Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

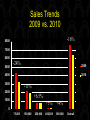

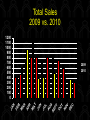

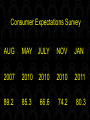

Market Overview January 2011 Total Single Family Sales for Jan-Nov 2007 vs. 2008 vs. 2009 vs. 2010 Douglas and Sarpy Counties 7416 7,000 7425 6524 6097 6,000 5,000 4,000 3,000 2,000 1,000 0 2007 2008 2009 2010 Sales Trends 2009 vs. 2010 -16% 8000 7000 6000 5000 -24% 2009 4000 2010 3000 -11% 2000 +6.5% 1000 +5% +4% 400,000 600,000 0 75,000 150,000 250,000 Overall Total Sales 2009 vs. 2010 1200 1100 1000 900 800 700 600 500 400 300 200 100 0 UG SE PT O C T N O V D EC A L JU N JU AY M PR A AR M B FE JA N 2009 2010 Inventories Increase in 2010 +12% 3000 2500 2000 1500 +17% Dec-09 +11% 1000 Dec-10 +13% 500 -7% +3% 0 75,000 150,000 250,000 400,000 600,000 TOTAL New Construction Inventories Increase in 2010 +8% 600 500 400 +4% 300 +19% 200 100 Dec-09 +15% Dec-10 -16% -45% 0 75,000 150,000 250,000 400,000 600,000 TOTAL Median Price $75,000 - $150,000 1% Median Price $150,000 - $250,000 1% Median Price $250,000 - $400,000 2% Median Price $400,000 - $600,000 2% Median Price $600,000 - $2,000,000 11% Total Sales Fall ’09 vs. Fall ‘10 700 600 500 2009 2010 400 300 200 100 0 SEPT OCT NOV DEC Consumer Expectations Survey AUG MAY JULY NOV JAN 2007 2010 2010 2010 2011 89.2 85.3 66.6 74.2 80.3 2010-2011 GDP FORECAST FANNIE MAE Q3 2.1 Q4 0.7 Q1 1.2 Source: http://www.fanniemae.com/media/economics Q2 0.9 NATIONAL HOUSING FORECAST FANNIE MAE 2009 Mean 2010 Mean 2011 Forecast Mean 5,530,000 5,199,000 5,432,000 CHANGE -6% CHANGE +5% Nebraska Economy Agriculture Insurance Manufacturing Transportation Housing Strong Strong Down Down Down Never has a “bubble Unemployment Lowest Rate in the U.S. Strong Nebraska Purchasing Manager Index 70 35.9 35.9 59 60 50 53 47 52 51 50 54 63 63 64 65 63 57 57 56 50 52 40 30 20 10 0 Aug- Sep- Oct- Nov- Dec- Jan- Feb- Mar- Apr- May- Jun- Jul- Aug- Sep- Oct- Nov- Dec09 09 09 09 09 10 10 10 10 10 10 10 10 10 10 10 10 Source: http://www.creighton.edu/business/economicoutlook/index.php 2010 VS. 2009 Non Ag. Business/Finance +1.5% Manufacturing +2.5% Construction No Growth UNL Bureau of Business Research 1.) Recovery likely to continue 2.) Rick of Double Dip Recession 3.) Weakness in Real Estate sector “FEARFULLY OPTIMISTIC” Positives 1. Lower House Prices 2. Higher savings rates - Lower indebtedness - Spending in line with income 3. Income growth supports - Consumption - Job Growth - Rising working hours Positives cont. 4. Business Growth - Exports - Technology 5. Fiscal Government restraint - Divided Federal Gov’t - Cost restraint Federal and State Levels - Gov’t cost restraint would encourage investment * Domestically * Internationally Negatives • Slow new construction • Buyers inability to sell existing home to enable purchase of a new home • Increased remodeling • Strong refinance activity The 2011 Outlook Omaha Outlook Employment Population Income New Jobs Self Employed Labor Force Unemployment Rate +1.5% +1.5% +4.5% 7000 Strong Growth Slow Growth to 4.5% Source: UNL Bureau of Business Research The 2011 Outlook Real Estate Markets 1. Improving Consumer Expectations 2. Improving Omaha Economic Conditions 3. Moderate but steady increase in activity in early 2011 4. High Inventories 5. Prices initially soft but firm up as inventories decline The 2011 Outlook HIGH END HOUSING Market focus on “needs” vs. wants Conservative buyer behavior High Real Estate Taxes Soft Pricing Trends The 2011 Outlook 1. Dependant on Market Mood a. Election - Done b. Tax Laws - Done c. Diminished expectation of new “stimulus” The 2011 Outlook 2. Pent up Demand a. Build up of buyers who went to the sidelines b. New buyers/sellers will move for typical reasons c. Could result in an active spring market The 2011 Outlook General Market Sales fall between 2008 and 2009 levels Mean for 1st half of 2008 & 2009 693 sales per month in 2008 vs. 806 sales per month in 2009 www.mitchellassociates.com Thank You