Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

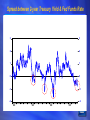

Current State of Automotive Industry: Where Is It Going? Ted Chu Lead Economist General Motors Corporation September 6, 2007 The Yin and Yang of Global Auto Industry Income growth and urbanization OE restructuring and new entries AUTOMOBILE INDUSTRY Innovation and integration Pressure on energy and environment Bottom Line: More business — but tougher business Economic & demand growth Global Real GDP* Growth Outlook 5% 4.1 4% 3.9 3.9 3.7 3.4 3% 3.5 3.3 3.2 3.3 3.4 2.8 2.5 2.5 1.9 2% 1.4 1.9 1.6 1.6 1% 0% ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 * Based on market exchange rates. Base year = 2005 Global Industry: Continues to Outperform Expectations Thousands 70,000 60,000 50,000 Japan bubble Gulf War Europe recession 40,000 Second oil crisis 30,000 ‘80 ‘82 ‘84 Actual ‘86 ‘88 ‘90 ‘92 ‘94 BP01 ‘96 ‘98 Linear (Actual) ‘00 ‘02 ‘04 ‘06 New Vehicle Sales by Region Millions 40.0 Forecast 37.1 30.0 AP 25.5 Europe 22.7 20.0 NA 10.0 LAAM 0.0 ‘80 ‘85 ‘90 ‘95 ‘00 Source: GMIA; GSRA, July 2007 Short-term Forecast, Prelim BP08 ‘05 ‘10 9.1 ‘15 U.S. Economic Forecast Economy forecasted to expand 1.9% in ’07 and 2.7% in ‘08 Residential housing sector will remain a weak spot of the economy going into 2008 Unemployment rate expected to remain low, but will increase from current 4.5% The U.S. dollar will generally remain weak against major currencies through 2008, providing support to exports Downside risks for 2008 forecast remain high Housing market could be worse than expected Spill-over of sub-prime market slump to the broader credit market Energy prices could be volatile Key U.S. Economic Indicators From Recession From 2003:Q2 From 2006:Q2 Recession through 2003:Q1 through 2006:Q1 to Current Latest Data2 Real GDP Average Q/Q% @ AR -0.2% 1.7% 3.5% 1.6% 3.4% Real Consumption Average Q/Q% @ AR 1.5% 2.7% 3.5% 3.2% 1.3% Index of Consumer Sentiment Average Index 88.2 87.7 91.2 88.1 90.4 Nonfarm Payroll Employment Average Monthly Change, Thousands -203 -61 160 160 92 Real Disposable Income Average Y/Y% Change 1.8% 2.6% 2.7% 3.2% 3.1% Corporate Profits Average Y/Y% Change -1.5% 18.6% 12.9% 10.3% 1.2% ISM-Manufacturing Index Average Index 44.4 51.5 0.0 53.0 53.8 New and Existing Home Sales Average, Thousands 5,611 6,015 7,113 6,522 5,844 West Texas Intermediate Average $/Bbl 25.67 27.18 45.45 64.64 67.48 CPI Inflation Average Y/Y% Change 2.8% 1.8% 2.8% 2.9% 2.4% Fed Funds Rate End of Period, Percent 3.4% 1.6% 2.2% 5.2% 5.25% 1 Notes: 1 2001:Q1 - 2001:Q3 for quarterly data or March 2001 - November 2001 for monthly data. 2 Latest quarter or month. New and Existing Single-Unit Home Sales New 1-Family Houses Sold: United States SAAR, Thous Existing 1-Family Home Sales: United States SAAR, Thous 6750 1400 6000 1200 5250 1000 4500 800 3750 600 3000 2250 400 05 00 95 Sources: Census Bureau, National Association of Realtors / Haver Analytics Spread between 2-year Treasury Yield & Fed Funds Rate 3 3 2 2 1 1 0 0 -1 -1 -2 -2 90 95 00 05 U.S. Productivity versus Labor Cost Nonfarm Business Sector: Output Per Hour/All Persons % Change - Year to Year SA, 1992=100 Nonfarm Business Sector: Unit Labor Cost % Change - Year to Year SA, 1992=100 6 12.5 10.0 4 7.5 2 5.0 0 2.5 -2 0.0 -4 -2.5 80 85 90 95 Source: Bureau of Labor Statistics /Haver Analytics 00 05 Business vs. Private Sector Auto Purchases Government 60 Business 50 Private 40 30 20 10 0 -10 -20 -30 -40 Q1 ‘02 Q3 ‘02 Q1 ‘03 Q3 ‘03 Q1 ‘04 Q3 ‘04 Q1 ‘05 Q3 ‘05 Q1 ‘06 Q3 ‘06 Q1 ‘07 Average Vehicle Transaction Price $26,500 $26,206 $25,846 $26,000 $25,855 $25,237 $25,500 $25,000 $24,710 $24,500 $24,218 $24,000 $24,006 $23,500 $23,000 $22,500 ‘01 ‘02 Source: GMIA, J.D. Power PIN ‘03 ‘04 ‘05 ‘06 ’07 CYTD Air Traffic Growth Outlook US (Airline Monitor, July '07) 2007 - 2.2% 2008 - 4.2% 2009 - 4.6% NA (Int'l Air