Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

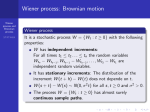

MONTE CARLO SIMULATION Topics • History of Monte Carlo Simulation • GBM process • How to simulate the Stock Path in Excel, • Monte Carlo simulation and VaR History of the Monte Carlo • http://www.youtube.com/watch?v=ioVccVC_Smg Markov Property • A Markov process is a particular type of stochastic process where only the present value of a variable is relevant for predicting the future Continuous-Time Stochastic Process • Suppose a variable follow a Markov stochastic process and its current value is 10. Suppose further that its value during 1 year is Type equation here. 𝑋~∅(0,1) • What is the probability of the change in the value during 2 year?......Ans. Because of the Markov process (independent distribution), the distribution 𝑋~∅(0,2) • What is the prob. of change during 6 months?…. • Generally, the change during a very short time period ∅(0, ∆t) but note that the variances of changes are additive but the standard deviations are not additive. Variance in 2, 3 years are 2 and 3 but the standard deviation are √2 and √3 Wiener Process • Wiener process is a particular type of Markov process. In physics, it is called as Brownian motion • If a variable z follows wiener process it must follow two properties • Property 1. The change in ∆z during a small time ∆t is ∆𝑧 = 𝜖 ∆t Where 𝜖 has a standardized normal distribution ∅(0,1) • Property 2. The value of ∆z for any two different short intervals of time ∆t are independent, thus • • • Mean of ∆z = 0, Standard deviation of ∆z = ∆𝑡 Variance of ∆z = ∆t The second property implies that z follows Markov process Graphically ∆𝑧1 𝜖 ∆t ∆𝑧 2 𝜖 ∆t ∆𝑧3 𝜖 ∆t ∆𝑧4 𝜖 ∆t ∆𝑧5 𝜖 ∆t Generalized Wiener Process • dS = a(Sdx = adt + bdz dx = a(S, t )dt + b(S, t)dz • ,mean change per unit of time is known as drift rate and the variance per unit is called as the variance rate)dt + b(S, t)dz Example • Suppose stock price follow the process of dx = adt or dx/dt = a Integrating with respect to time, we get x = x0 + at - Where x0 is the value of x at time 0. In a period of time of length T, the variable x increase by an amount of aT - bdz is regarded as noise or variability term added to the path of x - Wiener process has a standard deviation of 1.0. so, b times a Wiener process has a standard deviation of b. Stock price process: with out volatile If the volatility of stock price is zero, then ∆s = μ𝑠∆𝑡 When ∆𝑡 → 0, 𝑑𝑠 = μ𝑠𝑑𝑡 Or, 𝑑𝑆 𝑆 = 𝜇𝑑𝑡 Integrating between 0 and time T, we get 𝑆𝑇 = 𝑆0 𝑒 𝜇𝑇 Meaning that the stock price grow at a continuous compound rate of 𝜇 Stock price process with volatile 𝑑𝑠 = μ𝑠𝑑𝑡 + σsdz Or, 𝑑𝑠 𝑠 = μ𝑑𝑡 + σdz … … … … . . GBM For the discrete time, ∆𝑡 ∆𝑠 𝑠 = μ∆𝑡 + σϵ ∆𝑡 Return of stock price is normal distributed as; ∆𝑆 ~∅( 𝑆 μ∆𝑡, σ2 ∆𝑡) Change of x at small time changes and in time interval T ∆𝑥 = 𝑎∆𝑡 + 𝑏𝜖 ∆𝑡 • 𝜖 has a standard normal distribution. Thus, ∆𝑥 has a normal distribution with mean of ∆𝑥 = 𝑎∆𝑡 variance of ∆𝑥 = 𝑏 2 ∆𝑡 standard deviation of ∆𝑥 = 𝑏 ∆𝑡 • So, change in value of x in any time interval T mean of 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑥 = 𝑎𝑇 variance of 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑥 = 𝑏 2 𝑇 standard deviation of 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑥 = 𝑏 𝑇 Log normal return • When a log of any variable distribute as normal, we call it as lognormal distribute. We can show that the Log of returns is normally distributed as • 𝑙𝑛𝑆𝑇 − 𝑙𝑛𝑆0 ~∅ 𝜇− 𝜎2 2 𝑇, 𝜎 2 𝑇 • Or • 𝑙𝑛𝑆𝑇 ~∅ 𝑙𝑛𝑆0 + 𝜇 − 𝜎2 2 𝑇, 𝜎 2 𝑇 Fundamentals of Futures and Options Markets, 4th edition © 2001 by John C. Hull The Lognormal Property • These assumptions imply ln ST is normally distributed with mean: lnlnSS0 (( 2/ /22)T)T 0 2 and standard deviation: T • Because the logarithm of ST is normal, ST is lognormally distributed 11.14 Fundamentals of Futures and Options Markets, 4th edition © 2001 by John C. Hull 11.15 The Lognormal Property continued ln S T ln S 0 ( 2 2)T , T or ST 2 ln ( 2)T , T S0 where m,s] is a normal distribution with mean m and standard deviation s Fundamentals of Futures and Options Markets, 4th edition © 2001 by John C. Hull The Lognormal Distribution E ( ST ) S0 e T 2 2 T var ( ST ) S0 e (e 2T 1) 11.16 Monte Carlo Simulation (See Excel) • Suppose X follow the Wiener Process ∆𝑥 = 𝑎∆𝑡 + 𝑏𝜖 ∆𝑡 Suppose 𝑎 = 0.5, 𝑏 = 3.0 Find the path of X using Excel • To generate random variables using Excel Normsinv (rand()) * Note that rand() function generate the variables drawn from the uniform distribution, but to keep it simple just use it to generate ‘Z’. 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 101 value of x Monte Carlo Simulation (See Excel) 80 70 60 50 40 30 20 10 0 -10