Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Private equity secondary market wikipedia , lookup

Present value wikipedia , lookup

Mark-to-market accounting wikipedia , lookup

Lattice model (finance) wikipedia , lookup

Financialization wikipedia , lookup

Public finance wikipedia , lookup

Financial economics wikipedia , lookup

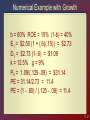

Macroeconomic and Industry Analysis Chapter 17-19 McGraw-Hill/Irwin Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved. Fundamental Analysis Approach to Fundamental Analysis: Domestic and global economic analysis Industry analysis Company analysis Why use the top-down approach? 17-2 Global Economic Considerations Performance in countries and regions is highly variable. Political risk Exchange rate risk Sales Profits Stock returns 17-3 Key Economic Variables Gross domestic product Unemployment rates Interest rates & inflation International measures Consumer sentiment 17-4 Domestic Economic Policy Fiscal Policy - government spending and taxing actions. Direct policy Slowly implemented Monetary Policy - manipulation of the money supply to influence economic activity. Initial & feedback effects Tools of monetary policy Open market operations Discount rate Reserve requirements 17-5 Shocks Demand shock - an event that affects demand for goods and services in the economy. Tax rate cut Increases in government spending Supply shock - an event that influences production capacity or production costs. Commodity price changes Educational level of economic participants 17-6 Business Cycles Business Cycle Peak Trough Industry relationship to business cycles Cyclical Defensive 17-7 Cyclical Indicators Leading Indicators tend to rise and fall in advance of the economy. Avg. weekly hours of production workers Stock Prices Coincident Indicators tend to change directly with the economy. Industrial production Manufacturing and trade sales Lagging Indicators tend to follow the lag economic performance. Ratio of trade inventories to sales Ratio of consumer installment credit outstanding to personal income 17-8 Industry Analysis Sensitivity to business cycles Sensitivity of earnings to business cycles depends on: Sensitivity of sales of the firm’s product to the business cycles Operating leverage Financial leverage Industry life cycles Stage Sales Growth Start-up Consolidation Maturity Relative Decline Rapid & Increasing Stable Slowing Minimal or Negative 17-9 Sector Rotation Portfolio is adjusted by selecting companies that should perform well for the stage of the business cycle Peaks – natural resource extraction firms Contraction – defensive industries such as pharmaceuticals and food Trough – capital goods industries Expansion – cyclical industries such as consumer durables 17-10 Equity Valuation Models Chapter 18 McGraw-Hill/Irwin Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved. Models of Equity Valuation Basic Types of Models Balance Sheet Models Dividend Discount Models Price/Earning Ratios Estimating growth rates and opportunities Intrinsic Value Self assigned value or estimate derived from a variety of models Market Price Consensus value of all potential traders Trading Signal IV > MP Buy IV < MP Sell or Short Sell IV = MP Hold or Fairly Priced 17-12 Dividend Discount Models: General Model Dt Vo t t 1 (1 k ) V0 = Value of Stock Dt = Dividend k = required return 17-13 No Growth Model D Vo k Stocks with earnings & dividends expected to be constant (often preferred stock) E1 = D1 = $5.00 k = .15 V0 = $5.00 / .15 = $33.33 17-14 Constant Growth Model Do (1 g ) Vo kg g = constant perpetual growth rate E1 = $5.00 b = 40% k = 15% (1-b) = 60% D1 = $3.00 g = 8% V0 = 3.00 / (.15 - .08) = $42.86 17-15 Estimating Dividend Growth Rates g ROE b g = growth rate in dividends ROE = Return on Equity for the firm b = plowback or retention percentage rate (1- dividend payout percentage rate) 17-16 Specified Holding Period Model P D D D ... V (1 k ) (1 k ) (1 k ) 1 0 N 2 1 2 N N PN = the expected sales price for the stock at time N N = the specified number of years the stock is expected to be held 17-17 Growth & No Growth Components of Value E1 Vo PVGO k Do (1 g ) E1 PVGO (k g) k PVGO = Present Value of Growth Opportunities E1 = Earnings Per Share for period 1 17-18 Partitioning Value: Example ROE = 20% d = 60% b = 40% E1 = $5.00 D1 = $3.00 k = 15% g = .20 x .40 = .08 or 8% 17-19 Partitioning Value: Example 3 Vo $42.86 (.15.08) 5 NGVo $33.33 .15 PVGO $42.86 $33.33 $9.52 Vo = value with growth NGVo = no growth component value PVGO = Present Value of Growth Opportunities 17-20 Price Earnings Ratios P/E Ratios are a function of two factors Required Rates of Return (k) Expected growth in Dividends Uses Relative valuation Extensive Use in industry 17-21 P/E Ratio: No Expected Growth E1 P0 k P0 1 E1 k E1 - expected earnings for next year E1 is equal to D1 under no growth k - required rate of return 17-22 P/E Ratio with Constant Growth D1 E1(1 b) P0 k g k (b ROE ) P0 1 b E1 k (b ROE ) b = retention ratio ROE = Return on Equity 17-23 Numerical Example: No Growth E0 = $2.50 g=0 k = 12.5% P0 = D/k = $2.50/.125 = $20.00 PE = 1/k = 1/.125 = 8 17-24 Numerical Example with Growth b = 60% ROE = 15% (1-b) = 40% E1 = $2.50 (1 + (.6)(.15)) = $2.73 D1 = $2.73 (1-.6) = $1.09 k = 12.5% g = 9% P0 = 1.09/(.125-.09) = $31.14 PE = 31.14/2.73 = 11.4 PE = (1 - .60) / (.125 - .09) = 11.4 17-25 Pitfalls in P/E Analysis Use of accounting earnings Historical costs May not reflect economic earnings Reported earnings fluctuate around the business cycle. 17-26 Other Valuation Ratios Price-to-Book Price-to-Cash Flow Price-to-Sales 17-27 Inflation and Equity Valuation Inflation has an impact on equity valuations. Historical costs underestimate economic costs. Empirical research shows that inflation has an adverse effect on equity values. Research shows that real rates of return are lower with high rates of inflation. 17-28 Lower Equity Values with Inflation Shocks cause expectation of lower earnings by market participants. Returns are viewed as being riskier with higher rates of inflation. Real dividends are lower because of taxes. 17-29 Financial Statement Analysis Chapter 19 McGraw-Hill/Irwin Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved. Overview Purpose Tools Used Statements Ratio Analysis Limitations 17-31 Financial Statements Balance Sheet Common Sized Trend or Indexed Income Statement Common Sized Trend or Indexed Statement of Cash Flows 17-32 Ratio Analysis Purpose of Ratio Analysis Uses Trend analysis Comparative analysis Combination Use by External Analysts Important information for investment community Important for credit markets 17-33 Type of Financial Ratios Liquidity Ratios Activity or Mgmt Efficiency Ratios Leverage Ratios Profitability Ratios Market Price Ratios 17-34 Liquidity Ratios Current Ratio Current Assets Current Liabilities Quick Ratio Current Assets - Inventory Current Liabilities 17-35 Activity or Management Efficiency Ratios Inventory Turnover Sales or Cost of Goods Sold Inventory Total Asset Turnover Sales Total Assets 17-36 Activity or Management Efficiency Ratios Average Collection Period Accounts Receivable Sales Per Day Days to Sell Inventory Inventory Sales Per Day 17-37 Leverage Ratios Times Interest Earned Earnings Before Int. & Taxes Interest Expense Fixed Charge Coverage Ratios Lease Payments Principal Repayments Preferred Dividends 17-38 Leverage Ratios Debt to Assets Long Term Debt Assets Debt to Equity Long Term Debt Shareholders Equity 17-39 Profitability Ratios Net Profit Margin % Net Income Sales Return on Assets Net Income Total Assets 17-40 Profitability Ratios Return on Equity Net Income Common Equity Operating Margin After Depr. Operating Profit Sales 17-41 Market Price Ratios Price to Earnings Market Price of Stock Earnings Market-to-Book-Value Market Price of Stock Book Value Per Share 17-42 Decomposition of ROE ROE = Net Profit x Pretax Profit Burden x EBIT (1) Tax Pretax Profit x x (2) Interest Burden x EBIT Sales (3) x x Sales Assets x Assets Equity (4) x (5) x Margin x Turnover x Leverage 17-43 Economic Value Added Difference between return on assets (ROA) and the opportunity cost of capital (k) EVA = above difference time the invested capital EVA can be positive or negative for firms that have positive earnings 17-44 Comparability Problems Accounting Differences Inventory Valuation Depreciation Inflation International Accounting Conventions Reserves –more or less flexibility allowed in use of reserves. Depreciation –separate tax and reporting presentations may be allowed. Intangibles – treatment varies widely. 17-45