Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

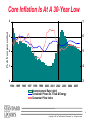

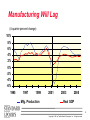

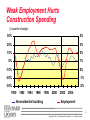

A New World David Wyss Chief Economist SIOR Boston October 2001 1 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved The Economy is in Recession We were skirting very close to recession The disaster has pushed us over the edge The consumer is scared Layoffs are rising Air travel is dead, and orders are being canceled But: The Fed is shoving interest rates down Fiscal policy will be very expansionary And consumers are resilient 2 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Inflation Will Stay Low Unemployment is rising There will be no wage pressure Security costs will cut productivity and raise prices, but impact will be borne mostly by government The dollar is remaining stable, but how much is it central banks? Oil prices are the big risk, but so far they are down 3 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved (% ch from year earlier) Core Inflation Is At A 30-Year Low 4 7 3 6 2 5 1 4 0 3 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Unemployment Rate (right) Consumer Prices Ex. Food & Energy Consumer Price Index 4 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Energy Costs Are Back to Normal ($/barrel, refiners acquisition price and deflated by CPI; consumer energy as percent of disposable income) 80 70 60 50 40 30 20 10 0 9% 8% 7% 6% 5% 4% 3% 2% 1% 1970 1973 1976 1979 1983 1986 1989 1992 1996 1999 2002 2005 $/Barrel 2000 prices Energy cost/disposable income 5 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved The Fed Is Loosening Aggressively (Percent) 8 6 4 2 1993 1995 1997 1999 Federal Funds Rate 2001 2003 2005 10-Year Treasury Bond Yield 6 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Mortgage Rates Are Low (Percent) 11 10 9 8 7 6 5 4 1990 1992 1994 1996 1998 2000 Conventional Mortgage Rate 2002 2004 10-year Treasury 7 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Heavy Government Spending Will End the Surplus Tax cuts had already eliminated the on-budget surplus The recession will hurt revenue further. Additional spending for defense, security, and recovery will eliminate the off-budget as well The spending is needed. The tax cuts aren’t. We need money to wage a war. Result will be higher Treasury yields 8 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Inventories and Equipment Spending Dominate the Slowdown (Percentage point contribution to growth) Real GDP Consumption Nonres. Const. Prod. Equip. Res. Const. Inventories Government Net Exports -4 -2 '2001:2 0 '2001:1 2 '2000:4 4 '2000:3 6 '2000:2 9 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Investment Was Already Plunging Low capacity utilization makes new capacity unnecessary. Interest rates won’t help much unless capacity is needed Worst earnings drop in postwar period. Speculative grade yields are high. Rebuilding activity and enhanced security spending will offset some of the decline 10 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Investment Follows GDP (4-quarter percent change) 8% 20% 6% 15% 4% 10% 2% 5% 0% 0% -2% -5% -4% -10% 1990 1992 1994 Real GDP (right) 1996 1998 2000 2002 2004 Equipment spending (left) 11 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Manufacturing Will Lag (4-quarter percent change) 10% 8% 6% 4% 2% 0% -2% -4% -6% 1995 1997 1999 Mfg. Production 2001 2003 2005 Real GDP 12 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Weak Employment Hurts Construction Spending (4-quarter change) 30% 4% 20% 3% 10% 2% 0% 1% -10% 0% -20% -1% -30% -2% 1990 1992 1994 1996 Nonresidential building 1998 2000 2002 2004 Employment 13 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Vacancy Rates Have Started to Rise U.S. Office Vacancy Rates CB Richard Ellis 25 20 Suburban 15 10 5 Downtown 0 84 86 88 90 92 94 96 98 00 02 14 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Public and Utility Construction is Stronger (4-quarter change) 30% 20% 10% 0% -10% -20% 1990 1992 1994 State & local 1996 1998 2000 2002 2004 Utilities 15 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Can the Consumer Keep Spending? Saving rate has dropped sharply Confidence will plunge after the attack The stock market has wiped out wealth Debts and defaults are already at record highs The tax cut will provide extra income And lower mortgage rates are freeing up funds Net result will be a slowdown, not a retreat But the saving rate will rise 16 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Saving Plunged As Wealth Hit A Record High 6.5 (Percent of Income) 15 6 12 5.5 9 5 6 4.5 3 4 0 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 Wealth/income Saving rate (right) 17 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Debt Is Hitting New Records, Dominated By Mortgages (Household debt as share of after-tax income) 120 100 80 60 40 20 0 1980 1983 1986 1989 1992 Total 1995 1998 2001 2004 Mortgages 18 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved College Unemployment Is Rising Most (Unemployment rate, persons 25 & older) 10 8 6 4 2 0 HS Dropout Jan-97 High School Some College Oct-00 College Grad Sep-01 19 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved More Affordable Housing Allows More Households To Own Their Home 1.40 68 1.20 66 1.00 64 0.80 62 0.60 60 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 Homeownership Rate (Right scale) Affordability (Left scale) 20 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved The Stock Market Will Recover, But Slowly Market rose 21%/year from 1995 -99 But has dropped since March 2000 First consecutive down years since 1973-74 Profits cannot continue to outpace GDP And share prices cannot continue to outpace earnings Stocks will thus yield much less in the future than in the recent past. 21 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Five Consecutive Years of 20%Plus Returns (Percent) 50 40 30 20 10 0 -10 -20 1990 1992 1994 1996 1998 Stock Market Return 2000 2002 2004 Bond Yield 22 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Long Bull Markets Are Followed by Periods of Weakness (Percent return on S&P 500 and corrected by CPI) 20 15 10 5 0 -5 1946-66 1966-81 Nominal 1981-99 1999-2009 Real 23 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Does Stock Picking Work? 1600 1200 800 400 0 86 1 STAR 4 STAR 88 90 92 2 STAR 5 STAR 94 96 98 2000 3 STAR S&P 500 INDEX 24 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Western And Southern States Have The Strongest Employment Growth (Annual percent change, 2000 to 2005) 1.5 . to 3.6 1.1 to 1.5 0.8to 1.1 0.4 to0.8 25 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved And Highest Unemployment Rates (Percent of labor force, July 2001) 2.5 - 3.4 3.5 - 4.4 4.5 - 5.5 5.5 + 26 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved Manufacturing States Suffer Most (12-month percentage-point rise in unemployment, July 2001) Decline 0 - 0.4 0.5 - 0.9 1.0 + 27 Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved