0.2 16.4 -4.1 3.8 5.3 -9.4 1999 24.6 36.0 -4.3 -14.4 -1.8 -8.5 2000 46.8 60.2 -6.7 -21.5 -16.0 -9.3 2001 33.9 48.1 -9.1 -16.2 -8.2 -9.6 2002 29.1 46.3 -9.9 -11.7 -11.4 -6.1 2003 35.4 59.9 -10.9 0.1 -26.4 -9.2 2004 59.5 85.8 -12.7 -8.4 -45.2 -5.9 2005 84.6 118.4 -13.8 -15.2 -61.5 -7.9 2006 94.9 139.3 -13.6 3.3 -107.5 9.5 2007 77.0 130.9 -19.6 84.8 -148.9 -12.9 2008 102.4 179.7 -25.1 -135.2 45.3 -12.6 2009 Q1 9.1 19.1 -4.1 -31.8 31.1 -8.3 Balance of payments and external debts (end of year, $10 billion) 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Current balance -0.08 0.2 24.6 46.8 33.9 29.1 35.4 59.5 84.4 94.3 77.0 102.4 Trade balance 14.9 16.4 36.0 60.2 48.1 46.3 59.9 85.8 118.4 139.3 130.9 179.7 Export 86.9 74.4 75.6 105.0 101.9 107.3 135.9 183.2 243.8 303.6 354.4 471.6 Import 72.0 58.0 39.5 44.9 53.8 61.0 76.1 97.4 125.4 164.3 223.5 291.9 Foreign direct investment 4.9 2.8 3.3 2.7 2.7 3.5 8.0 15.5 12.9 29.7 54.3 58.7 External debts (to the state) 149.9 158.4 148.9 128.6 111.1 104.3 106.0 97.4 71.4 48.6 46.4 32.8 Ex-USSR 95.1 98.2 96.8 65.8 61.0 55.9 58.3 56.1 34.5 9.4 7.1 4.6 External debts (to the private) 33.0 30.0 29.2 31.4 35.2 48.0 80.0 108.9 176.2 261.9 419.2 450.7 External debts per GDP (%) 44.4 67.8 93.3 65.1 50.5 43.8 39.4 33.5 30.9 31.4 36.0 28.8 External debts of enterprises ($ billion) 1993 1994 1995 1996 1997 1998 2 4 8 14 33 30 2003 2004 2005 2006 80 108 175 262 2007 417 2008 488 17 Net international investment position ($ billion) 2003 2004 2005 2006 2007 Nonfinancial -56 companies -117 -202 -307 -513 Russia, total -11 -32 -36 -127 +4 Net capital flows to the private sector ($ billions) 2004 2005 2006 Q1 Q2 Q3 Q4 -8.9 0.1 41.4 -5.6 20.6 12.4 14.4 Banking sector 3.5 5.9 27.5 -3.0 9.9 8.8 11.9 others -12.4 -5.8 13.9 -2.7 10.6 3.6 2.4 2007 Q1 Q2 Q3 Q4 2008 Q1 Q2 Q3 Q4 2009 Q1 82.4 13.9 54.5 -7.0 21.7 -132.7 -23.6 40.7 -19.2 -130.6 -38.8 45.8 0.1 36.9 -3.5 12.3 -57.6 -9.9 22.1 -13.5 -56.3 -5.8 36.6 13.8 17.4 -3.7 9.1 -75.1 -13.7 18.6 -5.7 -74.3 -32.9 Net, total 19 Capital flight and external loans ($ 10bn) 100 80 $ bn 60 40 capital flight 20 loans to private sector 0 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 -20 -40 -60 Russian economy drastically changed in the 2000s. • Economic growth maintained a twin surplus. • The economic structure becomes a fragile and sensitive to the global market. • Russia has been integrated into the global economy, and in this point, the transition is over. 2.The global crisis hit The economic crisis hit the Russian economy, and the Russian gets mired down in the crisis. Crisis under transition Transition economy and economic crisis • Contagion to transition economies Financial crisis and economic crisis (real sector crisis) • Difference of CIS countries and Central Eastern Europe: high debts and critical case of external debts in Kazakh, Ukraine, Belarus, Moldova, Tajikistan. • Contagion to non-open economy (Kyrgyz) Global crisis is strained in transition economies. Dependence on the European markets. Hungary, Latvia, Serbia…But From financial crisis to economic crisis When Russian crisis? • 2008 September: a drop down of stock price • 2008 July: limited growth of money supply and the increased interest rates • 2007 November: a decline of M&A transaction • 2007 August: weakening liquidity (V.Senchagov) A sudden drop of trading volumes in stock exchanges MICEX Объем торгов акциями, млрд руб. Объем торгов облигациями, млрд руб. 2000 400 1500 300 1000 200 500 100 0 0 янв мар 2007 май июл сен ноя янв мар 2008 май июл сен янв мар 2007 Объем размещений облигаций, млрд руб. май июл сен ноя янв 2008 мар май июл сен май июл сен Объем РЕПО, млрд руб. 100 4000 75 3000 50 2000 25 1000 0 0 янв мар 2007 май июл сен ноя янв 2008 мар май июл сен янв мар 2007 май июл сен ноя янв мар 2008 Asset price dropped suddenly after September 2008-Lehman shock • Stock price declined in MICEX and RTS. • A decline of real estate price negative chain functioned and… a collapse of bubble economy from financial sector to real sector A violent change of housing price ($/m2) Average price change of cottage in Q3 2008-Q3 2009 (%) Financing: stock market and Repo market Billion Ruble 70000 60000 50000 currency market 40000 bond market 30000 Repo market 20000 10000 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 30 Financing: stock market and Repo market Billion Ruble 1400000 1200000 1000000 currency market 800000 600000 bond market 400000 Repo market 200000 0 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 31 Share of Repo Transaction in MICEX 2005 2006 2008 2007 Q1 Q2 Stocks 18.3 25.6 50.5 58.0 62.4 Corporate bonds 28.0 50.9 71.2 77.9 77.9 Regional bonds 28.0 60.0 79.9 83.8 86.1 Municipal bonds 31.5 42.1 66.5 72.2 74.6 Enlargement of Repo market • Similar to GKO-OFZ in 1998 • Failure of Repo:7.1 billion Ruble of “KIT Finance” Margin calls:Firms with nonperforming loans in November 2008 34 Crisis Phenomena • • • • • • • • • Stock prices Foreign borrowing Margin calls Bankrupt of banks Financial crisis as SvyazInvest Consumer loans crisis: automobile and construction The sharp decline in petroleum price, aluminum and metals Construction, development, and retail External repayment: repayment $ 160 billion till the end of 2009 • Labour market • Regional gaps Industrial sectors in Crisis (1) Big shock sectors: banks, developer, retail with high leverage ratio (2) Export and resource sectors: metallurgy, nonferrous, oil and gas, diamond, paper (3) Import substitute sectors: automobile, cement Some Company cities faced difficulty. Decline of consumption and investment Production was diminished by three waves. 1) Reduction of speculation and expensive credit: developers---a decline in employment and income-a chain of reduction 2) Reduction of export profits 3) A decline in the state budget Changes of export prices in Russia ($ per ton) 1000 800 600 average real export price average world oil 'Urals' price 400 200 Se p. Ju ly y Ma r. Ma No v. 200 9J an. Ma r. Ma y 200 8.J a n 0 Export structure of Russia (2009.1-6) 39 Economic crisis in 2008-2009 2007 2008 2008Q4 2009Q1 GDP 8.1 5.6 1.1 -9.5 Industrial production 6.3 2.1 -6.1 -14.3 manufacturing 9.5 3.2 -7.7 -20.8 Retail trade 16.1 13.5 8.6 -1.1 investment 21.1 9.8 -2.3 -15 Foreign trade 23.5 32.1 -4.3 -43.5 unemployment 6.1 6.3 7.1 9.5 M&A (value) 194.6 -36.5 -38.6 4.8 40 Perspective of economic growth: Crisis is serious (pessimist)⇔no crisis, crisis hit the bottom (optimist) 2009 2010 IMF -6.0 0.5 World Bank -4.5 0 OECD -5.6 0.7 EBRD -7.5 2.5 Goldman Sachs -7.3 3.8 Russian Government -2.2 2-3 41 Defaults of corporate bonds (cases) 2008 2009.JanuaryApril Total Defaults total 56 77 133 Refinanced loan 8 18 26 Technical defaults 25 14 39 Employment (million) 73 72 71 70 69 68 67 66 65 2008April employment July Oct. 2009.Jan. April July 43 Unemployment rate (%) 10 8 6 unemployment rate 4 2 0 2008Apr. June Aug. Oct Dec Feb April June 44 Russian recovery perspective and positive scenario signals • First Quarter 2009 oil and gas price increase and stabilisation. Urals price $ 55 per barrel in May 2009. • Ruble Exchange rate stability against the USD/EUR currency basket. • Russian government and households sectors are not overleveraged. • Russian corporate sector is restructuring and servicing the debts. Volume of payments $ 114 bln. Per year 2009. • Reserve Fund and public debt resources are used to support 2009-2010 Budget expenditures. • Public budget and Central bank of Russian capital and subordinate credit investments supported the Bank System equities. • Public guarantees and credit placement to refinance corporate debts • 2009-2010 Public and private capital investments to start GDP recovery. 45 Symptoms of recovery After the first quarter of 2009, we can observe some symptoms which signal the end of the panic period. A.Kudrin, the Minister of Finance, considered Russia got out of the crisis in August. I.Shuvalov, the first vice-prime minister also announced a recovery of the economic growth. Oil price increased after May 2009, and the ruble exchange rate seems to be stabilised. Many corporations are restructuring and servicing their debts. The resident house price began to increase. In July 2009, almost all economic indicators were better than in June. Unemployment also declined to 6.3 million (8.3%). 3.Outcomes of the crisis: A collapse in the growth factors What did the crisis bring about in the Russian economy? Can Russia hold the growth factors based on the path in the 2000s? Specificities of the crisis in 2008 • The economic crisis is greatly influenced not only by the global economy but also by national specificities. Further, the crisis was contagious among not only the weak economies but also those showing strong macroeconomic performance; as a matter of course, the transition economies and emerging markets became the main target. Twin surplus in Russia • The subsequent dismal economic performance seems to have led Russian economists to describe extreme scenarios. These often included the ‘hard landing’ scenario Crisis in Russia not once in a hundred years but in ten years • Reconsidered 1998 crisis: GKO and the East Asian currency crisis • Fragility of domestic markets • From deficits in 1998 to surplus in 2008 common features and differences in the crisis International financial flow (1998 crisis) International fiancial markets Global oil and gas markets State bonds banks government Foreign reserve Enterprises Households 50 International financial flow (2008 crisis) Global oil and gas markets International financial markets banks government Foreign reserves Enterprises Households 51 Domestic microeconomic response to globalisation • Speculative behaviour (M&A oriented) • Natural resource • Diversified paths to gat chap money IPO However, • Capital flight and unmanaged trade surplus Overheated money demand M&A in Russia • World M&A(Thomson Financial):$ 4.48 trill. ($3.61trill. In 2006). USA 41%, Europe 40%, and Japan 3%. • M&A in Russia (2007) ReDeal:1260, $120.7bln. M&A:486, $124.6bln. Ernst & Young:$71 bln., of which 11.4 bln (In-out), 13.7 bln.(Out-in) in 2006. 2008:In-out23.6bln., Out-in26.2bln. 53 54 In-out and Out-in of M&A sectors Share of transact ion (%) Sectors 13739 58.13 energy 6017 23.00 energy 2685 11.36 food 3836 14.66 Construction and real estate 1837 7.77 finance 3819 14.60 3503 13.39 Technology centre 1677 7.10 Metallurgy and mining telecommunication 790 3.34 chemical 3190 12.19 entertainment 660 2.81 retail 2051 7.84 transportation 540 2.30 machinery 1431 5.47 machinery 470 1.97 pharmaceutical 930 3.57 finance 370 1.54 Transportation 760 2.92 others 870 3.67 others 620 2.36 23633 100.00 26162 100.00 55 Metallurgy and mining total total Value ($ million) Share of transaction (%) Value ($ million) IPO financing • An increase of syndicated loans: short term funds • An increase of IPO/SPO 29.4 billion (23 cases) in 2007 ⇒An increase of external debts • Suddenly dropped in 2008 External debts of Russia Jan. 2006 July 2006 Jan. 2007 July 2007 Oct. 2007 Jan. 2008 July 2008 Oct. 2008 Jan. 2009 April 2009 Total 257.2 288.8 313.2 399.2 437.8 471.0 535.7 548.2 483.5 450.8 State sector 150.7 (58.6) 153.8 (53.3) 137.1 (43.8) 175.5 (44.0) 188.4 (43.0) 190.8 (40.5) 198.0 (37.0) 191.2 (34.9) 161.8 (33.5) 147.2 (32.7) State organisation 82.1 78.9 48.6 49.0 52.5 46.4 38.9 42.8 32.7 30.1 Banks 19.4 27.4 32.0 54.2 59.2 65.5 78.2 71.2 61.7 54.4 Other sectors 49.3 47.6 47.1 72.3 76.7 78.9 81.0 77.2 67.4 62.7 Private sector 106.4 (41.4) 135.0 (46.7) 176.1 (56.2) 223.7 (56.0) 249.5 (57.0) 280.2 (59.5) 337.7 (63.0) 357.0 (65.1) 321.6 (66.5) 303.6 (67.3) Banks 30.8 39.3 59.8 76.1 87.7 96.9 113.1 125.2 102.9 90.6 Other sectors 75.6 95.6 116.3 122.5 136.0 156.4 191.8 199.0 186.0 179.7 Share of state secor in external debts (beginning of the year, % in total debts) 50 