Trans. Asso., Oct '06) 2007 - 4.5% 2008 - 4.3% 2009 - 4.1% U.S. Fleet Sales Outlook Relatively flat daily rental at slightly below 2 million units over next few years despite expected growth in leisure and business travel Structural shift of demand from light trucks to cars Import brands will step into the void left by the domestics, but they may not have the same impetus to play heavily in rentals as the Big 3 has done Government/commercial market is likely to see limited rebound over next few years The residential construction sector will take years to fully recover There could be some pull ahead into 2009 from 2010 due to diesel pricing in 2010 Innovation and Productivity Key Supply-side Developments Supply-side pressures are intensifying and driving improvements in product affordability Product choice continue to increase Squeeze in the middle Movement towards luxury/premium and upcontenting Consumers knowledge and expectations continue to increase Productivity, innovation, & cost cutting Price changes over the last 2 years US EU12 Germany UK France China 6.7% 4.4% 3.7% 4.5% 4.4% 3.8% 3.3% 2.8% 1.2% -0.8% -1.4% Total change in consumer prices (Annual, 2004-2006) -12.3% Total change in vehicle prices (Monthly, Mar-07 vs. Mar-05) * Note: Vehicle price changes are based on an equipment adjusted index (except China) China prices are for passenger cars only Sources: Bureau of Labor Statistics (US), Statistical Office of the European Communities, Cheshi Price Index Total Vehicle Entries – Selected Markets W & C Europe U.S. 407 356 Japan 442 394 289 258 287 Major Mature Markets 257 204 1995 2005 2010 Australia 142 206 225 China 253 Russia Major Emerging Markets 193 50 80 79 N/A India Mexico 19 233 53 78 Thailand 196 77 1995 2005 85 2010 S. Africa Brazil 131 147 129 65 90 232 174 73 Source: GMIA / EZQ Competition Has Intensified in the U.S. Year # of Models Big 3 Share 1965 96 90% 1975 185 81% 1985 245 73% 1995 287 72% 2003 322 63% 2006 352 56% Source: NA EZ Query GM Turnaround & Transformation GM continues to make significant progress in its North America turnaround Incentive spending is down Increased profitability of rental fleet sales Residual values and average transaction prices are up GM Turnaround & Transformation GM will continue to be a major player in the commercial fleet business GM will continue to grow volume and share with National Accounts and GM dealer commercial business We’ve grown our share in the commercial fleet business … and we intend to continue GM will not chase volume at the expense of profitability GM Turnaround & Transformation GM offers fleet customers the best products and service in the industry Chevrolet Impala “Fleet Car of the Year” two years in a row 2008 Chevrolet Malibu & Impala give GM the best mid-size lineup of any company GM offers customers newest and best-selling full-size pickups — Chevrolet Silverado & GMC Sierra Helping fleets “go green” without going broke Integration & Restructuring Changing Global Industry Landscape OE restructuring Production moves to low cost markets Rise of the AP region, esp. China Trade liberalization FX and other risks China: Vehicle Exports — 2006 C./E. Europe W. Europe 26,393 North America 48,925 Rest of Asia 19,869 Middle East 92,877 Central America and Caribbean 41,676 ASEAN 16,621 9,282 South America Oceania 21,037 994 Africa 61,582 Source: SIC, May 2007 Mini Chinese OEMs’ New Entries in 2007-2009 (Low-End Passenger Vehicles) Great Wall Perey, Reg. & 4X4 (’07) Small Chery A1 (’07) Lower Medium Great Wall Cool Bear (’07) Landwind CV7 (’07) Great Wall Florid (’07) Great Wall i7 (CH031) (’08) Chery M11 (A3) (’08) Chery M-12 (A3) (’09) Roewe W261 MG-3 (Concept) Hafei Saibao V JAC C926 (’07) What Will China Do to the Auto Industry? China's Share of Global Manufacturing Exports 9.0% In 2005, China’s GDP was around 5% of global GDP, but produced 50% of the world’s cameras 25% of washing machines 30% of air conditioners & TVs 20% of refrigerators 25% of toys 51% of microwave ovens 60% of bicycles 8.0% 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% ‘80 ‘82 ‘84 ‘86 ‘88 ‘90 ‘92 ‘94 ‘96 ‘98 ‘00 ‘02 ‘04 9% of automobiles Sources: WTO Statistical Database (2005), ATKearney – China Solutions Group Overview, Reuters News Report One reason why China must sustain high growth and low costs: 8 million college grads and 15 million migrant workers enter labor force each year Trade Agreements: Major Vehicle Producing Countries NAFTA EU Andean ASEAN Mercosur SADC Current trade agreements Future (likely signed by 2010) trade agreements • Even if signed within 5 yrs, auto transition periods may be longer • Black circles indicate major existing trade agreements Key Exchange Rates – Current vs. 5 Years Ago Jan-May Appreciation 2007 2002 80.95 110.30 -26.6% Euro 0.754 1.128 49.7% Japanese Yen 119.6 130.9 9.4% UK Pound 0.508 0.696 36.9% Canadian Dollar 1.149 1.583 37.8% Australian Dollar 1.248 1.894 51.8% South Korean Won 935.2 1,307.7 39.8% Brazilian Real 2.07 2.39 15.5% Mexican Peso 10.97 9.20 -16.2% Russian Ruble 26.11 31.01 18.8% 9.20 9.17 -0.4% UK Pound 0.675 0.617 -8.5% Japanese Yen 158.7 116.0 -26.9% 1,241.1 1,159.7 -6.6% Nominal Trade-Weighted Exch Value of US$ vs Major Currencies (Mar-73=100) Dollar Rates Euro Rates Swedish Krona South Korean Won Source: Federal Reserve (US), Wall Street Journal, Financial Times / Haver Analytics Pressure on Energy & Environment Crude Oil Price vs. U.S. Retail Gas Price Domestic Spot Market Price: Light Sweet Crude Oil, WTI, Cushing EOP, $/Barrel U.S. Retail Gasoline Price: Regular Grade Avg. U.S. $/Gallon 80 3.5 Oil prices surpass $70 per barrel and gas prices top $3 3.0 60 2.5 40 2.0 20 1.5 0 ‘00 ‘01 ‘02 Sources: WSJ, EIA / DO / Haver ‘03 ‘04 ‘05 ‘06 ‘07 1.0 Global Oil Consumption 000B/D 90,000 80,000 70,000 India Remaining Asia-Pacific 60,000 China Africa & Middle East 50,000 40,000 Europe 30,000 S. America 20,000 North America 10,000 0 ‘75 ‘78 ‘81 ‘84 ‘87 Sources: BP Statistical Energy Review 2006 ‘90 ‘93 ‘96 ‘99 ‘02 ‘05 GM’s Vision for Future Propulsion Technologies Improved Vehicle Fuel Economy & Emissions Displace Petroleum Hydrogen Fuel Cell Battery Electric Vehicles (E-Flex) Hybrid Electric Vehicles (including Plug-In HEV) IC Engine and Transmission Improvements Energy/Fuel Diversity Petroleum (Conventional & Alternative Sources) Bio Fuels (Ethanol E85, Bio-diesel) Electricity (Conventional & Alternative Sources) Hydrogen Recycling of Carbon Results in CO2 Benefits for Ethanol Compared to Gasoline CO2 in the atmosphere CO2 via photosynthesis CO2 emissions during fermentation Carbon in corn kernels Carbon in ethanol Carbon in crop residue Carbon in soil Ethanol plant CO2 emissions from ethanol combustion GM’s 2001 2-ModeHybrid Light Hybrid 2002 Portfolio 2003 2004 2005 2006 2007 2008 2009 GM/Allison Hybrid Bus Chevrolet Silverado/ GMC Sierra Saturn VUE Green Line Hybrid Saturn Aura Green Line Chevrolet Malibu Tahoe/Yukon Escalade 2-Mode Hybrid Silverado/ Sierra Saturn VUE Green Line Saturn VUE Green Line plug-in E-Flex Chevrolet Volt How will fleet market be impacted? Natural reaction in the marketplace to higher fuel prices … and to more powertrain options – hybrids, etc. Battery technology is key to plug-in hybrids and fuel cell development “Leaving no stone unturned” in improving fuel economy Commercial markets will always need larger vehicles and V8 engines to “get the job done.” Crossover vehicles, light duty diesel trucks, & other new products from GM Six Potential Surprises Global economic downturn around 2010 The peaking of energy/commodity “super cycle” The slowdown of U.S. productivity growth Structural reform accelerates in EuroZone The big breakthrough in powertrain and battery technologies Accelerated auto export drive from emerging markets