40 30 20 10 0 total in rubles 2007 2008 2009 in hard currency Ultimate debtors and government behaviour • Who is private sector? Firms which the government manages or holds more than 50% of shares like Gazprom (1/3), Firms which the government holds less than 50% (block shares) or strongly influences. Chebolization: “privatisation of profits and nationalization of deficits” • State-owned banks do not claim margin calls. Specific relation between government and enterprises • Protectionist measures 59 Anti-crisis measures 1) November 2008: stabilization of the financial situation-accessibility of financial resources, relaxation of business burdens, improvements of social results and others. The support to bog business 2) June 2009: social responsibility and the linkage between the anti-crisis measures and long-term projects (modernisation programme) Anti-crisis expenditure ($ billion) State gurantee Capital injection Assts purchase 0(0) 185(84) 11(5) 25(11) 222(13.9) UK 393(39) 79(8) 0(0) 549(54) 1020(37) USA 1769(50) 714(20) 663(19) 394(11) 3539(25) Germany 539(60) 177(20) 0(0) 176(20) 893(23) Japan 303(53) 0(0) 0(0) 273(47) 576(12) China 0(0) 0(0) 0(0) 570(100) 570(13) Russia others total Anti-crisis measures • Capital injection by the government • Protectionist measures: Subsidies • Guarantee of debts • Nationalization Anti-crisis modernisation programme (Shuvalov commission, V.Mau) strategic perspective of modernisation, list of untouchable enterprises Contents of June 2009 programme (1) social security, including employment, pension system, housing, etc. (2) the development of production and technological potential by increasing efficiency (3) the activation of domestic demand for Russian products using state investment and state order (4) the stimulation of innovation and structural reorganisation (5) the creation of an advantageous condition for economic growth by reforming market institutions and promoting SMEs (6) the formation of reliable financial markets (7) macroeconomic stabilization and reliance on domestic and foreign investors Government increased its holdings in the crisis: nationalisation • State control over economic activity is pervasive (OECD) • The number of majority stakes of the federal government increased • Establishment of state corporations • The state sector increased its share of assets in the banking sector: VEB using the oil money (the Fund of National Welfare) Anti-crisis economic policy • Access to financial resources (direct finance by -led banks and others) • Relaxation of business burden (tax, customs, administrative measures and others) • Improvement of social negative results and support to labour markets (enlargement of unemployment benefit, focus on education, housing and public health) • Stimulation of domestic demands (government order and others) • Support to SMEs Concentration to big business in the support measures Support to city enterprises and agglomeration Priority sectors: automobile, agricultural machine, defense, housing, construction PPP Strong protectionist measures 68 Main indicators of VEB (end of year, billion rubles) 2007 2008 Assets 540.5 1597.2 Credit portfolio 352.1 1061.6 Net income on interest Operational expenditure 4.1 20 4.6 14.3 profits 6.4 6.4 ( $ billion Russian foreign reserve ) 600 500 400 300 200 100 0 70 M&As by symbolised prices price buyer asset sector Debts Costs for recovery Date of transaction 100 rubles Alrosa 90% KITFinance bank 100-120 billion rubles 90 billion rubles Jan. 2009 5000 rubles NRK Rossiiskii kapital bank n.d. 8.2 billion rubles Oct.2008 5000 rubles VEB 90% Cvyz’bank bank 60 billion rubles 59 billion rubles Oct.2008 5000 rubles VEB 99% Globeksa bank n.d. 80 billion rubles Oct.2008 1 million rubles Gazpromen ergobank 75% Soyuz bank n.d. n.d. Dec.2008 1 Euro S.Pugachev 65.1% Soir media n.d. 10 million E Jan. 2009 60 rubles VEB 51% Systemy-Gals develo pment $ 700 million 5 billion rubles March 2009 $1 Moscow city 75% Sky Express airlift 2.5 billion rubles n.d. 2008 No cash Sverbank 100% Moi gorod retail $ 22 million n.d. Q1 2009 No cash Sverbank 17% capital city Mixedused $400 million n.d. Q1 2009 System-formation enterprises • From strategic industry and enterprises to system organizing- technological centre, large job provision, exporter, large investor, inter-departmental sector (MIC, metallurgy, company town and others) • 325 billion Ruble • 294 system organizing enterprises • State guarantee for credit: 70% of defense enterprises • rescue of leading enterprises Effects of the policy • GU-VSE and MATS are skeptical: 60% have a weak effect. • The policy includes negative aspects: the worsening of competition, corruption, asymmetric information between businesses and the government • Another nationalisation in social aspect: reduced working hours and others Weak response in employment • • • • Informal sector expands Incomplete employment has increased Wage arrears revived. – illegality Non-monetary transaction revived.-barter and mutual settlement (barter does not increase by Russian economic barometer) • Work hours decreased and temporary holidays increased (Russian work share) Robust foundation of the Russian society Unemployment and unpaid work Wage Arrears (millon R) 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 1 2 3 4 5 6 2008 7 8 9 10 11 12 1 2 2009 3 4.Causes and the significance of the crisis in Russia Specificities of the crisis and the meaning of the crisis Global factors The structural crisis of the ‘New Economy (service sector, asset based economy based information technology)’ Financial deregulation Overheated investments and the housing bubble Lack of liquidity and the credit crunch among financial organizations Mistakes made by the US government and Federal Reserve Board (FRB) Market failure through securitization and the increases in the securitization risk The uncertainty associated with derivatives Credit expansion through deregulation and uncontrolled financial technology Global inflow of excess money into forward markets (deterioration of the real sector by price jumps and the outflow of funds) The linkage between uneasy psychology and panic The real sector crisis stemming from a demand decline caused by drastic decreases in stock prices and the adverse wealth effect A decline in investment, consumption and employment An upturn in the interest rate from credit risk (monetary constraints) Causes of the crisis by V. Mau (1) the root factor of the inadequate financial policy of the US (2) fundamental and systematic factors such as the very aggressive growth-oriented policies of developed countries and the development of financial technology (3) factors specific to Russia. From the perspective of global capitalism, the flow of global finance has changed Economic growth has become a key factor in the crisis. 21st century crisis 21st century financial crisis: 1) private short term fund (Hedge Fund), 2) a decrease of IMF function 3) fragile financial system and drastic de-regulation 4) firm’s dependence on indirect financing and foreign capital Closely involved in the global economy and cheap global money Crisis as the periodicity of business fluctuations • Russia synchronized with the business cycle of the global capitalism. Russia has competed the transition period. • Stagflation in Russia: high inflation and recession Crisis in Russia Inflation: price increasing crisis Drop down of production 82 Linkage of developed country and emerging market economy Emerging market economy Financial pressure fragility Global factors: price production Interest rate Source: IMF, 2009, p.143 Linkage of finance Specific factors Developed countries Financial pressure 84 Specificity of crisis in Russia Stagflation (Depression or stagnation and inflation) for Russia and CIS Deflation and Depression for developed countries Crisis under the dual profits (budget and balance of payments) Crisis as transition indicators A comparison of economic background in 1998 and 2008 • Different political situation: regency (weak president) vs authoritarian (strong president) • Different economic policy: stabilization and state intervention by GKO vs high economic growth and 4I • Different economic situation Macroeconomic indicator : growth, inflation and finance Micro economic performance: loss-making enterprises and barter transaction Labour and social indicator: employment and income Contrast of two periods Comparison of crisis in 1998 and 2008 Source of crisis Acors of crisis Volume of external debts ($ billion) GKO holders 20 (banks) 1998 crisis GKO, government 2008 crisis Loans, Debtors global crisis (banks, and banks enterprises) and enterprises 500 External reserve ($ billion) 10 800 87 Comparison of crisis in 1998 and 2008 Financial deficits Final debtors 1998 crisis Large deficits government 2008 crisis Stable surplus, austerity economic policy, sterilization policy Enterprises and banks (private but semigovernment, government) 88 Comparison of three crises 1992 1998 2008/2009 Political crisis Yes Yes No Decline of demand Yes accompanied with collapse of USSR and CMEA No Yes linked with cyclical recession in the global economy and overheat in the non-trade sector Decline of oil price No Yes Yes Currency crisis Yes Yes affected by managed devaluation of ruble and rejection of exchange rate change by monetary authority Yes affected by appreciation of ruble and rejection of exchange rate change by monetary authority Instable state budget Yes Yes No A decline of revenue does not bring about instabilisation due to Stabilisation Fund Debts crisis No Russian cannot attract foreign money Yes The main debtors were state Yes The main debtors were corporate sector Capital flight No Yes Short-term state borrowing led outflow of capital for clearing GKO Yes Foreign investment led outflow of capital for declining markets A comparison of crisis in 1998 and 2008 • International financing and foreign debts caused the crisis. GKO vs M&A weak domestic financial markets difference: international balance: from state to private, shot term funds • Relaxation of restriction on capital transfer extended dependence on foreign capital. Parallel economy functioned in Russia. Capital flight • The fragility of the domestic financial market made financing more delicate. • Mistake of Central bank: reluctance of devaluation ex Argentine Different characteristics of crisis in 1998 and 2008 • Petroleum price (determined not by supply ability but by speculative funds, abnormal price change in 2008) 1) increase of Russia’s dependence on exporting resources: from 32% in 1998 to 62% in 2007, narrower economy 2) state budget dependence on the petroleum price: foreign reserves • International financial flow M&A funds and IPOs Russian specific factors (1) Political situation (2) High dependence on export of raw materials: Due to the crisis the prices and the demand for the main Russian export goods sharply declined.—1) capital flight, 2) government’s dependence, 3) dependence on foreign money, 4) out of control of oil price (3) The fragility of the market: financial market and monopolisation, M&As (4) Russian peculiarities 92 Ownership in companies in Russia 1995 1997 1999 2001 2003 2005 2007 2009 * Insiders, total 54 52 50 50 50 48 51 55 Managers 11 15 15 19 25 31 35 41 Workers 43 37 34 28 22 16 13 10 Outsiders, total 37 42 42 42 45 45 40 38 Non-financial outsiders 27 31 33 34 36 38 31 24 Outside individuals 11 15 20 22 21 20 13 8 Other enterprises 16 16 13 12 15 18 18 16 Financial outsiders 9 9 7 8 8 5 8 13 State 9 7 7 7 4 7 9 7 Russian peculiarities: response of economic actors • Specific adaptation: revival of “transition phenomena” Labour market and employment: low elasticity in employment (informal sector, incomplete employment), high elasticity in wage Transaction: barter ad non-monetarized transaction • Enterprises kept their speculative activity 94 Russia’s specificities in crisis • Unbalance of transaction: heavy import dependence and natural resources (direct impact) • Violation of liquidity: chap foreign money and high leverage ratio • Inflation with weak competitiveness: The government cannot devaluate Ruble. • Self-satisfaction of national financial system with speculation • Speculative management with Russian corporate governance • Abnormal Russia survives. Transition and crisis From the perspective of market transition, paradoxically speaking, it can be stated that the Russian transition concluded as a result of a close linkage with the global market as well as the regressive institutional changes and regeneration of embedded institutions. However, the end of market transition does not mean that one needs to build an Anglo-Saxon-type liberal market economy. As far as the state continues intervening and businesses do not lose their paternalistic behaviour, the Russian-type coordinated market will continue to be fragile. The weak competitiveness along with profits from abundant resources becomes a catalyst for crises, and the sustainability of the market institutions is undermined by conditions such as aging equipment and shortage of labour force and skills. At the beginning of 2008, the outdated (no longer serviceable) machines occupied 51.1% in enterprises. (1) Government failure: deep-rooted corruption • Corruption of bureaucrats: The economic policy doe not have consistency. • Corruption of police and public servants: enforcement of the law is weak. • There are many cases of takeover including raids. Ownership and M&A have a risk. • Administrative costs are pervasive. Russian corruption (INDEM fund) 2001 2005 Corruption involved 50.4% 54.9% Corruption risk 25.7% 35.0% Bribe average (Ruble) 2162 2452 Total business 33 corruption value ($, billion) 316 (2) The population problem is unsettled. • From 148.3 million in 1991 to 141.9 million in 2009 (-4.3%) • A decline of population brings about shortage of labour forces. Labour forces decreased from 75 million in 1992 to 74.2 million in 2006. • The social policy is difficult to keep in the future. • The age structure distorted. • A decline accompanies depopulation and overpopulation. 2006 Populatio 142.24 n million 2007 142 Natural change - 687 - 478 thousand thousand Social change + 132 + 240 thousand thousand (3) Skill and human resource are indispensable for survival. • The most difficult constraints for the firm is human resources. • The skill formation system in the Soviet period collapsed. The advantageous condition of Russia “potential good labour force” disappeared. • The new skill formation system has not created yet. The talented skill market and temp agencies are not well organized. • The size of non-regular workers is 15%. Constraints of enterprises (%) % 80 60 domestic demand import unpaid 40 lack of finance lack of employees lack of equipment 20 0 1995 1998 2001 2003 2005 2007 Young people change their job. 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 Less than one year 41 43 43 41 40 1-2 years 30 29 27 28 28 2-5 years 21 19 19 21 21 5-10 years 13 15 12 12 16 10-20 years 13 12 13 10 12 More than 20 years 9 12 11 10 10 Conclusion • The global crisis penetrates the Russian economy and it has a chance to adapt the global standard. E.g. revision of law on bankruptcy • Before the global crisis, the Russian economy has changed its economic structure under the economic growth. Russian was synchronized with the global capitalist business cycle, and the Russian economy cannot survive without the global markets. 102 • Strong hand of the government characterizes the Russian market. • The crisis recalled the Russia’s innate institutions and such institutions played a role of soft-landing (adjustment behaviour) of the crisis. • Russia continues to face a market that is both fragile and robust. Thank you •Fin 104